What Is a HomeStyle Renovation Loan? Requirements & Steps

You found a house with great bones but outdated everything, kitchen, bathrooms, maybe the roof. You could buy it, then apply for a separate renovation loan, juggling two closings, two sets of fees, and two approval processes. Or you could roll the entire project into one mortgage. That's exactly what a HomeStyle renovation loan is designed to do.

Backed by Fannie Mae, the HomeStyle loan lets you finance the purchase price (or refinance your current home) plus the cost of renovations in a single loan. It covers everything from structural repairs to luxury upgrades, with no restriction on the type of improvement as long as it's permanently affixed to the property. For buyers eyeing a fixer-upper or homeowners sitting on untapped equity, it's one of the most flexible renovation financing options available, and one that most borrowers don't know exists.

At David Roa, we've helped clients across Chicago and nationwide use HomeStyle loans to turn undervalued properties into exactly what they need, whether that's a primary residence, a second home, or an investment property. With over 25 years in lending and $150 million-plus funded, we know where these loans shine and where they get complicated. This guide breaks down the eligibility requirements, the step-by-step process, and the practical details you need before you apply.

Why a HomeStyle renovation loan matters

A significant share of the housing market is made up of properties that need work. These homes sit below market value precisely because most buyers either lack the cash to renovate after closing or can't qualify for a second loan on top of their mortgage. The HomeStyle renovation loan closes that gap by treating the purchase and the renovation as one financial package, making properties accessible that would otherwise stay out of reach for most buyers.

The problem with buying a fixer-upper the traditional way

When you buy a distressed property with a standard mortgage, the lender bases the loan on the home's current value, not its potential. That means if the home needs $80,000 in work, you need $80,000 in cash sitting in a bank account after closing, which most buyers simply don't have. Some turn to personal loans or home equity lines of credit, but those options carry higher interest rates, shorter repayment terms, and separate monthly payments that strain your cash flow every month.

Others try to sequence a purchase loan followed by a home equity loan once they've built enough value through the renovation itself. The problem is that a freshly purchased home rarely has the equity to support a second loan right away. You end up stuck: you need the renovation to build value, but you need the value to fund the renovation.

Most borrowers don't realize they can finance both the purchase and the full renovation costs at once with a single loan and one monthly payment.

What this loan unlocks for buyers and homeowners

Understanding what is a HomeStyle renovation loan matters because it reframes how you look at the housing market entirely. Instead of filtering out every property that needs a new roof, a kitchen gut, or updated electrical, you can factor those costs into the loan and still close with one mortgage. That shifts your search from a competitive pool of move-in-ready homes to a much broader universe of undervalued properties where you have real negotiating power on price.

For current homeowners, the HomeStyle loan works as a refinance tool. If you have equity in your home and want to renovate, you can refinance your existing mortgage into a new HomeStyle loan that wraps both the remaining balance and the renovation budget into one payment. That's a cleaner option than a home equity loan or line of credit, especially when the blended rate ends up close to what you're already carrying on your mortgage.

Real estate investors benefit here too. The HomeStyle loan allows financing on investment properties, which is a key advantage over the FHA 203k, a competing renovation product that's limited to owner-occupied homes only. If you're building a rental portfolio or planning a fix-and-hold strategy, this loan gives you a structured way to fund both the acquisition and the work needed to make the property cash-flow positive.

The bottom line is that this loan creates options where most traditional financing creates dead ends. Whether you're a first-time buyer targeting an affordable fixer-upper, a homeowner ready to finally renovate, or an investor looking for a more flexible funding structure, the HomeStyle renovation loan is worth understanding before you default to a less efficient alternative that costs you more in fees, time, and missed opportunity.

How a HomeStyle renovation loan works step by step

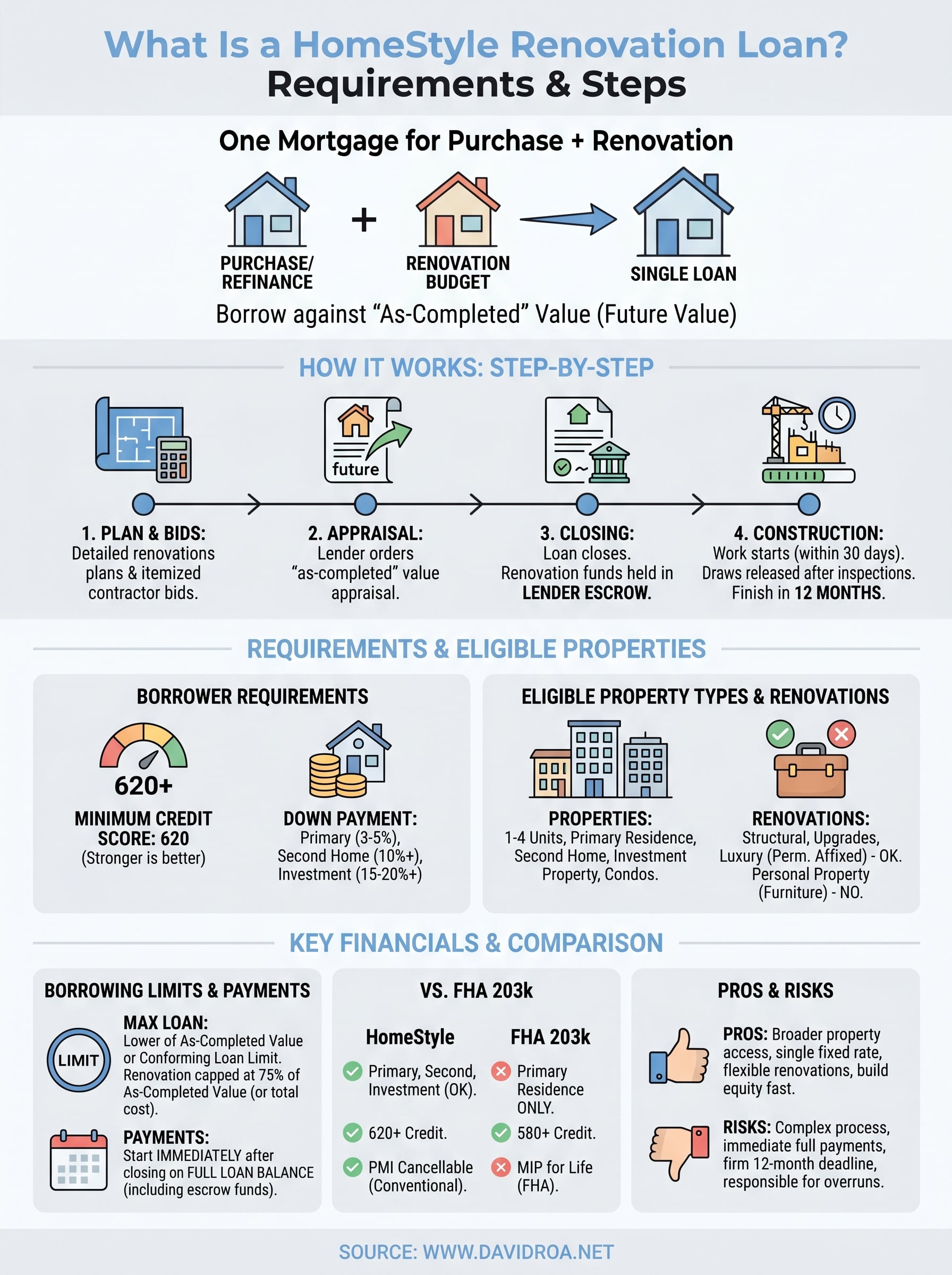

The mechanics of a HomeStyle renovation loan differ from a standard mortgage in one critical way: you're borrowing against the future value of the property, not its current condition. Your lender orders an appraisal based on the proposed renovation plans, and that "as-completed" value becomes the foundation for how much you can borrow. Once you close, the funds don't flow directly to you. Instead, they sit in a renovation escrow account controlled by the lender and get released in draws as work progresses.

Finding a lender and getting your plans in order

Before you apply, you need detailed renovation plans and contractor bids ready to submit. Your lender uses these documents to order the as-completed appraisal, so vague estimates won't work here. You'll need a licensed contractor to provide itemized cost breakdowns for every phase of the project. Fannie Mae requires the lender to review and approve the contractor before work starts, so factor that into your timeline.

Once your lender approves the plans, you move through standard mortgage underwriting: income verification, credit review, and asset documentation. The key difference is that the renovation budget gets added to your loan amount and held in escrow at closing. You do not write checks to contractors out of pocket while waiting for reimbursement; the lender manages those disbursements directly on your behalf.

The lender controls the renovation funds through an escrow account, which protects both you and the project from cost overruns and contractor disputes.

How draws work once construction begins

After closing, your contractor starts work and requests draw payments from the escrow account at agreed project milestones. Most lenders require an inspection before releasing each draw to confirm that completed work matches what was planned and paid for. This protects you from paying for incomplete work and gives the lender confidence that the collateral is gaining value at each stage.

Fannie Mae sets a 12-month window from closing to complete all renovations. If your project runs over budget, you typically cannot request additional loan funds; overages usually need to come from your own cash reserves. This makes submitting accurate contractor bids upfront one of the most consequential decisions you'll make in the entire process, not just a formality.

Borrower requirements to qualify

Understanding what is a HomeStyle renovation loan is only half the equation; you also need to know whether you qualify before you start submitting plans and contractor bids. Fannie Mae sets the baseline eligibility standards, but your individual lender may apply additional overlays on top of those. The requirements here are comparable to a conventional mortgage, which means strong credit and stable income carry more weight than they would with an FHA product, and your documentation needs to be complete before you apply.

Credit score and down payment minimums

Fannie Mae requires a minimum credit score of 620 to qualify for a HomeStyle renovation loan. In practice, lenders offer better rates the higher your score sits above that floor, so borrowers in the 680 to 740 range and above will see meaningfully lower rates over the life of the loan. Your down payment depends on how you plan to use the property. For a primary residence, you can put down as little as 3% if you're a first-time homebuyer, or 5% otherwise. Second homes require at least 10% down, and investment properties typically require 15% to 20% depending on the lender's internal guidelines.

Your credit score affects not just your approval odds but the interest rate you carry for the entire loan term, so reviewing your credit report before you apply is time well spent.

For refinance scenarios, Fannie Mae allows you to borrow up to 97% of the as-completed value on a primary residence. That gives you real borrowing power if you have existing equity and a solid renovation plan already priced out.

Income, debt, and employment standards

Your lender will verify your income using W-2s, tax returns, and recent pay stubs going back at least two years. Self-employed borrowers need to provide two years of both business and personal tax returns, and lenders will average your net income across both years to calculate qualifying income. Your debt-to-income ratio must generally stay at or below 45%, though some lenders allow up to 50% with compensating factors like strong cash reserves or a high credit score.

Employment history carries real weight in underwriting. Lenders look for two consecutive years of employment in the same field, and recent job gaps or career changes can complicate your approval. Bring complete documentation from the start and flag any income irregularities to your loan officer early, because last-minute surprises in underwriting are what push timelines off track.

Property and renovation rules you must follow

Not every property qualifies for a HomeStyle loan, and not every renovation project fits within Fannie Mae's guidelines. Before you lock in a contractor bid or make an offer on a property, you need to confirm that both the property type and the scope of work meet the program's requirements. Getting this wrong early in the process can stall your approval or force you to restructure your loan at a point where your options are limited.

Which property types are eligible

The HomeStyle loan covers a broader range of property types than many borrowers expect. Fannie Mae permits financing on 1- to 4-unit primary residences, second homes, and investment properties, as well as condominiums that meet standard Fannie Mae project guidelines. Manufactured homes are also eligible under specific conditions, though individual lenders may apply additional overlays for that property type. The key distinction is that the property must be residential in nature, meaning pure commercial buildings fall entirely outside the program's scope, even if you're financing other investment properties through the same lender.

If you're financing an investment property with a HomeStyle loan, confirm with your lender early that the property meets Fannie Mae's eligibility standards before ordering the appraisal.

What renovations qualify and what to watch for

Understanding what is a HomeStyle renovation loan also means knowing which improvements the program actually covers. Fannie Mae allows a wide range of projects, from structural repairs and kitchen remodels to landscaping, energy-efficient upgrades, and even luxury additions like in-ground pools, as long as the improvement is permanently affixed to the property. That flexibility is one of the program's strongest advantages compared to more restrictive renovation financing products.

What you cannot do is use the funds for work that isn't tied to the property itself. Purchasing freestanding appliances, furniture, or personal property does not qualify under the program. The renovation must add permanent value to the real estate, and your lender will verify this through inspections at each draw stage. Beyond eligible costs, Fannie Mae requires that all work begin within 30 days of closing and be fully completed within 12 months. If your project is large or your contractor has a packed schedule, build those timelines into your planning before you close, not after the funds are already sitting in escrow.

How much you can borrow and how appraisals work

Grasping what is a HomeStyle renovation loan comes down to understanding one key mechanic: your borrowing limit is based on the as-completed appraised value of the property, not what it's worth in its current condition. That distinction gives you real borrowing power on distressed or undervalued properties because the loan is built around the home's projected value after renovation, not the price tag on the listing.

How the as-completed appraisal sets your ceiling

Your lender orders an appraisal before closing, and the appraiser uses your contractor's plans and itemized cost estimates to project what the property will be worth once every improvement is finished. That as-completed value is the number your maximum loan amount derives from. Because of this, the quality of your renovation plans matters as much as your credit score at this stage. A vague scope of work gives the appraiser less to work with, which leads to a conservative projection and a lower borrowing ceiling, even if your contractor bids are reasonable and well-supported.

The detail in your renovation plans directly shapes the appraised value projection, which controls how much financing ends up available to you.

Fannie Mae caps your total loan at either the as-completed appraised value or the conforming loan limit for your county, whichever is lower. For 2025, the baseline conforming limit is $806,500 for a single-unit property in most markets, with higher limits in designated high-cost areas. If your total project value pushes above that threshold, you would need to explore jumbo renovation financing as an alternative path.

How the renovation budget fits into the total loan

Your renovation budget gets added directly to the purchase price or existing loan balance to calculate the total loan amount you're requesting. Fannie Mae limits the renovation portion to the lesser of 75% of the as-completed appraised value or the actual total cost of the renovation work. That cap matters because if the appraisal comes in conservatively, your renovation escrow gets trimmed even when your contractor bids are accurate and market-supported.

For homeowners refinancing a primary residence, Fannie Mae permits borrowing up to 97% of the as-completed value, which gives you substantial capacity to fund large projects when you already hold equity in the property. Getting a thorough, well-documented appraisal is how you protect that capacity from the start.

What it costs and how payments work during renovation

One of the most important practical details to understand about what is a HomeStyle renovation loan is that your payments start immediately after closing, covering the full loan amount, including the funds still sitting in the renovation escrow account. You are not paying only on the portion already disbursed to your contractor. From day one, interest accrues on the entire loan balance, which is a cost most borrowers don't factor into their monthly budget before they apply, and it can create real strain if you're also paying rent or carrying another housing expense during the renovation period.

Interest rates, fees, and contingency reserve requirements

HomeStyle renovation loans are conventional products, so they carry interest rates that track standard conforming mortgage rates rather than the higher rates associated with FHA products or private renovation financing. Your actual rate depends on your credit score, loan-to-value ratio, and the lender's own pricing, but borrowers with strong credit can often secure rates close to what they'd receive on a standard conventional mortgage. Lenders may also charge a slightly higher origination fee given the added complexity of managing the renovation escrow and draw process, so request a full loan estimate early and compare it line by line.

Fannie Mae also requires a contingency reserve of at least 10% of the total renovation cost, held in escrow to cover unexpected overruns. Some lenders push that requirement to 15% for larger or more complex scopes of work. That reserve is part of your total loan balance from closing, so it raises your monthly payment even if you never touch the funds. Any unused contingency money at the end of the project gets applied directly to your principal balance, which works in your favor over the long term.

Your contingency reserve is part of your loan balance from day one, which means it affects your monthly payment whether you use it or not.

Private mortgage insurance and how it comes off

If your down payment is less than 20% of the as-completed value, you will pay private mortgage insurance on a HomeStyle loan, the same as you would on any conventional mortgage. The advantage over FHA mortgage insurance is that PMI on a conventional loan is cancellable once your loan-to-value ratio reaches 80%, either through scheduled paydown or through an appraisal confirming that your renovation increased the property's value enough to hit that threshold. That gives you a defined and reachable exit point, which is a meaningful long-term savings compared to FHA products where mortgage insurance often stays in place for the life of the loan.

Pros, cons, and risks to watch for

Knowing what is a HomeStyle renovation loan means understanding not just how it works, but where it fits your situation and where it creates problems. This product offers genuine advantages over most alternatives, but the structure also introduces real financial exposure that borrowers who focus only on the approval process tend to miss until they're already in the middle of a renovation.

Where this loan genuinely works in your favor

The most compelling advantage is access to a broader property market. You can make competitive offers on homes that other buyers walk away from because the renovation costs price them out. You negotiate from a position of strength on distressed properties, and you build equity faster when the renovation adds more value than it costs to complete. For investors, the ability to finance 1- to 4-unit investment properties with a single loan structure separates the HomeStyle from FHA renovation products entirely.

The combination of flexible property eligibility and a wide renovation scope makes the HomeStyle loan one of the most versatile renovation financing tools available through a conventional mortgage channel.

Refinancing homeowners benefit from locking renovation costs into a fixed conventional mortgage rate rather than layering a home equity line of credit on top of an existing loan. You eliminate the second monthly payment and the variable rate exposure that comes with most home equity products.

Where the loan creates friction and real risk

The complexity is real. You're managing a standard mortgage underwriting process and a renovation project simultaneously, and both require detailed documentation from the start. If your contractor bids are inaccurate, the appraisal comes in lower than you need, or the renovation scope expands after closing, you absorb those overruns out of pocket. The 12-month completion deadline is firm, and lenders rarely have flexibility if your project runs long because of permitting delays or contractor scheduling conflicts.

You also start paying interest on the full loan balance at closing, including funds still held in escrow. If your renovation takes six months, you carry the full payment during that entire period whether you're living in the property or not. Borrowers who underestimate that carrying cost often feel the financial pressure mid-project when their cash reserves are already committed. Build that cost into your budget before you submit an application, not after you've already closed.

HomeStyle vs FHA 203k and other financing options

Once you understand what is a HomeStyle renovation loan, the next question is whether it's actually the right tool for your situation. Several renovation financing products exist, and each one serves a different borrower profile. Choosing the wrong one doesn't just cost you money in fees; it can slow your project down or limit how much you can borrow based on property type restrictions you didn't see coming.

HomeStyle vs FHA 203k

The FHA 203k is the most direct competitor to the HomeStyle loan, and the two programs share a similar structure: one loan covering purchase and renovation costs, with funds held in escrow and released as work progresses. The differences, though, matter significantly depending on your circumstances. The 203k is limited to owner-occupied primary residences, which rules it out entirely for investors or anyone financing a second home. The HomeStyle loan covers all of those property types.

If you're buying an investment property or a second home, the FHA 203k is not available to you; the HomeStyle loan is your primary conventional renovation option.

Credit requirements also diverge. The FHA 203k accepts credit scores as low as 580 with a 3.5% down payment, which makes it more accessible for borrowers with weaker credit histories. The HomeStyle requires a minimum score of 620 and generally rewards stronger credit with noticeably better rates. On mortgage insurance, the FHA 203k charges both an upfront premium and an annual premium that typically runs for the life of the loan, while HomeStyle PMI cancels once you reach 80% loan-to-value, which saves you money over time if your credit supports the HomeStyle qualification threshold.

HomeStyle vs cash-out refinance and personal loans

A cash-out refinance lets you pull equity from your home and use those funds however you choose, including renovations, but it doesn't tie the renovation costs to the project the way HomeStyle escrow does. That freedom can work against you if your contractor timelines slip or your project scope expands, because the funds are already in your account with no structural safeguard keeping the renovation on track.

Personal loans and home equity lines of credit carry higher interest rates, shorter repayment terms, and separate monthly payments that add to your debt load immediately. Neither product lets you borrow against the as-completed value of the property, which means your borrowing capacity stays anchored to current equity rather than what the home will be worth after renovation. For large projects, that gap in borrowing power is substantial.

How to apply and what the timeline looks like

Applying for a HomeStyle renovation loan follows the same basic path as a conventional mortgage, but the preparation phase is longer because you need contractor bids and renovation plans ready before your lender can even order the appraisal. Rushing that early documentation is one of the most common reasons applications stall or result in a loan amount lower than the borrower needed. Start organized, and the process moves in a straight line.

Steps to take before you submit your application

Before you contact a lender, you need to do groundwork that most mortgage applicants skip. Understanding what is a HomeStyle renovation loan makes clear that the renovation scope is as important to your approval as your credit file, so treat both with equal preparation.

Here's the sequence that sets you up to move efficiently:

- Pull your credit report from all three bureaus and resolve any errors before applying.

- Define your renovation scope clearly and get itemized bids from at least two licensed contractors.

- Gather your financial documents: two years of tax returns, W-2s, recent pay stubs, and bank statements.

- Compare lenders who actively originate HomeStyle loans, since not every conventional lender participates in the program.

- Submit your application along with the contractor bids, so your lender can order the as-completed appraisal immediately.

Getting your contractor bids locked in before you apply shortens your total timeline by weeks because the appraisal cannot start without them.

What the timeline looks like from application to renovation completion

From the point you submit a complete application with contractor documentation attached, most HomeStyle loans close within 30 to 45 days, though that window stretches closer to 60 days if the appraisal requires multiple revision cycles or underwriting requests additional documentation. Factor that timing into any purchase contract you sign and negotiate a realistic closing date with the seller upfront rather than asking for an extension mid-transaction.

Once you close, your contractor must begin work within 30 days and finish the entire project within 12 months. Lenders release draw payments at project milestones after an inspector confirms the completed work, so your contractor's scheduling discipline affects how smoothly funds flow throughout the renovation. Build buffer into your renovation plan for permitting delays or material lead times, because the 12-month deadline does not flex regardless of what causes the slowdown.

Conclusion

Now you understand what is a HomeStyle renovation loan and how it works from the appraisal stage through the final draw payment. This loan gives you a structured way to buy or refinance a property and fund the full renovation in one mortgage, with one closing and one monthly payment. That simplicity translates to real financial advantages over juggling a purchase loan with a separate line of credit or personal loan.

The details matter here. Your contractor bids, credit profile, and renovation timeline all affect how much you can borrow and whether your project stays on track within the 12-month completion window. Getting those pieces organized before you apply separates a smooth closing from a drawn-out process.

If you're ready to explore whether this loan fits your situation, connect with David Roa for a direct conversation. With 25 years of experience and $150 million funded, we can tell you quickly what you qualify for and how to move forward.