How Do VA Loans Work? Benefits, Costs, And Step-by-Step

VA loans are one of the strongest mortgage benefits available to U.S. military service members, veterans, and eligible surviving spouses, yet many who qualify don't fully understand how do VA loans work or what makes them different from conventional financing. The short answer: the Department of Veterans Affairs partially guarantees the loan, which allows private lenders to offer terms you won't find anywhere else, including zero down payment and no private mortgage insurance.

That guarantee changes the entire equation. It reduces the lender's risk, which means better rates and fewer upfront costs for you. But the VA doesn't actually lend the money, a private lender does, and that distinction matters when you're choosing who to work with. Having closed over $150 million in funded loans across more than 25 years, I've walked hundreds of borrowers through this exact process, and the questions that come up are almost always the same: Who qualifies? What does it actually cost? What's the catch?

This guide breaks down VA loan eligibility, benefits, costs (including the funding fee), and the step-by-step process from pre-approval to closing. Whether you're buying your first home or using your VA entitlement again, you'll leave with a clear picture of how the program works and what to expect at each stage.

What a VA loan is and how it works

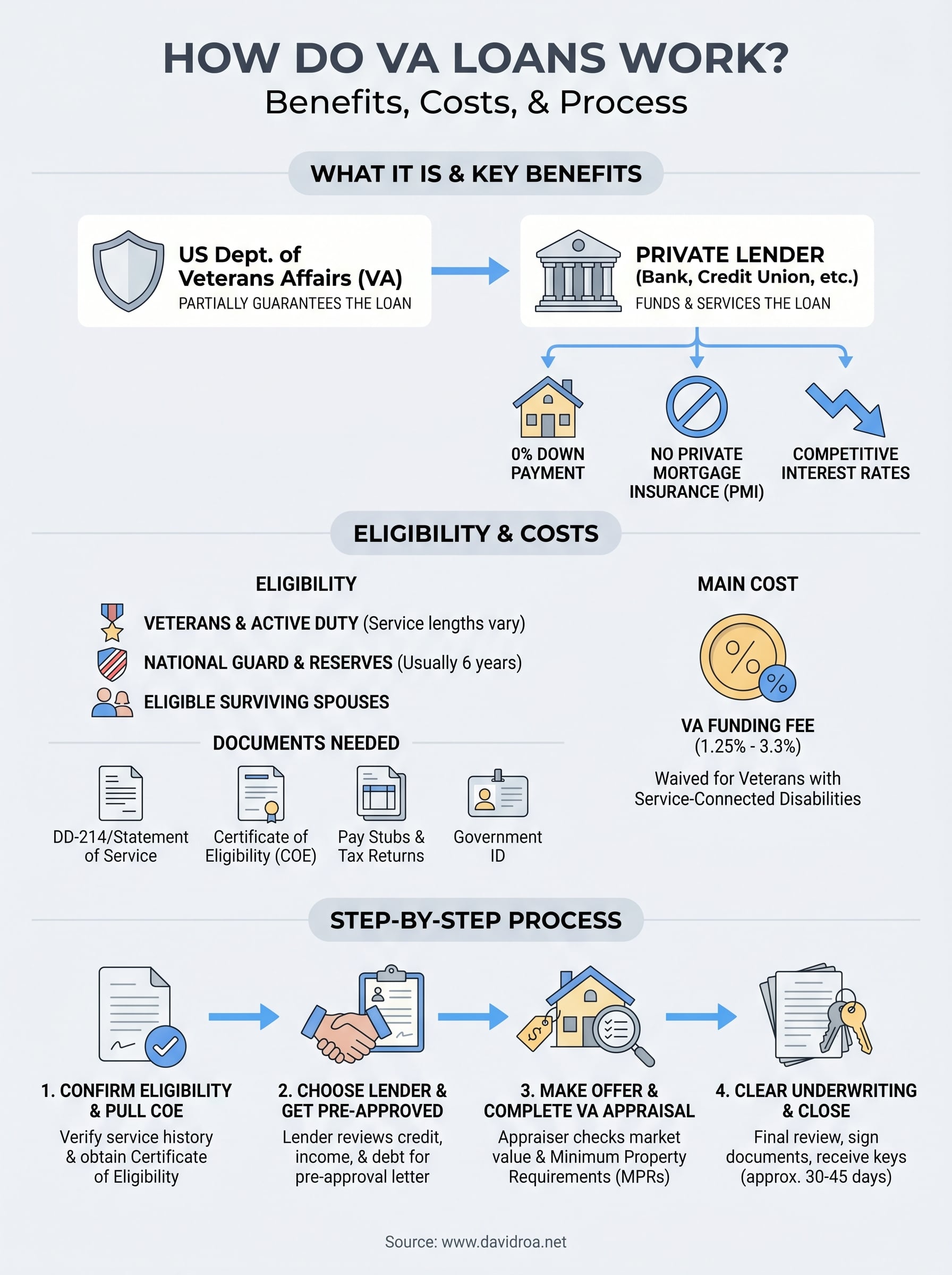

A VA loan is a mortgage backed by the U.S. Department of Veterans Affairs that eligible service members, veterans, and surviving spouses can use to purchase, build, or refinance a home. The key word is "backed." The VA doesn't hand you money directly. Instead, it guarantees a portion of the loan to a private lender, which changes the risk profile of the entire transaction in your favor.

The government guarantee explained

Understanding how do VA loans work starts with the guarantee itself. When a lender approves a conventional loan without a down payment, they take on serious risk if you default. The VA removes most of that risk by promising to repay the lender up to 25% of the loan amount if you stop making payments. Because the lender is protected, they're willing to extend better terms to you, including lower interest rates, no down payment requirement, and no private mortgage insurance (PMI).

The VA guarantee is what makes zero-down lending possible at competitive rates. Without it, lenders would require a 20% down payment to cover that same level of risk.

The size of the guarantee ties directly to your VA entitlement, which is essentially your borrowing power under the program. Most eligible veterans carry full entitlement, meaning there is no VA-set loan limit for them as of 2020. If you've used a VA loan before and paid it off, you can restore your entitlement and use the benefit again. If you have a partial entitlement remaining, county-level conforming loan limits may apply depending on your lender's requirements.

How the VA loan process actually works

The actual mechanics are straightforward. A private lender, such as a bank, credit union, or mortgage broker, funds and services your loan. The VA sets the guidelines those lenders must follow, including minimum service requirements, acceptable property types, and appraisal standards. Your lender handles the application, underwriting, and closing, while the VA's role is to set the rules and back the guarantee.

One important step in that process is the VA appraisal. Before your lender approves the loan, a VA-assigned appraiser assesses both the property's market value and its condition against Minimum Property Requirements (MPRs). The home needs to be safe, structurally sound, and sanitary. This protects you from buying a property with serious defects, but it also means certain fixer-uppers may not qualify for standard VA financing unless repairs are completed first.

Private lenders also have some flexibility in setting their own overlays, meaning they can require a slightly higher credit score or a stricter debt-to-income ratio than the VA's minimum guidelines. That's exactly why choosing an experienced VA lender matters. The program's benefits are strong, but the lender you work with determines how smoothly the process runs from application to keys in hand.

VA loan benefits and downsides

Understanding how do VA loans work means looking at both sides of the equation. The program delivers genuinely strong advantages that most conventional loans can't match, but a few limitations are worth knowing before you apply. Knowing both sides upfront helps you go in with accurate expectations.

The benefits that set VA loans apart

The biggest draw is the zero down payment option. You can purchase a home without saving tens of thousands of dollars upfront, which is a significant advantage in high-price markets where a 20% down payment would take years to accumulate. Combined with no private mortgage insurance requirement, your monthly payment stays lower than it would with a comparable conventional loan at less than 20% down.

For most qualified borrowers, the monthly savings from skipping PMI alone can offset the VA funding fee within the first few years of ownership.

VA loans also tend to carry competitive interest rates because the government guarantee reduces lender risk. You'll also benefit from limits on closing costs, since the VA restricts which fees lenders can charge. On top of that, if you run into financial hardship after closing, the VA offers counseling services and will advocate on your behalf with the servicer to explore alternatives to foreclosure.

Where VA loans fall short

The VA funding fee is the main cost to plan for. This upfront fee ranges from 1.25% to 3.3% of the loan amount depending on your down payment size and whether it's your first use of the benefit. Most borrowers roll it into the loan, which adds to your overall loan balance and means you pay interest on it over the life of the loan. Veterans with service-connected disabilities are exempt from this fee entirely.

Beyond the fee, the VA appraisal process can create friction in competitive markets. Because VA appraisers must verify Minimum Property Requirements, some sellers hesitate to accept VA offers on homes with deferred maintenance or condition issues. You're also limited to owner-occupied properties, meaning you can't use a VA loan to buy a rental or vacation home. This is a hard boundary, and no workaround exists within the program.

VA loan eligibility and required documents

Before you can fully apply what you learn about how do va loans work, you need to confirm you're actually eligible. The VA sets clear service-based requirements that determine whether you can access the program at all. Meeting those requirements is the starting point, but your private lender will still evaluate your credit score, income, and debt load during underwriting, so eligibility and approval are two separate things.

Who qualifies for a VA loan

Eligibility breaks down into a few distinct groups based on your service history. Active-duty service members generally qualify after 90 continuous days of active service. Veterans must meet minimum service thresholds that vary depending on when they served, typically 90 days during wartime or 181 days during peacetime. Members of the National Guard and Reserves qualify after six years of service, though federal activation orders can shorten that window. Eligible surviving spouses of veterans who died in the line of duty or from a service-connected disability may also use the benefit.

The fastest way to confirm your eligibility is to obtain a Certificate of Eligibility through the VA, which your lender can often request on your behalf directly through an automated system.

Your discharge status also affects eligibility. An honorable or general discharge qualifies you. A dishonorable discharge disqualifies you entirely, while other-than-honorable discharges go through a case-by-case review process at the VA level.

Documents you'll need to apply

Pulling your paperwork together before your first lender conversation saves real time during underwriting. Your lender will need documents to verify both your VA eligibility and your financial standing, and gaps in either area can slow your approval. Having everything organized upfront is one of the most practical steps you can take.

Here's what you'll typically need to provide:

- DD-214 for veterans, or a Statement of Service for active-duty members

- Certificate of Eligibility (COE), which your lender can pull electronically in most cases

- Pay stubs from the last 30 days

- W-2s and federal tax returns from the past two years

- Bank statements covering the last two to three months

- Government-issued photo ID

How to get a VA loan step by step

Understanding how do VA loans work on paper is one thing; moving through the actual process is another. The steps follow a clear sequence, and each one has details that can either accelerate or stall your timeline depending on how prepared you are going in. Knowing what comes next at every stage puts you in control of the process rather than reacting to it.

Confirm eligibility and pull your COE

Your first move is to verify your service eligibility and obtain your Certificate of Eligibility. In most cases, your lender can pull your COE directly through the VA's automated system in minutes. If you have unusual service history or a prior VA loan on record, the process may take a few additional days, but it rarely blocks the application entirely.

Choose a lender and get pre-approved

Not every lender has the same level of experience with VA loans, and that gap shows up during underwriting. You want a lender who handles VA appraisals regularly, understands the program's property requirements, and communicates clearly at each stage. Once you select a lender, they review your income, credit score, and debt-to-income ratio to issue a pre-approval letter, which signals to sellers that you're a serious buyer who can close.

Pre-approval is not a guarantee of final loan approval, but it puts you in a significantly stronger position when making an offer on a home.

Make an offer and complete the VA appraisal

Once a seller accepts your offer, your lender orders a VA appraisal through the VA's appraisal management system. The appraiser checks both the market value of the home and its physical condition against the VA's Minimum Property Requirements. If the home clears both tests, you move forward. If the appraiser flags repairs, you'll need to negotiate with the seller to address them before closing can proceed.

Clear underwriting and close

Your lender's underwriting team reviews your complete loan file, including income documents, credit history, the appraisal report, and title work. Once underwriting issues a clear-to-close, you'll review your final Closing Disclosure, sign your loan documents, and receive the keys. The full timeline from application to closing typically runs 30 to 45 days with an experienced VA lender.

VA loan FAQs and common misconceptions

Even after reading a detailed breakdown of how do VA loans work, a few stubborn misconceptions tend to hold qualified borrowers back from applying. Clearing those up now means you move forward with accurate information rather than second-guessing a benefit you've already earned through your service.

Can you use a VA loan more than once?

Yes, and this is one of the most common misunderstandings about the program. Your VA entitlement is not a one-time benefit. Once you pay off a VA loan and sell the property, you can restore your full entitlement and use the program again on your next purchase. You can also hold two VA loans simultaneously in certain situations, such as when a military relocation requires you to purchase a new primary residence before selling your previous home. Partial entitlement situations require a closer look, but a lender with strong VA experience can tell you exactly what you have available before you start shopping.

Does a VA loan require perfect credit?

The VA does not set a minimum credit score requirement at the program level. Private lenders set their own standards, and most look for a score somewhere between 580 and 620. A lower score does not automatically disqualify you, but it can affect your rate and lender options. If your score needs work before you apply, focus on paying down revolving balances and correcting any errors on your credit report directly through the bureaus first.

Strong credit still improves your rate and expands your lender choices, even when the VA itself does not require a specific score threshold.

Is the VA funding fee avoidable?

For most borrowers the funding fee is a required cost, but it is not always unavoidable. Veterans with a service-connected disability rating from the VA are fully exempt, which can save thousands of dollars depending on the loan size. Active-duty service members who have received the Purple Heart are also exempt. If you think you may qualify, confirm your disability rating status before closing because the exemption must be applied at loan origination and cannot be refunded after the fact.

Where to go from here

Now that you understand how do VA loans work, from the government guarantee to the step-by-step closing process, you have a real foundation to move forward with confidence. The program's combination of zero down payment, no PMI, and competitive rates makes it one of the most valuable financing tools available to eligible veterans and service members, but knowing the mechanics is only the first step. Selecting the right lender determines how smoothly everything else runs.

Your next move is to confirm your eligibility, pull your Certificate of Eligibility, and connect with a lender who has direct experience closing VA loans. That experience matters when the appraisal comes back with conditions or when underwriting needs documentation quickly. If you're ready to get started or have specific questions about your situation, reach out to an experienced VA loan specialist who can walk you through your options based on your actual service history and financial picture.