What Is a VA Loan? Eligibility, Benefits & How It Works Now

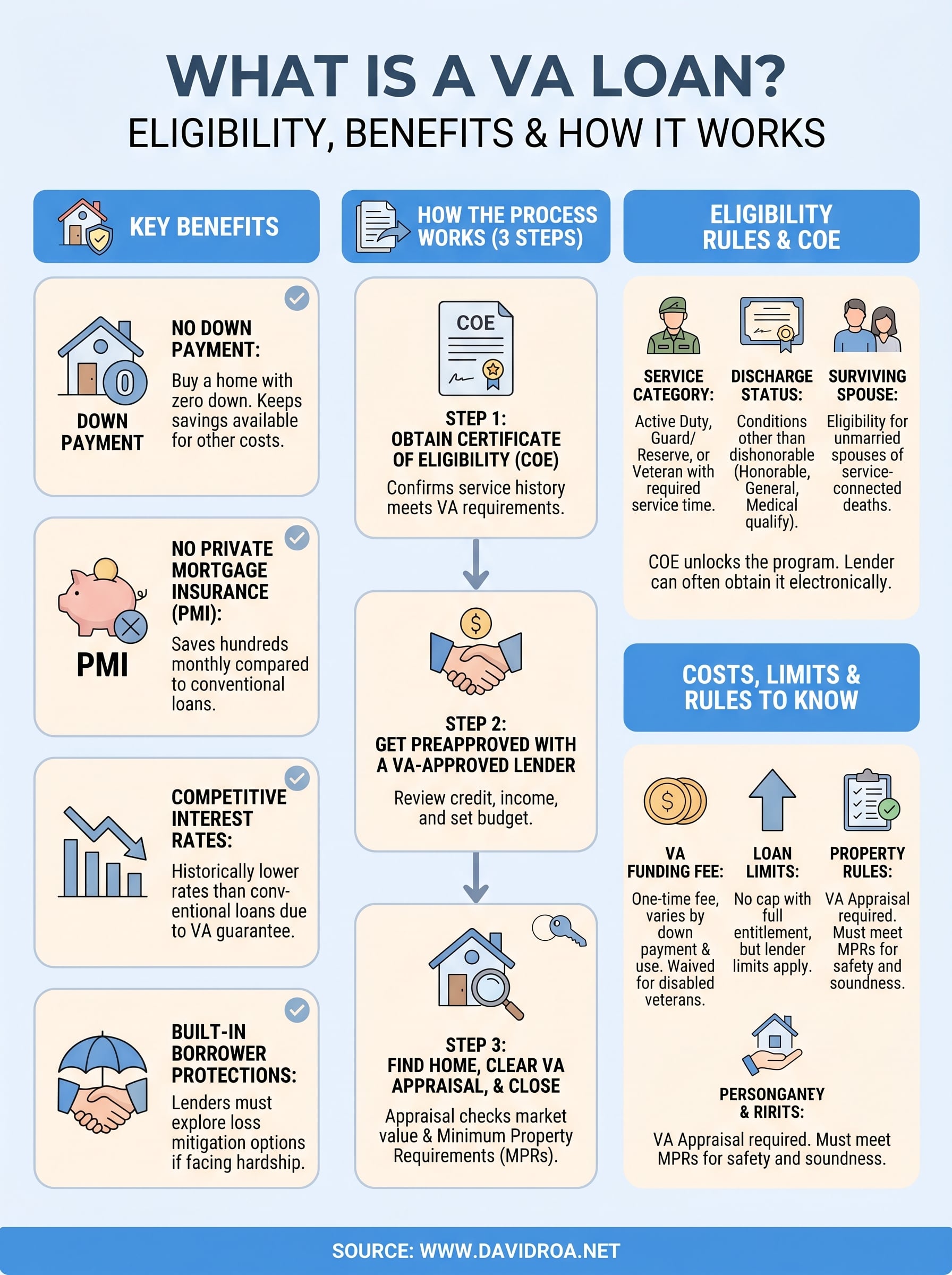

If you've served in the military or are currently serving, you've probably heard someone mention VA loans. But what is a VA loan, exactly, and why does it consistently rank as one of the best mortgage options available? It's a home loan backed by the U.S. Department of Veterans Affairs, designed to help eligible service members, veterans, and surviving spouses buy a home, often with no down payment and no private mortgage insurance.

That's not a small deal. On a $300,000 home, skipping the down payment alone could save you $60,000 upfront compared to a conventional loan requiring 20% down. And dropping PMI can save hundreds per month. These aren't theoretical savings, they're real dollars that stay in your pocket at a time when every dollar matters. The catch? Not everyone qualifies, and the process has specific steps that differ from a standard mortgage.

At David Roa, we've helped veterans and active-duty service members secure VA loans as part of over $150 million in funded deals across more than 25 years in lending. Below, we break down exactly who qualifies, what benefits you can expect, and how the VA loan process works from application to closing, so you can move forward with clarity, not confusion.

Why VA loans matter for eligible homebuyers

When you ask what is a VA loan and why it deserves serious attention, the answer comes down to one core fact: no other mortgage program gives eligible buyers this combination of zero down payment, no PMI, and competitive rates at the same time. Most loan programs force you to trade one benefit for another. VA loans don't. For service members, veterans, and surviving spouses who qualify, the financial advantages are substantial and start from the moment you close.

No down payment required

For most buyers, the down payment is the single biggest obstacle to homeownership. A conventional loan typically requires 3% to 20% down, and FHA loans ask for at least 3.5%. VA loans let you buy with zero down payment if you have full entitlement, which means your savings stay available for other priorities. Here is where that liquidity can go instead:

- Moving and relocation costs

- Home repairs or upgrades immediately after purchase

- Six months of emergency reserves

- Business capital if you also invest or own a company

On a $400,000 home, skipping a 10% down payment keeps $40,000 working for you instead of going directly into equity you cannot touch.

No private mortgage insurance

When conventional borrowers put less than 20% down, lenders require private mortgage insurance (PMI), which typically costs 0.5% to 1.5% of the loan amount each year. On a $300,000 loan, that adds $1,500 to $4,500 annually to your costs. VA loans never require PMI, regardless of how much you put down or what your credit profile looks like.

That distinction adds up fast. Removing PMI on a $350,000 loan at a 1% rate saves you roughly $292 per month. Over a 30-year term, that single removed line item saves more than $100,000 in total payments, without changing anything else about the loan.

Competitive interest rates

VA loans consistently carry lower average interest rates than conventional mortgages. The VA guarantee reduces lender risk, which allows lenders to pass better pricing on to you. Historically, VA loan rates have run 0.25% to 0.50% below comparable conventional rates. On a $300,000 loan over 30 years, even a quarter-point reduction saves more than $15,000 in total interest paid.

Your credit score still affects the specific rate you receive, but lenders have more flexibility to approve borrowers with less-than-perfect credit histories on VA loans than on conventional products. That matters if you've had financial setbacks in the past but currently have stable income.

Built-in borrower protections

Beyond the upfront savings, VA loans include mandatory servicer obligations that conventional mortgages do not carry. If you face financial hardship, your lender must explore every loss mitigation option before moving toward foreclosure. That includes repayment plans, loan modifications, and special forbearance programs overseen by the VA, giving you a real safety net that standard mortgage servicers are not required to provide.

How a VA loan works from COE to closing

One question that comes up after you understand what is a VA loan is how the process actually unfolds day to day. The steps follow a clear, predictable sequence, and knowing them in advance keeps you from losing time or momentum when you find the right home and want to move quickly.

Step 1: Obtain your Certificate of Eligibility

Your Certificate of Eligibility (COE) is the document that confirms your service history meets VA lending requirements. You can request it through the VA's eBenefits portal, through your lender directly, or by mailing VA Form 26-1880. Most lenders can pull it electronically in minutes once you provide your service information. Without a valid COE, no lender can process your VA loan application, so getting this document squared away is the first concrete step you take.

Your lender can often obtain your COE on your behalf through the VA's automated system, which speeds up this step significantly.

Step 2: Get preapproved with a VA-approved lender

After securing your COE, you apply for preapproval with a lender who participates in the VA loan program. The lender reviews your credit score, income, employment history, and debt-to-income ratio. VA loans do not set a minimum credit score by rule, but most lenders apply their own internal floor, typically around 620. Preapproval gives you a firm budget before you start shopping and signals to sellers that you are a serious, qualified buyer backed by a strong loan program.

Step 3: Find a home, clear the VA appraisal, and close

Once you have a signed purchase contract, your lender orders a VA appraisal conducted by an independent VA-approved appraiser. This appraisal confirms the home's market value and verifies that the property meets the VA's Minimum Property Requirements (MPRs), which cover safety, structural soundness, and sanitary conditions. If the home clears both reviews, you move into underwriting and then to closing. At closing, you will see the VA funding fee appear as a line item in your final closing disclosure, which you can pay upfront or roll into the loan balance.

VA loan eligibility rules and the COE

One of the first questions people ask when they start researching what is a VA loan is whether they actually qualify. Eligibility comes down to your service history, your discharge status, and your ability to document both through a Certificate of Eligibility. Missing any one of those pieces can delay your application, so it pays to sort them out before you approach a lender.

Service requirements by category

Your specific service category determines the minimum active-duty periods required to qualify. The VA breaks eligibility into three main groups: active duty, National Guard and Reserve members, and veterans. Knowing which category fits your background tells you exactly what documentation you need to gather.

| Service Category | Minimum Service Requirement |

|---|---|

| Active Duty | 90 continuous days during wartime, or 181 days during peacetime |

| National Guard / Reserves | 6 years of service, or 90 days under Title 32 orders |

| Veteran | Discharged under conditions other than dishonorable |

An other-than-honorable discharge may still qualify under certain circumstances, but you would need to request a discharge upgrade review through the VA before applying.

Discharge status carries significant weight throughout this process. A dishonorable discharge automatically removes eligibility, while honorable, general, and medical discharges all qualify. If your paperwork shows anything in a gray area, the VA has a formal review process you can initiate before you apply.

Surviving spouse eligibility

Surviving spouses of veterans who died in service or from a service-connected disability may also qualify for a VA loan. To use this benefit, the surviving spouse must not have remarried, with limited exceptions for remarriages that occurred after age 57. Required documentation includes VA Form 26-1817 along with the veteran's discharge papers.

Securing your Certificate of Eligibility is the step that formally unlocks the program, regardless of which eligibility category applies to you. Your lender can pull it electronically through the VA's automated system, which means you often have confirmation within minutes of starting your application.

Costs, limits, and rules to know

Once you understand what is a VA loan and how eligibility works, the next step is getting familiar with the actual costs and structural rules that govern the program. VA loans eliminate PMI and often require no down payment, but they do carry specific fees and limits that you need to account for before you finalize your purchase strategy.

The VA funding fee

The VA funding fee is a one-time charge the government uses to sustain the VA loan program without relying on ongoing taxpayer contributions. The fee percentage varies based on your down payment amount and whether this is your first time using the benefit. First-time users with no down payment pay 2.15% of the loan amount, while subsequent users pay 3.3%. Putting 5% or more down reduces that percentage meaningfully.

Veterans receiving VA disability compensation of any amount are fully exempt from the funding fee, which can save thousands at closing.

You can pay the funding fee at closing as a lump sum or roll it into your loan balance. Rolling it in keeps cash in your pocket upfront, but you will pay interest on that added amount over the full loan term, so factor both scenarios into your budget before you decide.

Loan limits and property rules

VA loans do not cap how much you can borrow when you carry full entitlement, meaning your lender determines the maximum based purely on your income and creditworthiness. If you hold remaining entitlement from a prior VA loan you still carry, county conforming loan limits may apply to any amount above your available entitlement portion.

Every property you purchase with a VA loan must also pass a VA appraisal conducted by an independent VA-approved appraiser. This review confirms market value and verifies that the home meets the VA's Minimum Property Requirements, covering structural soundness, safety hazards, and sanitary systems. Homes with major deficiencies require documented repairs before your lender can move the file to closing.

VA loan pros and cons vs other mortgages

When you're weighing what is a VA loan against other mortgage options, the comparison gets more useful once you put them side by side. VA loans beat most alternatives on upfront cost and monthly payment, but they carry specific restrictions that FHA, conventional, and USDA loans do not impose. Understanding both sides helps you choose the right product for your actual situation.

Where VA loans win

VA loans outperform conventional and FHA products in three concrete ways: no required down payment, no PMI, and lower average interest rates. FHA loans require at least 3.5% down and carry both an upfront mortgage insurance premium and an annual MIP that stays for the life of the loan in most cases. Conventional loans drop PMI once you reach 20% equity, but you still have to carry it until then. VA loans skip both barriers entirely from day one.

If you qualify for a VA loan, using it over an FHA or conventional product will almost always result in a lower total cost of ownership over the full loan term.

Beyond insurance savings, the rate advantage is meaningful. Because the VA guarantees a portion of each loan, lenders take on less default risk, which typically translates to rates that run below conventional market pricing without requiring you to pay points upfront to buy them down.

Where VA loans fall short

Eligibility is the program's single biggest limitation, and it is a hard one. Buyers with no military service connection cannot access VA loans at all, which pushes them toward FHA or conventional alternatives. The program also restricts financing to primary residences only, so you cannot use a VA loan to purchase an investment property or a second home. Conventional loans give real estate investors far more flexibility on property type. The funding fee is another real cost. Unlike PMI, you cannot cancel or remove it retroactively once it is paid or rolled into your balance, so it represents a fixed expense tied directly to using the benefit.

Next steps

Now that you know what is a VA loan and how every part of it works, the logical move is to take action before rates shift or your target home goes under contract with another buyer. Start by pulling your service records and requesting your Certificate of Eligibility through the VA's eBenefits portal or directly through a lender. That single document unlocks the entire process, so getting it in hand first saves you time later.

From there, connect with a lender who has direct experience closing VA loans, not just general mortgage volume. The VA appraisal process, entitlement calculations, and funding fee exemptions require hands-on knowledge that generalist lenders often lack. Working with someone who has seen these deals close repeatedly makes a real difference when timing is tight.

If you are ready to move forward, reach out to David Roa to review your VA loan options with a lender who has funded over $150 million in deals across 25-plus years.