VA Loan Credit Score Requirements: No VA Minimum, Lenders Do

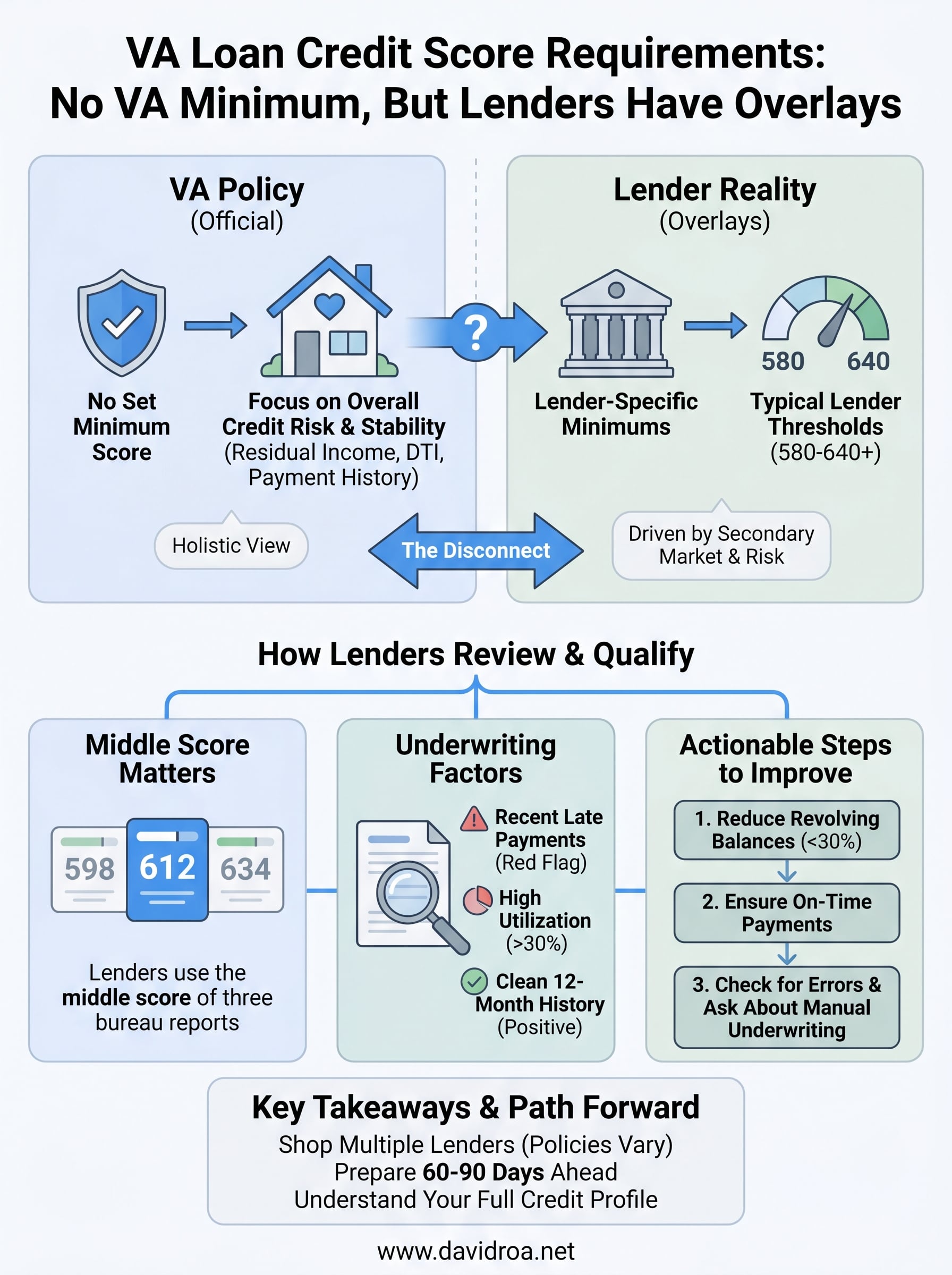

The VA doesn't set a minimum credit score to use your home loan benefit. That's the official policy, and it surprises most veterans and active-duty service members who start researching va loan credit score requirements. But here's where it gets tricky: the lender you apply with almost certainly does set one. Every mortgage company adds its own qualification thresholds, called "overlays," and those typically land somewhere between 580 and 640.

That gap between what the VA allows and what lenders actually require is where confusion, and missed opportunities, pile up. With over 25 years funding residential mortgages, including VA loans, I've walked hundreds of borrowers through this exact disconnect. At David Roa, we work directly with veterans and military families to match their credit profile to the right lending program, whether that means a lender with lower overlay requirements or a short-term credit strategy before applying.

This article breaks down the real credit score thresholds lenders use for VA loans, explains why they differ from VA guidelines, and gives you a clear path forward regardless of where your score sits today.

What the VA actually requires

The Department of Veterans Affairs publishes clear guidelines for VA home loans, and credit score minimums are not among them. According to the VA's official loan guaranty program, the agency focuses on whether a borrower presents a satisfactory credit risk overall, not on hitting a specific number. That distinction matters enormously when you start comparing your options across lenders.

The VA's official credit policy

The VA underwrites loans based on a holistic review of your financial history. Residual income, the money left over after paying all major monthly obligations, carries significant weight in that review, as does your overall debt-to-income ratio. The VA wants to see that you have the capacity to repay the loan and a reasonable pattern of meeting your financial obligations, even if your score has taken some hits along the way.

The VA's own guidelines make clear that a below-average credit history alone is not sufficient grounds to deny a loan, lenders must document a specific reason tied to your overall credit pattern, not just a score.

Your credit history gets reviewed in context, including late payments, collections, and bankruptcies. A medical collection that went unpaid during a deployment, for example, carries different weight than a pattern of missed installment payments over the past 12 months. The VA expects lenders to account for that context rather than apply a blanket cutoff.

What the VA does evaluate instead

Rather than a score threshold, the VA looks at several concrete factors when determining whether you present an acceptable credit risk. Here's what actually gets reviewed:

- Payment history on installment accounts: mortgages, auto loans, and student loans receive the most scrutiny

- 12-month rental or mortgage payment history: consistent on-time payments here work strongly in your favor

- Major derogatory events: bankruptcies require a two-year discharge, foreclosures typically two years as well

- Collections and judgments: unpaid collections don't automatically disqualify you, but active judgments are a serious problem

- Residual income thresholds: the VA sets specific dollar minimums by region and family size

Understanding these factors gives you a far clearer picture of va loan credit score requirements than a single number ever could. The VA's framework rewards demonstrated financial stability and responsible credit behavior, which means your full credit story matters more than the score sitting at the top of your report.

Why Lenders Set Their Own Minimum Scores

The VA guarantees a portion of each loan it backs, but it doesn't fund the loan itself. Private lenders, including banks, credit unions, and mortgage companies, put up the actual capital. Because they're taking on real financial exposure, they set their own qualification standards on top of the VA's framework. Those internal thresholds are called overlays, and they're the reason two lenders can look at the same borrower and reach completely different decisions.

The Secondary Market Drives Lender Behavior

Most VA loans don't stay with the originating lender. After closing, lenders sell them to investors through the secondary mortgage market, primarily to institutions that package loans into mortgage-backed securities. Those investors have their own risk standards, and lenders design their overlays to match what buyers in the secondary market will accept. A lender that can't sell its loans quickly faces a serious cash flow problem.

The stricter a lender's overlay requirements, the easier it is for that lender to offload loans quickly, which directly affects how aggressively they can price their rates.

Risk Tolerance Varies by Lender

Not every lender sells to the same investors or operates with the same capital reserves. Smaller portfolio lenders who hold their own loans sometimes accept lower credit scores because they control the risk directly. Larger retail lenders tend to apply stricter minimum score thresholds to protect their ability to sell in volume. This is exactly why shopping multiple lenders matters when your score falls below 640, because va loan credit score requirements genuinely differ from one institution to the next. Common thresholds by lender type include:

- Portfolio lenders: may accept scores as low as 580

- Large retail banks: often require 620 to 640

- Mortgage brokers: vary based on their specific investor network

How lenders review your credit for a VA loan

When you apply, the lender pulls a tri-merge credit report that combines data from Equifax, Experian, and TransUnion. Most lenders use the middle score of the three as your qualifying score, not the highest. So if your scores come back at 598, 612, and 634, the lender works with 612. On a joint application with a co-borrower, they typically take the lower of the two middle scores, which can move your qualifying number in either direction.

Reviewing all three of your credit reports before you apply lets you spot outdated negative items or reporting errors that could be dragging down your middle score unnecessarily.

The score is just the starting point

Your credit score tells lenders a quick summary of statistical risk, but underwriters don't stop there. They read the full credit report to understand the pattern behind the number, which is why va loan credit score requirements work differently in practice than a simple cutoff suggests. A 600 with a clean 24-month payment history reads very differently from a 600 with recent missed payments.

Lenders specifically look at how recently negative events occurred and whether your credit behavior has improved over time. Positive trends, like 12 straight months of on-time payments after a rough period, carry real weight during manual underwriting.

What underwriters flag during review

Beyond the score itself, underwriters closely examine specific account behavior over the past 12 to 24 months. The items that most commonly raise concerns include:

- Recent late payments on installment loans or your current rent or mortgage

- High revolving utilization, typically above 30 percent of your credit limits

- Unpaid collections opened or updated within the past 12 months

- Open judgments or tax liens, which usually require resolution before closing

How to qualify with a lower credit score

If your score falls below a lender's overlay threshold, you have real options beyond simply waiting. Understanding va loan credit score requirements at the lender level means you also know which specific levers to pull before you apply. Two actions tend to move the needle fastest: reducing revolving credit utilization and building a clean 12-month payment history across every open account.

Paying down a credit card from 80 percent utilization to under 30 percent can lift your middle score by 20 to 40 points within a single billing cycle.

Target the factors lenders actually weigh

Your payment history accounts for roughly 35 percent of your FICO score, making it the single largest factor in the calculation. Bringing any past-due accounts current before you apply removes a major red flag from your file. Pair that with reducing revolving balances below 30 percent of each card's limit, and you address the two heaviest scoring factors simultaneously. Practical steps to take in the 60 to 90 days before applying include:

- Pay down credit cards to below 30 percent utilization on each individual card

- Bring any delinquent accounts current immediately

- Avoid opening new accounts or generating new hard inquiries

Ask your lender about manual underwriting

Not every lender offers manual underwriting for VA loans, but those that do give you a meaningful advantage when your score sits in a gray zone. Manual underwriting lets an actual underwriter review your full financial picture, including residual income, employment stability, and documented reasons for any negative items, rather than relying entirely on an automated approval system.

Bring written explanations and supporting documents for any derogatory items tied to medical bills or a job loss. Clear documentation shifts the conversation from a number on a report to a complete, honest story of your financial behavior over time.

Credit Score FAQ for VA Borrowers

Veterans and active-duty borrowers ask the same questions about va loan credit score requirements at the start of nearly every application. The answers below cover the most common points of confusion so you walk into your application with clear expectations rather than surprises.

Does checking my credit score hurt my VA loan application?

Checking your own credit through a monitoring service counts as a soft inquiry and has zero impact on your score. When a lender pulls your file during the application process, that registers as a hard inquiry, which may lower your score by a few points. If you apply with multiple VA lenders within a 45-day window, the credit bureaus typically count those pulls as a single inquiry, so shopping around costs you very little.

Limiting your rate shopping to a focused 45-day window protects your score while still giving you enough time to compare multiple lenders.

Can I get a VA loan after bankruptcy?

Yes. A Chapter 7 bankruptcy requires a two-year waiting period from the discharge date before most lenders will consider your application. A Chapter 13 bankruptcy works differently since you may qualify after 12 months of on-time payments within the repayment plan, provided the court trustee approves the new debt.

What if my co-borrower has a lower score?

When you apply jointly, lenders take the lower of the two middle scores as the qualifying number. If your co-borrower's score falls below the lender's overlay threshold, your application gets evaluated at that lower score. In some cases, applying as a single borrower and later adding the co-borrower to title after closing is a workable solution worth discussing with your loan officer.

Next Steps

You now have a complete picture of va loan credit score requirements: the VA sets no minimum, but every lender does, and those thresholds typically fall between 580 and 640. Your job is to know your middle score before you apply, understand which lender overlays fit your profile, and address the two biggest scoring factors, payment history and revolving utilization, in the 60 to 90 days before you submit an application.

If your score already clears the 620 mark, you're ready to start comparing lenders today. If it falls short, the steps in this article give you a clear, focused path to get there without guessing. Either way, working with an experienced loan officer who knows VA loan programs from the inside shortens that path considerably. Connect with David Roa to review your credit profile and find the right VA loan program for your situation.