What Is Down Payment Assistance? Grants Vs. Loans Explained

Saving enough cash to put down on a home is one of the biggest hurdles buyers face, and for many, it's the reason they keep renting instead of building equity. But here's the thing: thousands of buyers close on homes every year without covering the full down payment out of pocket. If you've been asking what is down payment assistance, you're already on the right track. These programs exist specifically to bridge the gap between what you've saved and what you need to get through closing day.

The catch? Not all down payment assistance works the same way. Some programs hand you money you never have to pay back. Others are loans with specific repayment terms that can catch you off guard if you don't read the fine print. Understanding the difference between grants and loans matters, it directly affects your monthly payment, your long-term costs, and your options down the road. Getting this wrong can cost you thousands of dollars over the life of your mortgage.

With over 25 years in the lending business and more than $150 million funded, I've helped first-time buyers, ITIN holders, and families across the Chicago area and nationwide navigate these exact programs. At David Roa, we work through the details with you, matching you to the right assistance program based on your finances, your goals, and the loan product that fits. This article breaks down how down payment assistance actually works, who qualifies, and how to tell whether a grant or a loan makes more sense for your situation.

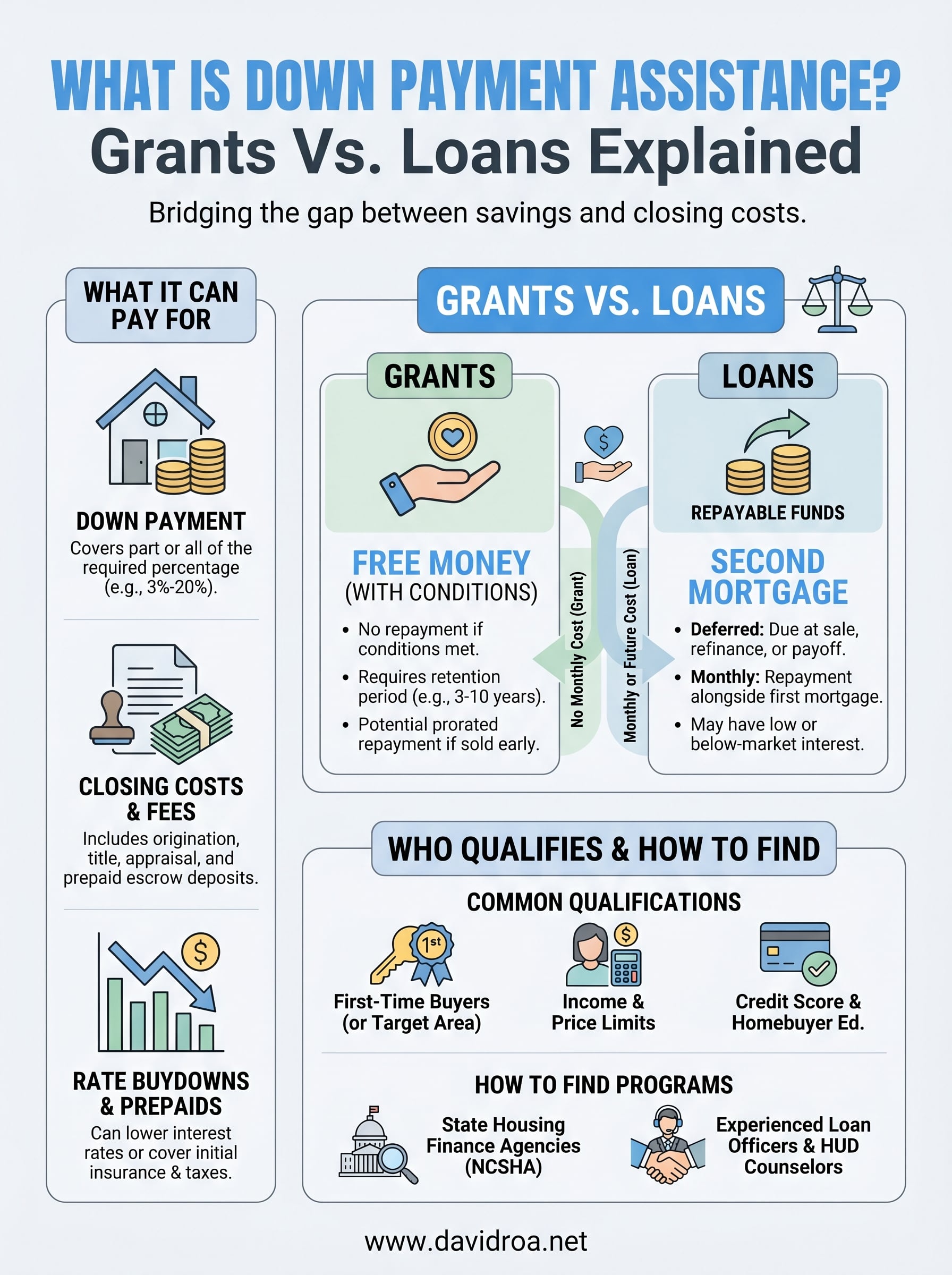

What down payment assistance can pay for

Most buyers assume what is down payment assistance means one thing: money toward the down payment. The reality is that many programs cover more than just that single expense, and understanding the full scope of what assistance can pay for changes how you budget for your home purchase. Getting clear on the details before you apply means fewer surprises at the closing table and a more accurate picture of how much cash you actually need.

The funds from a down payment assistance program can apply to several upfront costs, which could dramatically reduce how much cash you actually need to bring to closing.

The down payment itself

The most straightforward use of assistance funds is toward your actual down payment, the percentage of the purchase price you pay before your mortgage begins. Conventional loans typically require between 3% and 20% down depending on your credit profile and lender requirements, while FHA loans set the minimum at 3.5% for borrowers who meet the credit score threshold. Assistance programs can cover part or all of that required amount. For buyers with steady income but limited savings, this is often the single biggest factor that makes homeownership realistic rather than a goal that keeps getting pushed back another year.

Your loan officer plays a key role here because they can tell you whether a specific program requires you to contribute any of your own funds alongside the assistance, which some programs do as a condition of approval.

Closing costs and fees

Closing costs are a separate line item from your down payment, and they catch a lot of buyers off guard when the final numbers come in. These fees typically run between 2% and 5% of the loan amount and include charges like loan origination fees, title insurance, the appraisal, and prepaid escrow deposits for property taxes and homeowner's insurance.

Many assistance programs allow funds to be applied directly toward these costs. Some programs focus entirely on closing cost relief rather than the down payment itself, which still frees up several thousand dollars you would otherwise need in cash at the closing table. Understanding which costs a specific program covers helps you identify the right match for your actual financial gap.

Rate buydowns and prepaid expenses

Certain assistance programs go further and allow funds to apply toward a mortgage rate buydown, which means paying discount points upfront to lower your interest rate. A lower rate reduces your monthly payment for the life of the loan, so the savings are meaningful over time. Not every program permits this use, and eligibility depends on both the program rules and the lender.

Prepaid expenses like your initial homeowner's insurance premium and the property tax deposit into escrow are also part of your upfront costs. These charges can add several hundred to over a thousand dollars depending on your loan size and local tax rates, and some assistance programs include them in what the funds can cover.

Grants vs loans and how each option works

When you're researching what is down payment assistance, you'll quickly find that programs fall into two main categories: grants and loans. Both reduce how much cash you need at closing, but they work very differently once you own the home. Knowing which type you're receiving before you sign anything is critical because the long-term financial impact can be significant.

The difference between a grant and a loan isn't just about repayment; it determines your total cost of homeownership over time.

How grants work

A grant is free money you don't have to repay, provided you meet the program's conditions. Most grant programs require you to stay in the home for a set period, often called a retention period, which typically ranges from three to ten years. If you sell or refinance before that window closes, you may owe the money back on a prorated basis. After you satisfy the retention period, the grant is fully forgiven and you owe nothing.

Grant amounts vary widely by program and location. Some cover a flat dollar amount, while others provide a percentage of the purchase price, typically between 2% and 5%. Because grants don't add to your debt load, they don't raise your monthly payment, which makes them the more financially favorable option when you qualify.

How down payment loans work

A down payment assistance loan is a second mortgage placed behind your primary loan. These come in two forms: loans that require monthly repayment alongside your first mortgage, and deferred loans where repayment is due only when you sell, refinance, or pay off the home.

The deferred structure sounds straightforward, but the full balance comes due at that trigger point, which can affect how much equity you walk away with. Some assistance loans charge little to no interest, while others carry a below-market rate designed to keep the cost manageable over time.

Who qualifies and common requirements

One of the first questions buyers ask when learning what is down payment assistance is whether they'll actually be eligible. Programs set their own rules, but several core requirements appear consistently across federal, state, and local programs. Meeting those requirements is realistic for many buyers, but you need to know the specific conditions before you apply.

Missing a single eligibility condition can mean restarting the application process with a different program entirely.

First-time buyer status

Most programs define a first-time buyer as someone who hasn't owned a primary residence in the past three years. That means buyers who owned a home years ago but have been renting since can still qualify in many cases. You don't need to be buying your very first home ever to meet this condition.

Some programs drop the first-time buyer requirement entirely if your home sits in a designated target area, which are typically lower-income or revitalization zones identified by the program administrator.

Income and purchase price limits

Programs cap both your household income and the home's purchase price to ensure funds reach buyers who genuinely need them. Income limits are usually set as a percentage of your area median income and vary by county and family size. Purchase price caps also shift by location, with higher ceilings in more expensive markets.

- All household members listed on the loan typically count toward the income total

- Family size can raise your income ceiling in many programs

- Purchase price limits are updated periodically, so confirm current figures when you apply

Credit score and loan type requirements

Most programs set a minimum credit score, commonly 620 to 640, though FHA-backed programs sometimes accept lower scores. Assistance funds are often tied to a specific loan type, such as a conventional or FHA product, so your primary mortgage directly determines which programs you can access.

You also typically need to complete a homebuyer education course before closing, which is usually available online and takes a few hours to finish.

How to find down payment assistance programs

Finding programs that match your situation takes more than a quick online search. Thousands of federal, state, and local programs exist across the country, and availability shifts regularly as funding gets allocated or depleted. Knowing where to look first saves you time and puts you in front of the options most likely to fit your income, location, and loan type.

Start with your state housing finance agency

Every state has a housing finance agency that administers down payment assistance and affordable mortgage programs for residents. These agencies are your most reliable starting point because they manage programs with consistent funding, clear eligibility rules, and lender partnerships that make the application process smoother. You can find your state's agency through the National Council of State Housing Agencies directory.

Your state agency often offers both assistance programs and access to below-market interest rates on your primary mortgage, which can stack additional savings on top of down payment help.

Beyond your state agency, HUD-approved housing counseling agencies offer free or low-cost guidance on programs available in your specific county or city. You can locate a HUD-approved counselor at HUD.gov, and these counselors are trained to match you with programs based on your full financial picture.

Work with an experienced loan officer

A knowledgeable loan officer is often your most practical resource for tracking down current assistance programs. Lenders who specialize in first-time buyer financing stay updated on which programs are open, what the income limits are, and which ones pair with the loan products they originate. That combination of loan and assistance program knowledge is hard to replicate by searching on your own.

Part of what is down payment assistance searching requires is understanding which programs work with your specific mortgage type, and a loan officer handles that matching process on your behalf from the start.

How to apply and avoid common pitfalls

Applying for down payment assistance follows a clear sequence, but the process moves faster when you come prepared. Your loan officer typically coordinates the application alongside your primary mortgage, which means you're not running two separate processes. Understanding what is down payment assistance on paper is one thing; executing the application correctly under a deadline is another. Most buyers who run into trouble do so not because they were ineligible, but because they were unprepared.

Getting your documents organized before you start the application is the single fastest way to avoid delays that could cost you a home.

Get your documents ready before you apply

Programs require documentation to verify your income, identity, and financial profile, and missing a single item can pause your application for days. Gathering these materials upfront keeps your timeline intact and reduces back-and-forth with the program administrator.

- Two years of federal tax returns and W-2s

- Recent pay stubs covering the last 30 days

- Bank statements from the last two to three months

- Government-issued photo ID

- Proof of homebuyer education course completion, if required by the program

Avoid these common mistakes

One of the most frequent problems buyers run into is depositing large sums of cash into their bank accounts shortly before applying. Underwriters flag unexplained deposits, and a sudden influx of money can raise questions that delay or derail both your assistance application and your primary mortgage approval. Keep your financial activity consistent and document any legitimate transfers or gifts thoroughly before they land in your account.

Another mistake is applying for new credit during the process. Opening a new credit card or taking out a car loan after your application is submitted can lower your credit score and shift your debt-to-income ratio enough to disqualify you. Hold off on any new credit until after your closing is complete.

Next steps

Now that you understand what is down payment assistance and how grants differ from loans, the next move is connecting with a lender who can tell you exactly which programs you qualify for today. Eligibility rules, income limits, and funding availability all shift regularly, so waiting too long can mean missing a program that's a strong fit for your situation. The buyers who close fastest are the ones who get their documents together and talk to a loan officer before they start shopping for a home.

Your specific income, credit profile, and target location determine which programs stack with your loan type and how much assistance you can actually access. At David Roa, we work through those details with you directly, matching your situation to the right loan and assistance combination from day one. If you're ready to move forward, connect with a mortgage expert at David Roa and let's map out your path to closing.