1031 Exchange Explained: Rules, Timelines, And Examples

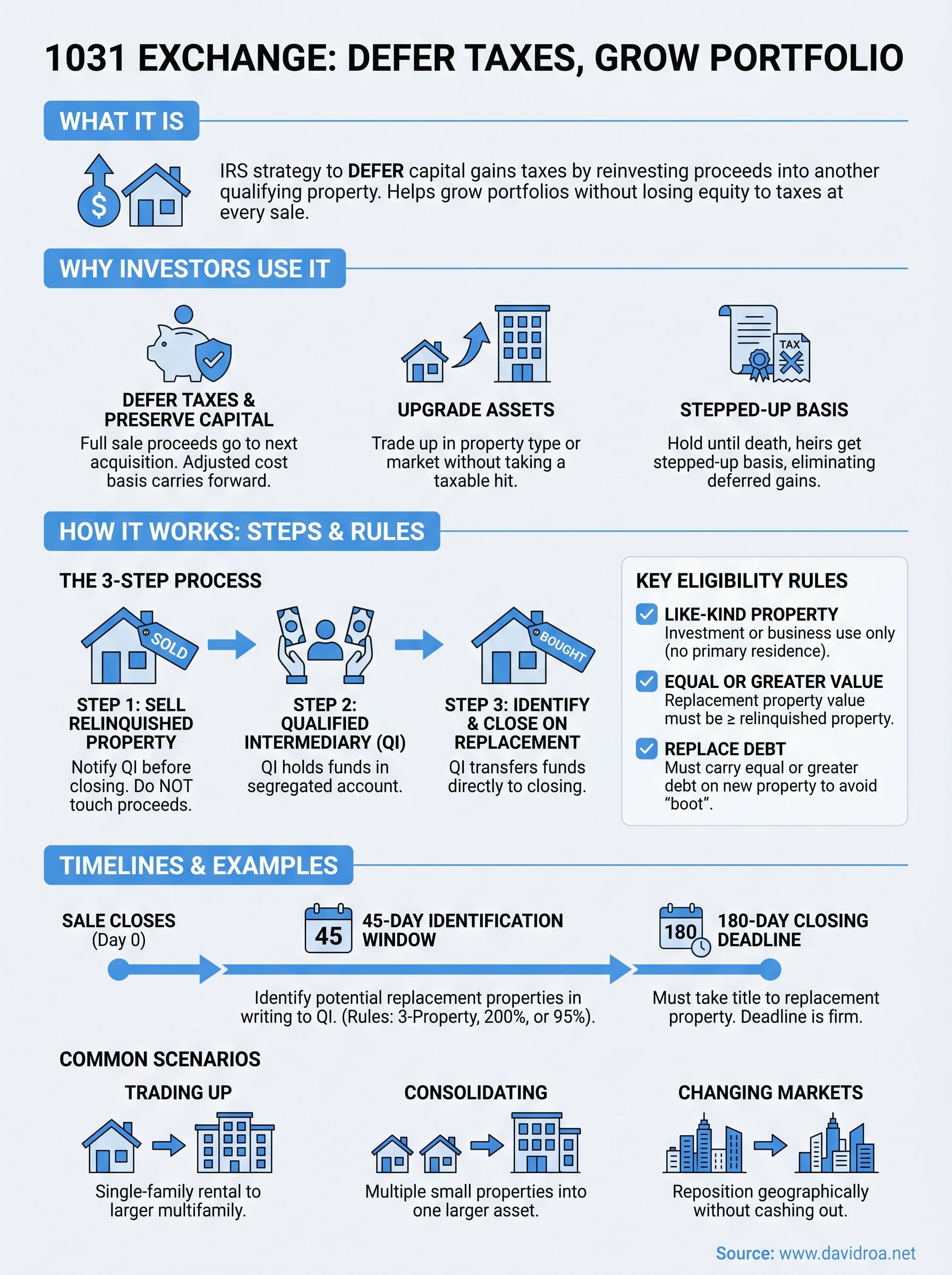

You sell an investment property, pocket a solid profit, and then watch a chunk of it disappear to capital gains taxes. That scenario plays out constantly for real estate investors who don't plan their exits. A 1031 exchange explained in simple terms is this: a strategy written into the IRS tax code that lets you defer those capital gains taxes by reinvesting the proceeds into another qualifying property. It's one of the most powerful tools available to investors who want to grow their portfolios without losing equity to Uncle Sam at every transaction.

But the rules are strict, the timelines are tight, and one misstep can disqualify the entire exchange. That's where clarity matters. Over the past 25-plus years, I've helped real estate investors across the Chicago area and nationwide structure deals that align with their long-term goals, including financing the replacement properties that make 1031 exchanges work. At David Roa, we see these transactions from both sides: as an active investor and as a lender who has funded over $150 million in deals.

This guide breaks down how a 1031 exchange works, the IRS rules you need to follow, the critical deadlines that trip people up, and real examples that show the strategy in action. Whether you're flipping your first rental into a larger asset or rolling a portfolio forward, you'll walk away with a clear understanding of how to use this tax code provision to your advantage.

Why investors use 1031 exchanges

Real estate investing builds wealth over time, but every property sale creates a tax event that can cut deeply into your returns. The federal capital gains tax rate on investment property can reach up to 20%, and when you factor in depreciation recapture and state taxes, the total bill can easily consume 30% or more of your profit. Investors who grasp the 1031 exchange explained correctly use it to keep that money working inside their portfolio rather than writing a check to the IRS at every transaction.

Deferring taxes to preserve capital

The most immediate benefit is straightforward: you defer taxes rather than avoid them permanently. When you complete a valid exchange, the IRS does not collect capital gains taxes at the point of sale. Instead, the adjusted cost basis carries forward into your replacement property. That means your full sale proceeds go toward your next acquisition rather than a reduced amount after taxes. Over multiple exchanges, this compounding effect can dramatically increase the scale of properties you control and the income they generate.

Deferring taxes on a $200,000 gain could keep an additional $40,000 to $60,000 actively working in your next deal rather than going straight to the government.

Upgrading assets without losing buying power

Another reason investors use 1031 exchanges is to trade up in property type or market without taking a taxable hit at each step. You might own a single-family rental that has appreciated significantly but no longer fits your investment goals. Rather than selling it and buying smaller after taxes, you can roll the full equity forward into a larger multifamily building, a commercial property, or a higher-growth market. This flexibility lets you reposition your portfolio based on strategy or market conditions without a forced reduction in purchasing power.

Eliminating deferred taxes through stepped-up basis

If you continue exchanging throughout your investing career and hold a property until death, your heirs receive a stepped-up cost basis equal to the fair market value at that time. Under current IRS rules, this means the accumulated deferred capital gains from every prior exchange can be eliminated entirely for your estate. No other widely available real estate strategy produces that magnitude of long-term tax outcome. This is why serious investors treat the 1031 exchange as a permanent portfolio strategy rather than a one-time event they stumble into between deals.

How a 1031 exchange works step by step

A 1031 exchange doesn't happen automatically when you sell an investment property. You must set it up before closing on your sale, and every step follows a specific sequence that the IRS requires. Understanding this sequence is the fastest way to see why the 1031 exchange explained properly demands preparation, not reaction.

Step 1: Sell your relinquished property

The process starts when you list and sell your existing investment property, which the IRS calls the "relinquished property." Before that closing happens, you need to signal your intent to exchange by notifying your escrow or title company and getting the right paperwork in place. You cannot touch the sale proceeds yourself at any point in this transaction.

The moment you receive the sale proceeds directly, the exchange is disqualified and the full capital gain becomes immediately taxable.

Step 2: Work with a qualified intermediary

Once your sale closes, the proceeds go directly to a qualified intermediary (QI), a neutral third party who holds the funds throughout your exchange. The IRS requires this structure under Treasury Regulation 1.1031. Your QI drafts the exchange agreement, holds your funds in a segregated account, and facilitates the transfer to your replacement property when you identify one. Choosing a reputable QI is critical since there is no federal licensing requirement for this role.

Step 3: Identify and close on your replacement property

From the day your relinquished property closes, two hard deadlines begin running simultaneously. You have 45 days to formally identify your replacement property in writing and 180 days total to close on it. Your QI then transfers the funds directly to the closing table, completing the exchange without the proceeds ever passing through your hands.

Rules that make or break eligibility

The IRS doesn't just reward investors for completing a sale and buying something new. Several specific eligibility requirements must be met for a 1031 exchange explained correctly to hold up under scrutiny. Missing even one of these rules means the exchange fails and your full capital gain becomes taxable immediately.

Like-kind property requirement

Real estate investors often assume "like-kind" means the property type must match exactly, but the IRS applies this term broadly. Any investment or business-use property can generally be exchanged for another, regardless of type. You can swap a single-family rental for a commercial strip mall, a vacant lot for a multifamily building, or an industrial warehouse for a retail center. Both properties must be held for investment or productive use in a trade or business, not for personal use, which means your primary residence does not qualify on either side of the exchange.

Since January 1, 2018, the Tax Cuts and Jobs Act limited 1031 exchanges to real property only, so equipment, vehicles, and other personal property no longer qualify under current IRS guidelines.

Equal or greater value rule

To defer 100% of your capital gains, your replacement property must be of equal or greater value than your relinquished property. You also need to reinvest all of the net equity, since any cash you receive from the exchange, called "boot," is taxable in the year it's received. Receiving $30,000 in boot because your replacement costs less means you owe capital gains taxes on that amount while the rest stays deferred.

Your lender plays a direct role here. If you carry debt on the relinquished property, you must replace it with equal or greater debt on the replacement property, or offset the difference with additional cash. Failing to do so creates taxable boot.

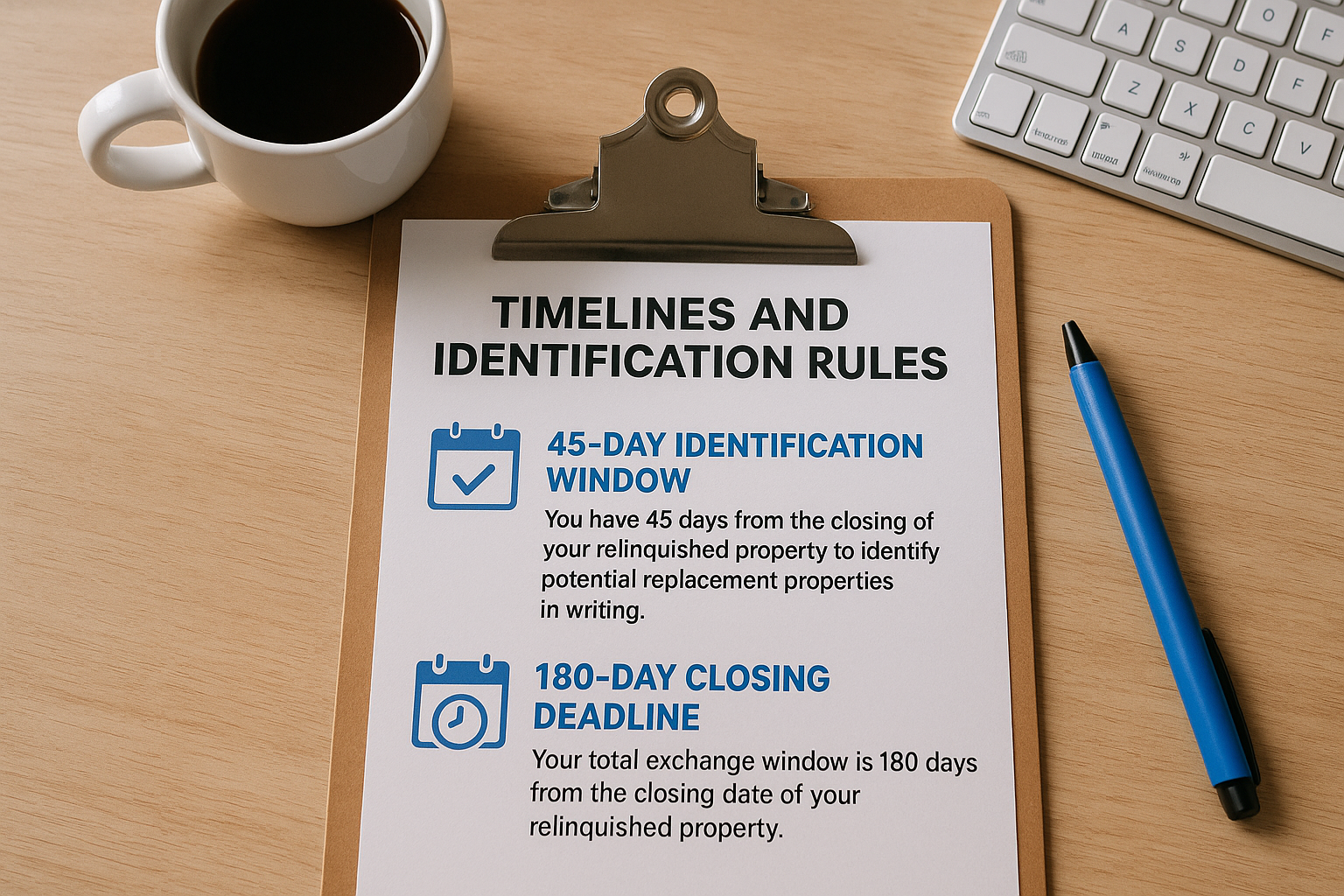

Timelines and identification rules

The two deadlines built into a 1031 exchange explained clearly are the features that cause the most problems for investors who don't prepare in advance. Both clocks start on the day your relinquished property closes, and neither one pauses for weekends, holidays, or unfinished negotiations on the replacement side. Missing either deadline means the exchange fails completely, and your full capital gain becomes taxable immediately.

The 45-day identification window

You have exactly 45 calendar days from the closing of your relinquished property to identify potential replacement properties in writing. This identification must be submitted to your qualified intermediary and must describe each property clearly enough for the IRS to confirm it. Vague descriptions or verbal agreements do not count.

If day 45 falls on a Sunday or federal holiday, the IRS does not grant an extension, so submit your identification letter well before the deadline.

The IRS gives you three identification rules to work within. You can use any one of the following:

- 3-Property Rule: Identify up to three properties regardless of their combined value.

- 200% Rule: Identify any number of properties as long as their combined fair market value does not exceed 200% of your relinquished property's sale price.

- 95% Rule: Identify any number of properties at any combined value, but you must close on at least 95% of the total identified value.

The 180-day closing deadline

Your total exchange window is 180 calendar days from the closing date of your relinquished property. You must take full title to your replacement property before this window closes. Note that the 180-day period and the tax return due date for the year of your sale interact directly. If your return is due before day 180, you may need to file an extension to protect your full exchange window, which the IRS permits under Publication 544.

Examples and common scenarios

Seeing real transactions makes the 1031 exchange explained process much easier to internalize. The rules and timelines described above apply to every investor, but the specific deal structures vary widely depending on where you are in your portfolio and what your next move looks like.

Investor trading up from a rental to multifamily

Say you purchased a single-family rental in 2015 for $150,000 and you sell it today for $350,000. After closing costs, your net sale proceeds are $330,000, with a capital gain of roughly $190,000. Without an exchange, you could owe $40,000 or more in combined federal and state capital gains taxes. With a 1031 exchange, those proceeds transfer directly to your qualified intermediary, and you have 45 days to identify a replacement property.

You use the full $330,000 as a down payment on a $1.1 million fourplex, financing the remaining balance with a DSCR loan based on the rental income the property produces, with zero tax triggered at closing.

Consolidating multiple properties into one asset

Some investors use the exchange to simplify their portfolios. You might own two smaller rental properties in different neighborhoods that are difficult to manage. By selling both in coordinated exchanges within the same 180-day window, you can roll the combined equity into one larger commercial or mixed-use property that generates more income with less management overhead. Each relinquished property requires its own qualified intermediary agreement, but a single replacement property can absorb proceeds from multiple exchanges simultaneously.

Rolling forward into a different market

Your local market may have peaked while another city shows stronger fundamentals. A 1031 exchange lets you reposition geographically without cashing out. You sell a Chicago-area property, identify a replacement in a growth market within 45 days, and preserve your full equity to compete in that new market at full buying power.

Next steps

A 1031 exchange explained from start to finish comes down to preparation, timing, and having the right team in place before you close your sale. You need a qualified intermediary lined up, a clear picture of your replacement property criteria, and a lender who understands how exchange financing works, particularly if you plan to use a DSCR loan or other investment-focused product to close on the replacement side.

Your next move is to map out your exit from your current property with those 45-day and 180-day deadlines built into the plan from day one. Waiting until after closing to figure out your financing almost always creates pressure that leads to mistakes. If you want to talk through your financing options for a replacement property, including DSCR loans, hard money, or conventional investment financing, connect with David Roa to work through your specific situation before the clock starts.