Apply For A VA Loan: 7 Steps From Eligibility To Closing

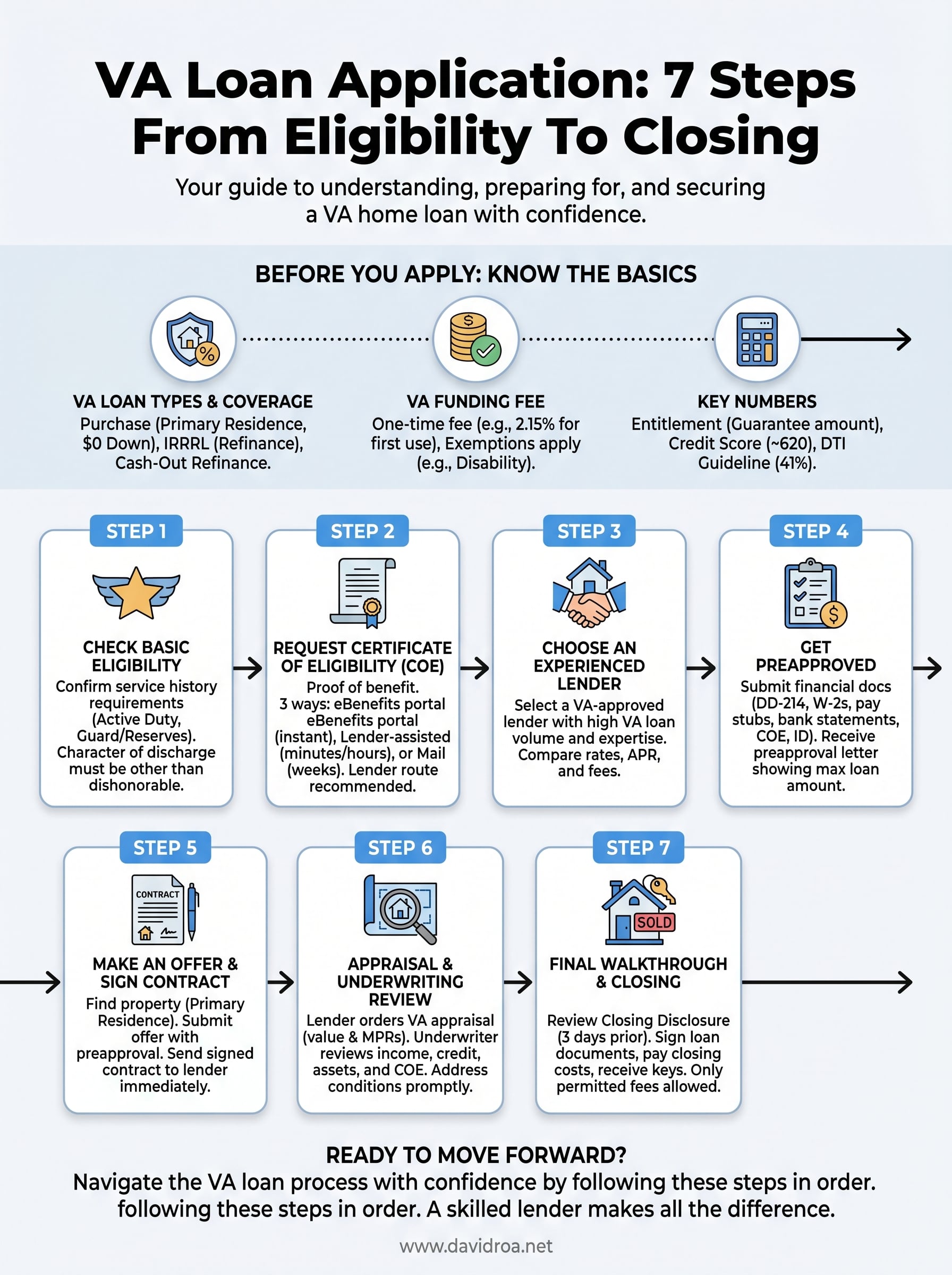

If you've served in the military, the VA loan is one of the strongest mortgage benefits available to you, no down payment, no private mortgage insurance, and competitive interest rates. But knowing those perks exist and actually knowing how to apply for a VA loan are two different things. The process has specific steps that, when done in order, keep your home purchase on track and on time.

This guide breaks down the seven steps from confirming your eligibility to sitting at the closing table. You'll learn how to get your Certificate of Eligibility, what documents to gather, and how to choose a lender who actually understands VA lending, because not every lender does it well or often enough to avoid costly delays.

At David Roa, we've helped veterans and active-duty service members secure VA financing as part of the over $150 million in loans we've funded across more than 25 years in the mortgage industry. Whether you're buying your first home or your fourth, here's exactly how the VA loan process works from start to finish.

What you need to know before you apply

Before you start gathering documents or calling lenders, understanding how the VA loan program actually works saves you time and prevents surprises later in the process. The VA does not lend you money directly. Instead, the Department of Veterans Affairs guarantees a portion of the loan made by a private lender, which reduces the lender's risk and allows them to offer you better terms than a conventional mortgage. That guarantee is the reason you can buy a home with zero down payment and no private mortgage insurance requirement.

VA loan types and what they cover

Not every VA loan works the same way, and knowing which type fits your situation helps you ask the right questions when you apply for a VA loan. The most common option is the VA purchase loan, which lets you buy a primary residence with no down payment. You also have access to the VA Interest Rate Reduction Refinance Loan (IRRRL) if you already hold a VA loan and want to lower your rate, or a VA cash-out refinance if you want to tap the equity in a home you own.

| Loan Type | Purpose | Down Payment |

|---|---|---|

| VA Purchase Loan | Buy a primary residence | $0 |

| VA IRRRL (Streamline Refinance) | Lower your rate on an existing VA loan | $0 in most cases |

| VA Cash-Out Refinance | Access equity or convert a non-VA loan | $0 |

| VA Native American Direct Loan | Purchase on Federal Trust Land | $0 |

The VA loan benefit applies only to primary residences. You cannot use it to purchase a vacation property or a standalone investment rental property.

The VA funding fee

The VA funding fee is a one-time charge the government uses to keep the loan program running, and almost every borrower pays it. The fee percentage depends on your service type, your down payment amount, and whether you are using the benefit for the first time or a subsequent time. For a first-time use with no down payment, the fee is currently 2.15% of the loan amount for most veterans and active-duty service members. You can pay it at closing or roll it into the loan balance.

Some borrowers are exempt from the funding fee entirely. If you receive VA disability compensation, you are a surviving spouse of a veteran who died in service or from a service-connected disability, or you have a pre-discharge disability rating, you do not owe the fee. Confirm your exemption status before closing so your lender removes the charge from your loan estimate.

Key numbers that affect your loan

Entitlement is the dollar amount the VA will guarantee on your behalf, and it directly shapes how much you can borrow without a down payment. Most veterans with full entitlement have no loan limit, meaning the lender sets the ceiling based on your income and credit profile rather than a hard VA cap. If you have used your benefit before and not fully restored it, you may have reduced entitlement, which can require a down payment on higher-priced homes.

Two other numbers matter before you reach out to a lender. First, your credit score: the VA sets no official minimum, but most VA-approved lenders require at least a 620 FICO score. Second, your debt-to-income ratio (DTI): the VA guideline sits at 41% or below, though lenders can approve higher DTI with strong compensating factors like significant cash reserves. Knowing both numbers before your first lender conversation puts you in a stronger starting position.

Step 1. Check basic VA eligibility

Eligibility for a VA loan is tied to your military service history, and the requirements vary depending on when you served and in what capacity. Before you apply for a VA loan or contact any lender, confirm you meet the baseline service criteria so you know exactly where you stand. Skipping this step can stall your application later when the lender requests documentation you haven't pulled together.

Service requirements by category

Your eligibility category determines the minimum length of service the VA expects. Active-duty veterans, National Guard members, and reservists each follow different rules, and the exact dates of your service period matter. Review the table below to identify which category applies to you.

| Service Category | Minimum Service Requirement |

|---|---|

| Active Duty (wartime) | 90 consecutive days |

| Active Duty (peacetime) | 181 continuous days |

| National Guard / Reserves | 6 years of service |

| National Guard / Reserves (activated under federal orders) | 90 days under Title 10 or Title 32 |

| Surviving Spouse | Veteran died in service or from a service-connected disability |

Surviving spouses who have not remarried may also qualify, provided the veteran met the service standards above. In that case, your DD-214 or a Statement of Service letter from your commanding officer is the primary eligibility document you will need.

Character of discharge

The VA requires that your discharge be under conditions other than dishonorable. An honorable discharge or a general discharge under honorable conditions qualifies you without any additional review process. Other than honorable (OTH) discharges require a character of discharge review by the VA before your eligibility is confirmed, which adds time to the process.

If your discharge status is anything other than honorable, submit a character of discharge review request before you do anything else. Waiting until mid-application creates delays that can cost you a home contract.

You can start that review by submitting VA Form 21-4138 (Statement in Support of Claim) to your regional VA office. This step sits completely outside the Certificate of Eligibility process and should be completed first if it applies to your situation.

Step 2. Request your Certificate of Eligibility

Your Certificate of Eligibility (COE) is the official document that proves to a VA-approved lender that you meet the service requirements for the VA loan benefit. Without it, no lender can move forward with your application. The good news is that getting your COE is usually faster than most veterans expect, and you have three separate routes to request it depending on your situation and how quickly you need it.

Three ways to get your COE

Each method works, but the time to receive your certificate differs significantly depending on which path you take. Review the options below and pick the one that matches your timeline.

| Method | How It Works | Typical Turnaround |

|---|---|---|

| VA eBenefits Portal | Log in at eBenefits.va.gov, navigate to Benefits, and request your COE online | Instant in many cases |

| Through your lender | Most VA-approved lenders access the VA's Web LGY system and pull your COE directly | Minutes to a few hours |

| By mail | Complete VA Form 26-1880 and mail it with your DD-214 to your regional VA loan center | Several weeks |

The lender-assisted route is the most practical option if you are already working with a VA-approved lender. Your loan officer can pull the COE before you even gather all your financial documents, which keeps the process moving without extra steps on your end.

Request your COE through your lender first. If the automated system cannot locate your records, you still have time to gather paper documentation without stalling your purchase timeline.

What to do if your COE shows issues

Sometimes the COE comes back with a reduced entitlement amount because you have a prior VA loan that has not been paid off or restored. This does not automatically disqualify you, but it does affect how much you can borrow without a down payment. Your lender can walk you through the numbers to calculate your remaining entitlement and whether a down payment covers the gap.

If your service records are incomplete or missing, contact the National Personnel Records Center (NPRC) directly to request a copy of your DD-214 before you apply for a VA loan again. Incomplete records are the most common reason COE requests stall, and getting ahead of that problem takes the pressure off your closing date.

Steps 3–4. Choose lender and get preapproved

With your COE in hand, you're ready to find a lender and get your preapproval letter. Not every lender handles VA loans with the same level of skill or frequency, and choosing the wrong one can introduce delays, miscommunication, or unexpected fees that slow your purchase. These two steps happen nearly in parallel, so moving on both at once keeps your timeline tight.

Step 3. Find a VA-approved lender who does this regularly

Any lender on the VA's approved list can technically process your loan, but volume and experience matter significantly. A loan officer who closes VA loans every week understands how to handle VA appraisals, how to document military service income correctly, and how to communicate with the VA when problems arise. Ask each lender you contact how many VA loans they closed in the last 12 months before you commit.

A lender with limited VA experience may misapply the funding fee exemption, miscalculate your entitlement, or miss a step in the appraisal process, all of which push your closing date back.

When you compare lenders, focus on three specific numbers: the interest rate, the annual percentage rate (APR), and the lender fees listed on the Loan Estimate. The APR accounts for lender fees and gives you a more accurate comparison point than the rate alone.

Step 4. Submit your preapproval documents

Preapproval requires you to submit a standard set of financial documents so the lender can verify your income, assets, and credit. Pulling these together before you formally apply for a VA loan saves you significant time once you find a property you want to purchase. Use this checklist:

- DD-214 or current Statement of Service (active duty)

- Two years of W-2s or federal tax returns

- Most recent 30 days of pay stubs

- Two months of bank statements for all accounts

- Your COE (if not already pulled by the lender)

- Government-issued photo ID

Your lender runs your credit, reviews your DTI, and issues a preapproval letter that specifies the maximum loan amount you qualify for. Sellers and their agents treat this letter as proof that you are a serious buyer, so secure it before you start touring homes.

Steps 5–7. Offer, underwriting, and closing

Once you have your preapproval letter in hand, the final three steps move quickly if you stay organized. Each stage has specific VA requirements that differ from a conventional purchase, so knowing what to expect keeps you from reacting to surprises and protects your closing date.

Step 5. Make an offer and sign a purchase contract

When you find a property, your real estate agent submits an offer on your behalf. Your preapproval letter goes with it to show the seller you are a verified buyer. Once both parties sign the purchase contract, send a copy to your lender immediately so they can open your loan file and order the VA appraisal without delay.

The VA requires you to use the property as your primary residence. Confirm this with your lender before you write any offer so the address and intended occupancy on your contract match your loan application.

Step 6. The VA appraisal and underwriting review

After you apply for a VA loan and the purchase contract is signed, the lender orders a VA appraisal through the VA's roster of approved appraisers. This appraisal serves two purposes: it confirms the property's market value and verifies that the home meets VA Minimum Property Requirements (MPRs). MPRs cover structural soundness, safe mechanical systems, and adequate living conditions. If the appraiser flags a repair, the seller typically must fix it before closing.

Underwriting runs alongside the appraisal. Your underwriter reviews your full file and checks each item against VA and lender guidelines. Here is what they evaluate:

- Income documentation: W-2s, pay stubs, tax returns, and any military allowances

- Credit history: Payment patterns, open accounts, and any derogatory marks

- Asset verification: Bank statements confirming you have funds for closing costs and reserves

- COE and entitlement: Confirmed benefit amount tied to the subject property

- Property eligibility: Appraisal report and MPR compliance

Respond to any underwriter conditions within 24 to 48 hours to avoid pushing your closing date back.

Step 7. Final walkthrough and closing

Your lender sends you a Closing Disclosure at least three business days before closing. Review it against your Loan Estimate and flag any fee that changed without explanation. On closing day, you sign the loan documents, pay any allowable closing costs, and receive your keys. VA loans restrict which fees lenders can charge you, so verify that only permitted charges appear on your final disclosure before you sign.

Ready to move forward

You now have a clear, step-by-step path to apply for a VA loan, from confirming your service eligibility and pulling your COE to selecting a lender, getting preapproved, and closing on your home. Each step builds on the one before it, so working through them in order keeps your timeline on track and reduces the chance of a last-minute delay.

The difference between a smooth VA loan experience and a frustrating one often comes down to the lender you choose. A loan officer with deep VA experience handles appraisal issues, entitlement questions, and underwriting conditions without slowing down your purchase. At David Roa, we bring over 25 years of mortgage experience and more than $150 million in funded loans to every file we work on. If you are ready to start, connect with a VA loan specialist at David Roa and get your preapproval moving today.