What Is A Conventional Mortgage? Requirements, Pros & Cons

If you're shopping for a home loan, you've probably seen the term "conventional mortgage" pop up more than any other option. It's the most common type of home financing in the United States, yet many buyers, especially first-timers, aren't sure what it actually means or how it stacks up against government-backed alternatives like FHA or VA loans.

Here's the short answer: a conventional mortgage is a home loan that isn't insured or guaranteed by a federal agency. That distinction matters because it affects everything from your down payment and credit score requirements to your monthly costs and long-term flexibility. Whether a conventional loan is the right fit depends on your financial profile and goals, and understanding the details before you apply puts you in a much stronger position at the closing table.

With over 25 years in the lending business and more than $150 million funded, I've helped borrowers across the Chicago area and nationwide choose the right loan product for their situation. At David Roa, we work through every option, conventional, FHA, VA, Jumbo, and beyond, so you're never squeezed into a program that doesn't serve you. In this guide, I'll break down exactly how conventional mortgages work, what lenders expect from you, and the real pros and cons you should weigh before making a decision.

Why a conventional mortgage is so common

When buyers ask what is a conventional mortgage and why it dominates the market, the answer comes down to flexibility. Conventional loans aren't backed by the government, which means private lenders set their own guidelines within a framework established by Fannie Mae and Freddie Mac. That structure gives lenders room to serve a wider range of borrowers, from first-time buyers putting 3% down to move-up buyers with substantial equity and strong credit history.

Conventional loans account for roughly 70% of all mortgages originated in the United States each year, according to data from the Federal Housing Finance Agency.

More options across loan sizes and property types

One of the biggest reasons conventional mortgages stay at the top of the market is that they work across a broader set of property types and loan amounts than most government-backed programs allow. You can use a conventional loan to finance a primary residence, a second home, or an investment property. Conforming conventional loans currently go up to $806,500 in most U.S. counties, with higher limits in designated high-cost areas, and Jumbo conventional loans cover amounts above that threshold.

This range matters because your financial goals shift over time. A conventional loan grows with you: the same product type that helps you buy your first home also works when you're ready to add a rental property or vacation home, without forcing you into a completely different program with different rules.

PMI removal gives you a real exit

Government-backed loans like FHA carry mortgage insurance that stays for the life of the loan in most cases. A conventional loan works differently. If you put down less than 20%, you'll pay private mortgage insurance (PMI), but you can request cancellation once your loan balance drops to 80% of the home's original appraised value, and lenders must terminate it automatically at 78% under the federal Homeowners Protection Act.

That built-in exit from PMI saves you real money over time. For a borrower carrying a $400,000 loan balance, PMI typically runs between $100 and $200 per month. Eliminating that payment even a few years into repayment makes a measurable difference in your monthly budget and total cost of homeownership.

Competitive rates for the right financial profile

Conventional loans reward borrowers who carry strong credit scores and low debt-to-income ratios with some of the most competitive interest rates available. Because these loans typically get sold into the secondary market through Fannie Mae or Freddie Mac, lenders operate within a liquid, standardized system that keeps pricing tight. If your financial profile is solid, a conventional loan will often beat FHA on both rate and total cost once you account for mortgage insurance over the full loan term.

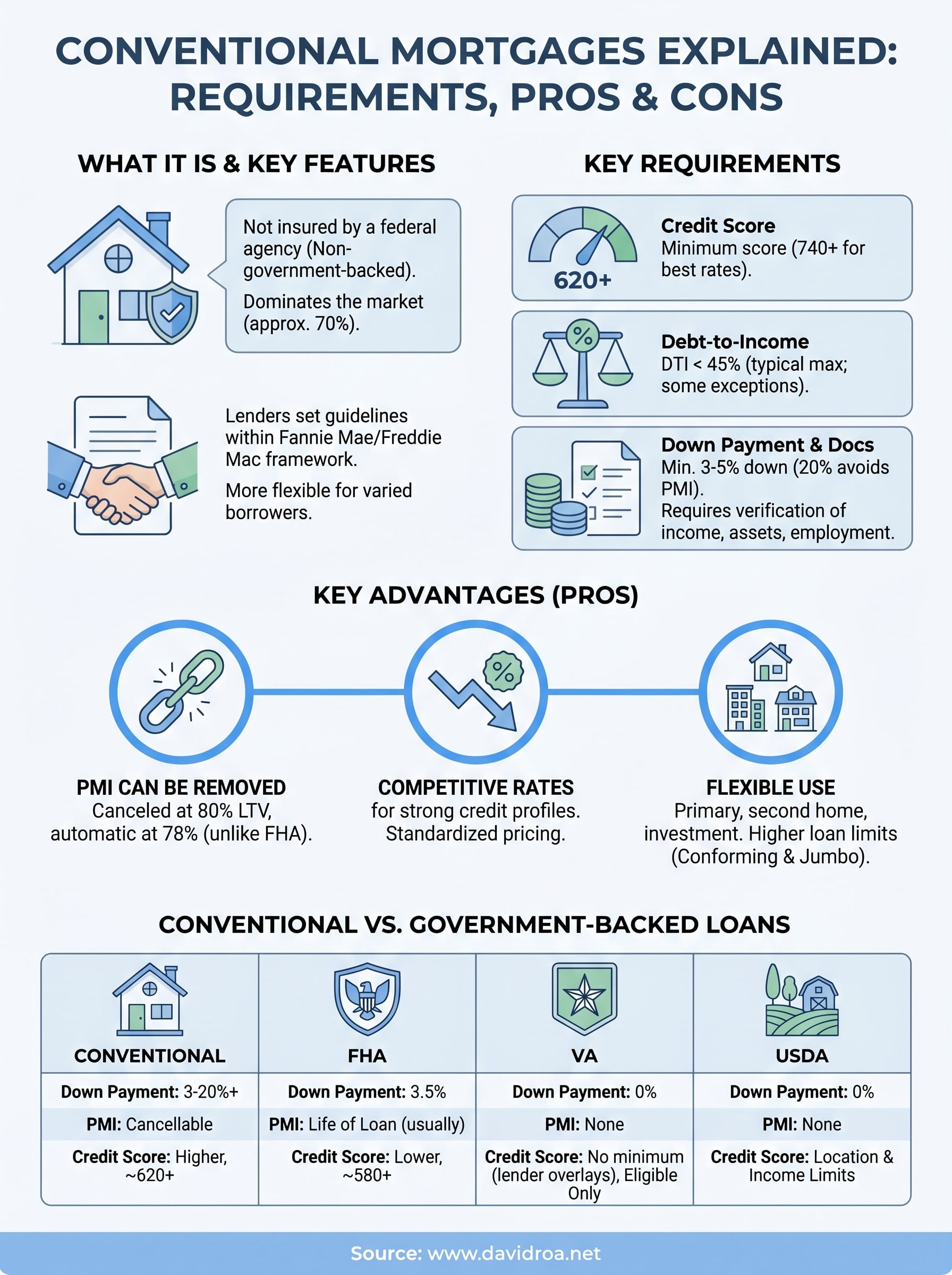

Conventional mortgage requirements at a glance

One question that comes up constantly when people ask what is a conventional mortgage is: "Do I actually qualify?" The answer depends on four core factors: your credit score, debt-to-income ratio, down payment, and the documentation you bring to the table. Meeting these benchmarks puts you in a strong position to get approved and lock in competitive pricing.

Credit score and debt-to-income ratio

Most lenders require a minimum credit score of 620 to qualify for a conventional loan, though scores above 740 unlock the best available rates. Your debt-to-income (DTI) ratio is equally important: lenders generally want your total monthly debt payments, including the proposed mortgage, to stay at or below 45% of your gross monthly income. Some automated underwriting systems will approve DTIs up to 50% for borrowers with strong compensating factors like significant cash reserves.

Borrowers with credit scores above 740 and DTI ratios below 36% consistently qualify for the lowest rates and most favorable loan terms available on conventional mortgages.

Down payment and loan limits

Your down payment requirement starts at 3% for qualified first-time buyers under Fannie Mae's HomeReady program, and 5% for most other borrowers. Putting down 20% eliminates PMI entirely from day one, which produces real long-term savings. For 2025, the conforming loan limit sits at $806,500 in most counties, with higher ceilings in high-cost markets.

Here's a quick breakdown of how down payment size affects your loan:

| Down Payment | PMI Required | Loan Type |

|---|---|---|

| 3% | Yes | Conforming conventional |

| 5-19% | Yes | Conforming conventional |

| 20%+ | No | Conforming or Jumbo |

Lenders also verify income, employment history, and assets through documents like W-2s, tax returns, and bank statements. Having two years of steady employment in the same field strengthens your file significantly.

How to apply for a conventional mortgage

Once you understand what is a conventional mortgage and confirm it fits your situation, the application process is straightforward if you come prepared. Lenders move faster and offer better terms when your financial documents are organized and your credit profile is clean before you submit a single form. Taking a few weeks to prepare upfront saves you from delays and unwanted surprises mid-process.

Get your finances in order first

Before you contact any lender, pull your credit reports from all three bureaus through AnnualCreditReport.com and dispute any errors you find. Even a small correction can lift your score enough to drop you into a better rate tier. At the same time, avoid opening new credit accounts or making large undocumented deposits into your bank accounts, both of which raise flags during underwriting.

Lenders typically review the last 60 days of bank statements, so any unusual activity right before your application can slow down or complicate your approval.

Gather your W-2s, federal tax returns from the past two years, recent pay stubs, and two months of bank statements before your first lender conversation. If you're self-employed, expect to provide profit and loss statements as well. Having this documentation ready shortens your processing time significantly.

Move through the application and underwriting process

Once you submit your application, the lender issues a Loan Estimate within three business days that outlines your rate, monthly payment, and closing costs. Review this document carefully and ask questions about anything unclear. After you formally accept, the file moves to underwriting where the lender verifies your income, assets, employment, and the property's appraised value.

Stay responsive during this phase. Underwriters regularly request additional documentation, and slow responses push back your closing date. Keep your financial situation stable, hold off on major purchases, and maintain steady employment until the loan closes.

Types of conventional mortgages

Understanding what is a conventional mortgage also means understanding that "conventional" isn't one single product. The category splits into several distinct loan types based on loan size, rate structure, and underwriting guidelines. Choosing the right variation depends on your loan amount, how long you plan to stay in the home, and your tolerance for payment fluctuation.

Conforming and non-conforming loans

Conforming conventional loans meet the loan limits and underwriting standards set by Fannie Mae and Freddie Mac, which allows lenders to sell them on the secondary market. In 2025, the conforming limit is $806,500 in most counties, with higher ceilings in high-cost areas. Staying within this limit typically earns you lower rates because lenders carry less risk.

Non-conforming loans, commonly called Jumbo loans, cover purchase prices above the conforming limit and require stronger credit profiles and larger down payments to compensate for the higher exposure lenders take on.

If your purchase price pushes above the conforming cap, a Jumbo conventional loan steps in to fill the gap. Jumbo products often require a credit score of 700 or higher and a down payment of at least 10 to 20 percent, though exact requirements vary by lender.

Fixed-rate and adjustable-rate options

A fixed-rate conventional mortgage locks your interest rate for the entire loan term, typically 15 or 30 years. Your principal and interest payment never changes, which makes long-term budgeting straightforward. Most buyers who plan to stay in a home for seven or more years benefit from this stability.

An adjustable-rate mortgage (ARM) starts with a fixed rate for an introductory period, usually 5, 7, or 10 years, then adjusts periodically based on a benchmark index. ARMs often open with lower initial rates than fixed-rate loans, which can reduce your payment in the early years if you plan to sell or refinance before the adjustment period begins.

Conventional vs FHA, VA, and USDA loans

Understanding what is a conventional mortgage gets clearer when you place it side by side with government-backed programs. Each loan type serves a different borrower profile, and choosing the wrong one can cost you thousands over the life of your loan. The right choice depends on your credit score, military status, location, and how long you plan to keep the property.

FHA loans: lower bar, higher long-term cost

FHA loans are insured by the Federal Housing Administration and allow credit scores as low as 580 with a 3.5% down payment. That lower entry point helps buyers who haven't had time to build strong credit, but it comes with a significant drawback: you pay mortgage insurance for the life of the loan in most cases, regardless of how much equity you build.

Conventional loans become the cheaper long-term option for most borrowers once their credit score exceeds 680, because PMI can be canceled while FHA mortgage insurance typically cannot.

Conventional loans require a stronger financial profile upfront, but they reward you with lower total costs over time if your credit and down payment meet the threshold. For buyers on the credit boundary, running the numbers on both programs with your lender before committing makes sense.

VA and USDA loans: program-specific eligibility

VA loans, backed by the Department of Veterans Affairs, are available exclusively to eligible veterans, active-duty service members, and qualifying surviving spouses. They offer zero down payment and no PMI, making them the strongest available product for those who qualify. If you have VA eligibility, it almost always beats a conventional loan on cost.

USDA loans serve buyers purchasing in designated rural and suburban areas with moderate incomes. They also offer zero down payment but carry geographic and income restrictions that conventional loans don't. If your target property falls outside USDA-eligible zones or your income exceeds program limits, a conventional mortgage remains your most practical path forward.

Final takeaways

Understanding what is a conventional mortgage puts you in a stronger position before you ever sit down with a lender. Conventional loans offer flexible property eligibility, cancelable PMI, and competitive rates for borrowers who bring solid credit and a reasonable down payment to the table. They work well for primary homes, second properties, and investment purchases, making them the most versatile financing tool available to most buyers.

Your specific financial profile determines whether a conventional loan beats FHA, VA, or USDA for your situation. Borrowers with credit scores above 680 and stable income usually find conventional products deliver better long-term value once you account for total mortgage insurance costs across the full loan term.

Making the right call requires a real conversation with an experienced lender who knows every program available. If you're ready to run those numbers and find the best fit for your goals, connect with David Roa today.