7 VA Loan Rates Today: 30-Year Vs. 15-Year APRs (2026)

If you're a veteran or active-duty service member shopping for a mortgage, knowing VA loan rates today can save you thousands over the life of your loan. Even a fraction of a percentage point changes what you pay monthly, and what you pay total. Rates shift daily, so having a reliable snapshot matters before you lock in.

Right now in May 2026, VA loan rates sit in a range that reflects broader economic conditions, Fed policy decisions, and lender-specific pricing. The difference between a 30-year and a 15-year fixed VA loan can be significant, not just in monthly payment size, but in total interest paid. Understanding both options puts you in a stronger position to negotiate with any lender. Comparing APRs side by side (not just interest rates) gives you the clearest picture of actual borrowing costs.

At David Roa, we've funded over $150 million in loans across residential, commercial, and investment lending, VA loans included. With more than 25 years originating mortgages, I've guided hundreds of veterans through rate comparisons, helping them choose terms that fit their budget and timeline. This article breaks down seven current VA loan rate offerings across 30-year and 15-year terms, explains what's driving today's numbers, and shows you exactly what to look for when comparing lenders.

1. David Roa mortgage broker rate quote

As a mortgage broker with access to multiple wholesale lenders, I pull quotes from a network of VA-approved lenders rather than working from a single bank's rate sheet. That means when you ask for va loan rates today, I compare live pricing across lenders simultaneously to find the most competitive rate and fee combination for your specific profile.

What you can expect for today's VA loan rates

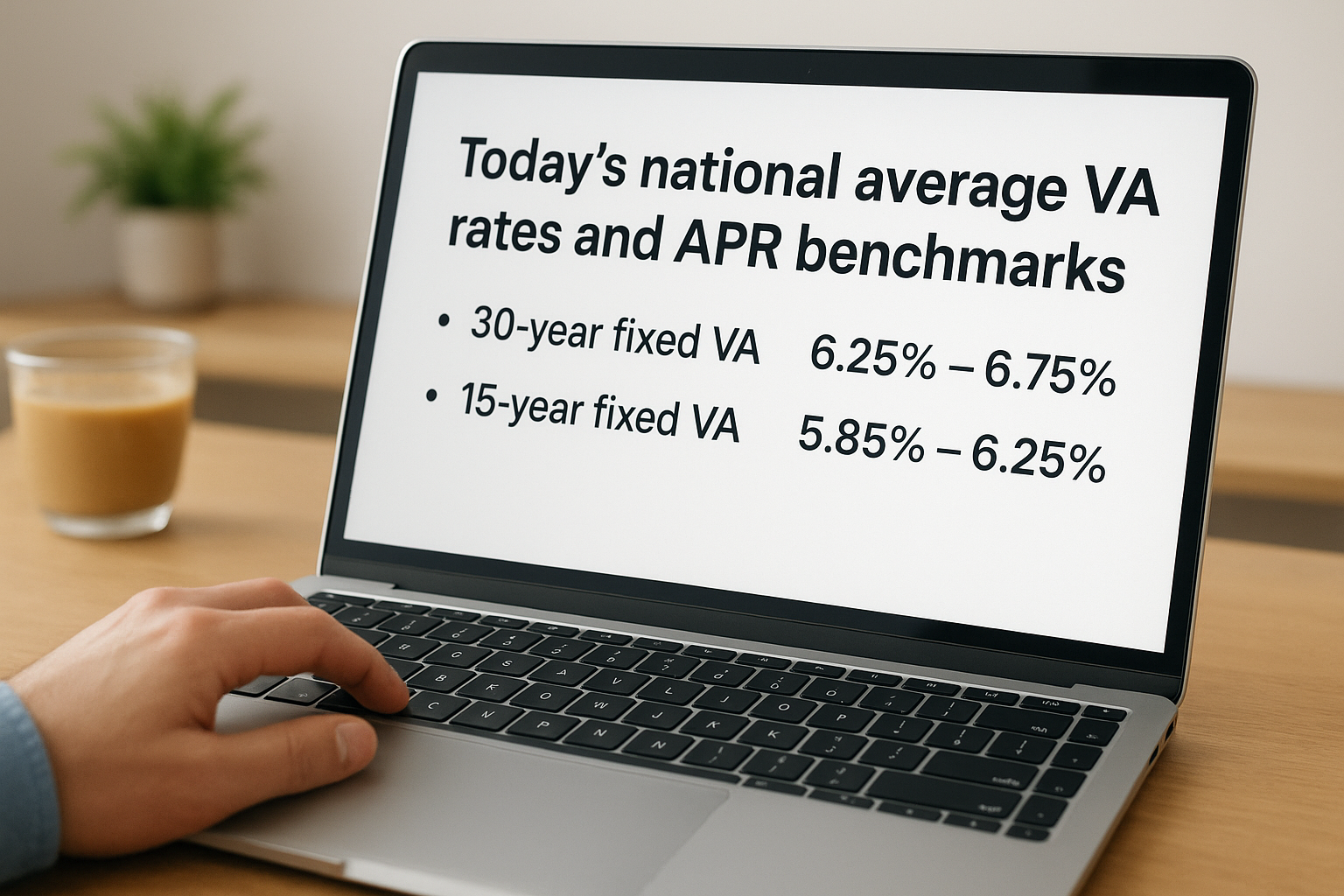

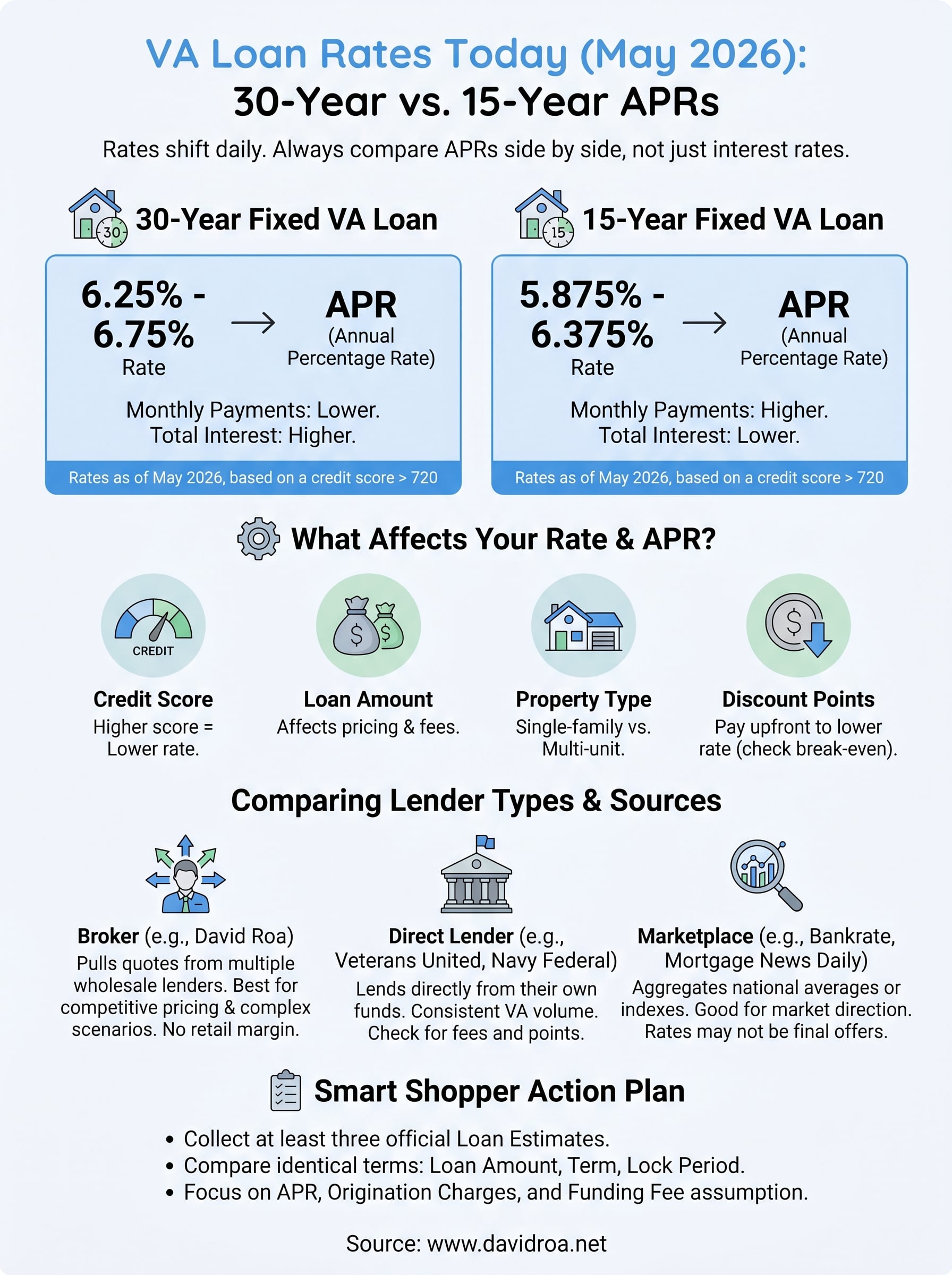

For a well-qualified veteran with a credit score above 720 and a loan amount in the conforming range, today's VA purchase rates through brokered quotes are running between 6.25% and 6.75% on a 30-year fixed and between 5.875% and 6.375% on a 15-year fixed. APRs sit slightly above those figures depending on lender fees and discount points selected. These are live market numbers as of May 2026 and shift with bond markets daily.

A lower rate with a higher APR often signals discount points baked into the quote. Always compare APR, not just the rate.

What affects your rate and APR in a brokered quote

Your credit score, loan amount, and property type are the three biggest variables lenders use to price your VA loan. Beyond those, your remaining VA entitlement and whether you've used a VA loan before affects the funding fee, which rolls into your APR. Lenders also price differently based on how quickly you plan to close and whether you're purchasing or refinancing.

Discount points are another lever. Paying one point upfront (1% of the loan amount) typically buys down your rate by around 0.25%, though this varies by lender. Modeling break-even scenarios lets you know exactly when buying points saves money versus when it costs you more over your expected timeline in the home.

When a broker quote makes the most sense

Broker quotes add the most value when your scenario is anything but straightforward. If you carry a higher debt-to-income ratio, are purchasing a multi-unit property, or need a jumbo VA loan, wholesale lenders often have more flexible overlays than retail banks. Even when your situation is clean, a broker quote still delivers competitive pricing by removing the retail margin that banks layer on top of the same wholesale rate.

How to compare Loan Estimates apples to apples

Federal law requires every lender to issue a Loan Estimate within three business days of receiving your application. That document standardizes costs so you can compare quotes side by side. Focus on Section A (origination charges), the interest rate, the APR, and total closing costs on page 2. Avoid comparing monthly payments in isolation since a lower payment can mask a higher rate stretched across a longer term. Ask every lender to quote the same loan amount, term, and lock period so you're reading the same numbers across every sheet.

2. Veterans United VA loan rates today

Veterans United is one of the largest VA-focused lenders in the country, which means their published rates carry real weight as a market reference point. They serve veterans exclusively through VA products, so their pricing reflects dedicated VA lending volume rather than a general mortgage menu. Checking their posted figures gives you a concrete baseline before you call any lender.

Latest posted 30-year and 15-year VA purchase rates

Veterans United posts daily rate tables on their website, updated each business day. As of May 2026, their 30-year fixed VA purchase rate is running around 6.375% to 6.625%, with a 15-year fixed option typically landing 0.375% to 0.5% below that. APRs shown alongside those figures run slightly higher and reflect their standard fee structure. These numbers assume a qualified borrower with strong credit and sufficient entitlement.

What their APR assumptions and points mean

Veterans United's posted rates often include discount points, which means the advertised rate may not reflect your zero-point cost. Their APR calculations factor in origination fees and the VA funding fee, which adjusts based on your down payment and whether you've used your VA benefit before. A first-time VA borrower putting no money down pays a higher funding fee than a subsequent user, and that difference moves the APR noticeably.

Always ask Veterans United to show you both a zero-point quote and their advertised rate quote so you can calculate your own break-even timeline.

When their posted rates help you benchmark the market

Their published rates help you understand where the market sits today when you're gathering va loan rates today from multiple sources. Because Veterans United handles high loan volume, their pricing tends to track closely with current bond market movements.

What to ask for so the quote matches your scenario

Request a Loan Estimate tied to your actual loan amount and credit profile, not a generic rate table. Ask them to specify the exact points, lender credits, and funding fee assumption built into the quote so you can compare it directly against other lenders using identical terms.

3. Navy Federal Credit Union VA loan rates

Navy Federal Credit Union is the largest credit union in the United States and has a strong track record serving military families. Their VA loan volume gives them consistent pricing power, and their posted rates are worth reviewing when you're comparing va loan rates today across multiple sources.

Latest posted 30-year and 15-year VA rates and APR

Navy Federal's current VA purchase rates as of May 2026 sit around 6.25% to 6.50% on a 30-year fixed, with the 15-year fixed option running roughly 0.375% lower. Their published APRs reflect their standard fee structure and assume a borrower with solid credit history and full VA entitlement. Rates update regularly, so pulling a personalized quote directly from their site gives you a more accurate number than any snapshot.

How discount points and origination fees change the APR

Navy Federal's posted rates sometimes include discount points, which lower the rate upfront in exchange for a higher out-of-pocket cost at closing. Their origination fees and VA funding fee both feed into the APR calculation, which means the gap between the interest rate and APR tells you how much you're actually paying to borrow. A wider gap signals more upfront costs buried in the loan structure.

Ask Navy Federal to show you a zero-point quote alongside their advertised rate so you can calculate which option costs less based on how long you plan to stay in the home.

Eligibility and membership details that impact your options

Navy Federal membership is limited to active-duty military, veterans, Department of Defense personnel, and their immediate family members. You need to establish membership before you can access their loan products, which adds a step that direct lenders skip. Confirm your eligibility before investing time in their application process.

How to use their rate table when shopping other lenders

Their rate table works best as a competitive benchmark rather than a final answer. Pull a Loan Estimate from Navy Federal and compare it against quotes from other VA lenders using the same loan amount, term, and lock period to identify which offer actually saves you more money.

4. USAA VA mortgage rates

USAA serves active-duty military, veterans, and their eligible family members exclusively, which means their mortgage products are built around the needs of the military community. Their VA loan volume and member focus give them consistent pricing, making them a reasonable stop when you're gathering va loan rates today from multiple lenders.

Latest posted VA purchase and refinance rates

USAA's current VA purchase rates as of May 2026 run around 6.375% to 6.625% on a 30-year fixed and approximately 5.875% to 6.25% on a 15-year fixed. Their refinance rates tend to sit slightly higher than purchase rates, reflecting standard industry pricing patterns. APRs displayed alongside those figures include their standard fee structure and assume a borrower with full entitlement and solid credit.

How points and APR work on their posted rates

USAA's advertised rates sometimes include discount points baked in, which reduces the stated rate but increases your upfront closing costs. The gap between their rate and APR tells you how much those costs add to your total borrowing expense. A borrower who plans to stay in the home long-term may benefit from buying points, while someone who expects to sell or refinance within five years often comes out ahead with a zero-point option.

Ask USAA to show you both a zero-point quote and their advertised rate quote so you can calculate your break-even timeline before committing.

When USAA fits best for VA borrowers

USAA works best for borrowers who already bank or carry insurance through USAA, since existing members often experience a smoother application process. Their platform is fully digital, which suits buyers who prefer managing their mortgage without in-person meetings.

What details you need to confirm before you lock

Before you lock your rate, confirm the exact points, lender credits, and funding fee assumption built into your quote. Request a formal Loan Estimate so you can compare their total costs directly against other lenders on identical terms.

5. Bankrate VA loan rates comparison

Bankrate operates as a financial comparison marketplace, aggregating rate data from multiple lenders and publishing national averages daily. When you're researching va loan rates today, their dashboard gives you a broad view of where the market sits across lenders, terms, and credit profiles without requiring you to submit applications anywhere.

Today's national average VA rates and APR benchmarks

Bankrate's national averages as of May 2026 show 30-year fixed VA purchase rates ranging from approximately 6.25% to 6.75%, with 15-year fixed options running roughly 0.40% to 0.50% lower. Their published APRs factor in average fee structures across contributing lenders, giving you a rough baseline for what qualified borrowers are seeing in the current market.

How Bankrate's marketplace quotes differ from direct lenders

Bankrate does not originate loans. Instead, they connect you with participating lenders who bid for your business through their platform. The rates displayed on their comparison tables reflect lender submissions, which means individual lenders choose what they post to attract clicks. Those posted figures may not include all fees, and the actual quote you receive after submitting your information often looks different from the advertised number.

Always pull a formal Loan Estimate from any lender you find through Bankrate before treating their displayed rate as a real offer.

When averages help and when they mislead

National averages work well for understanding broad market direction, but they fall apart when applied to your specific situation. Your credit score, loan amount, and entitlement status all produce a rate that may sit above or below any published average. Averages also blend quotes from lenders with very different fee structures, which makes APR comparisons across the table unreliable for individual decisions.

How to use Bankrate results to negotiate with real quotes

Use Bankrate's data as negotiating context when you talk to direct lenders or a broker. If their table shows the market averaging 6.375% on a 30-year VA loan and a lender quotes you 6.75%, you now have concrete market data to push back with or take elsewhere.

6. Mortgage News Daily VA mortgage rates

Mortgage News Daily tracks daily mortgage rate movements across loan types, including VA loans, using a proprietary survey of lenders and originators. Their data feeds are widely used by industry professionals to follow rate trends in real time. When you're pulling va loan rates today, their index gives you a useful daily reading on where the broader market is moving.

What their daily VA rate index shows today

Mortgage News Daily's VA rate index as of May 2026 shows 30-year fixed VA rates tracking in the 6.35% to 6.60% range for well-qualified borrowers. Their index aggregates pricing signals from multiple lenders, so the number you see reflects a composite market reading rather than a single lender's offer. It updates throughout the day as bond market conditions shift, making it one of the more responsive rate-tracking tools available.

Why an index can move differently than your actual quote

An index captures average market direction, not your personal rate. Your credit score, loan amount, debt-to-income ratio, and VA entitlement status all create pricing adjustments that push your actual quote above or below any index figure. Lender overlays and fee structures add another layer of variation, so two borrowers with similar profiles can still receive meaningfully different rates from the same lender on the same day.

Use the index to understand the direction rates are moving, not as a number you should expect to receive from a lender.

When to use this data for timing and rate locks

Mortgage News Daily's daily tracking helps you spot rate trends over days and weeks, which matters when you're deciding whether to lock or float. If rates have moved lower three days in a row, you have context for a conversation with your lender about timing.

How to pair market tracking with lender-specific APRs

Combine their index data with formal Loan Estimates from at least three lenders to get a complete picture. The index tells you what the market is doing; the Loan Estimate tells you what it actually costs you to borrow from a specific lender on a specific day.

7. PennyMac VA home loan rates

PennyMac is one of the largest mortgage servicers in the country and offers a full suite of VA loan products for both purchases and refinances. Their online platform makes it straightforward to pull initial rate information when you're researching va loan rates today across multiple lenders.

Latest posted VA fixed-rate options and APR

PennyMac's posted VA purchase rates as of May 2026 run approximately 6.375% to 6.625% on a 30-year fixed, with their 15-year fixed option sitting roughly 0.375% to 0.50% lower. Their published APRs reflect standard lender fees and a VA funding fee assumption based on a first-time VA loan user with no down payment. Rates update regularly, so confirm current figures directly through their site before using them for any comparison.

What to watch for in points, credits, and fee structure

PennyMac's advertised rates sometimes include discount points, which lower the stated rate while increasing your closing costs. Their fee structure includes origination charges and the VA funding fee, both of which feed into the APR. A wider spread between the interest rate and the APR signals more upfront costs built into the loan, so always review the full fee breakdown before treating their posted rate as your cost of borrowing.

Ask PennyMac to provide a zero-point quote alongside any advertised rate so you can calculate the break-even point based on your expected time in the home.

When PennyMac may fit versus a local lender or broker

PennyMac fits best when you prefer a fully digital process and want to manage your loan through an established servicer with broad VA lending experience. A local lender or broker may offer more flexibility on complex scenarios or overlays that PennyMac's automated underwriting system handles conservatively.

What to verify in writing before you choose a lender

Request a formal Loan Estimate before you commit to any lender. Confirm the exact points, credits, funding fee assumption, and lock period so you can compare PennyMac's total cost directly against every other quote you've collected using identical loan terms.

Next steps

You now have a clear picture of va loan rates today across seven sources, from a brokered quote to national indexes and direct lenders. The most important move you can make right now is to collect at least three Loan Estimates using identical loan terms so you can compare real costs, not marketing numbers. Focus on APR, origination charges, and the funding fee assumption on each sheet, since those three figures separate a genuinely competitive offer from one that looks good on the surface.

Rates move daily, so your timing matters. If you're ready to act, working with an experienced originator who pulls from multiple wholesale lenders gives you more pricing options than any single bank can offer. With over 25 years of VA lending experience and $150 million funded, David Roa can pull live quotes from competing lenders on your behalf and walk you through every number before you lock. Request your VA loan rate quote today and start comparing real offers.