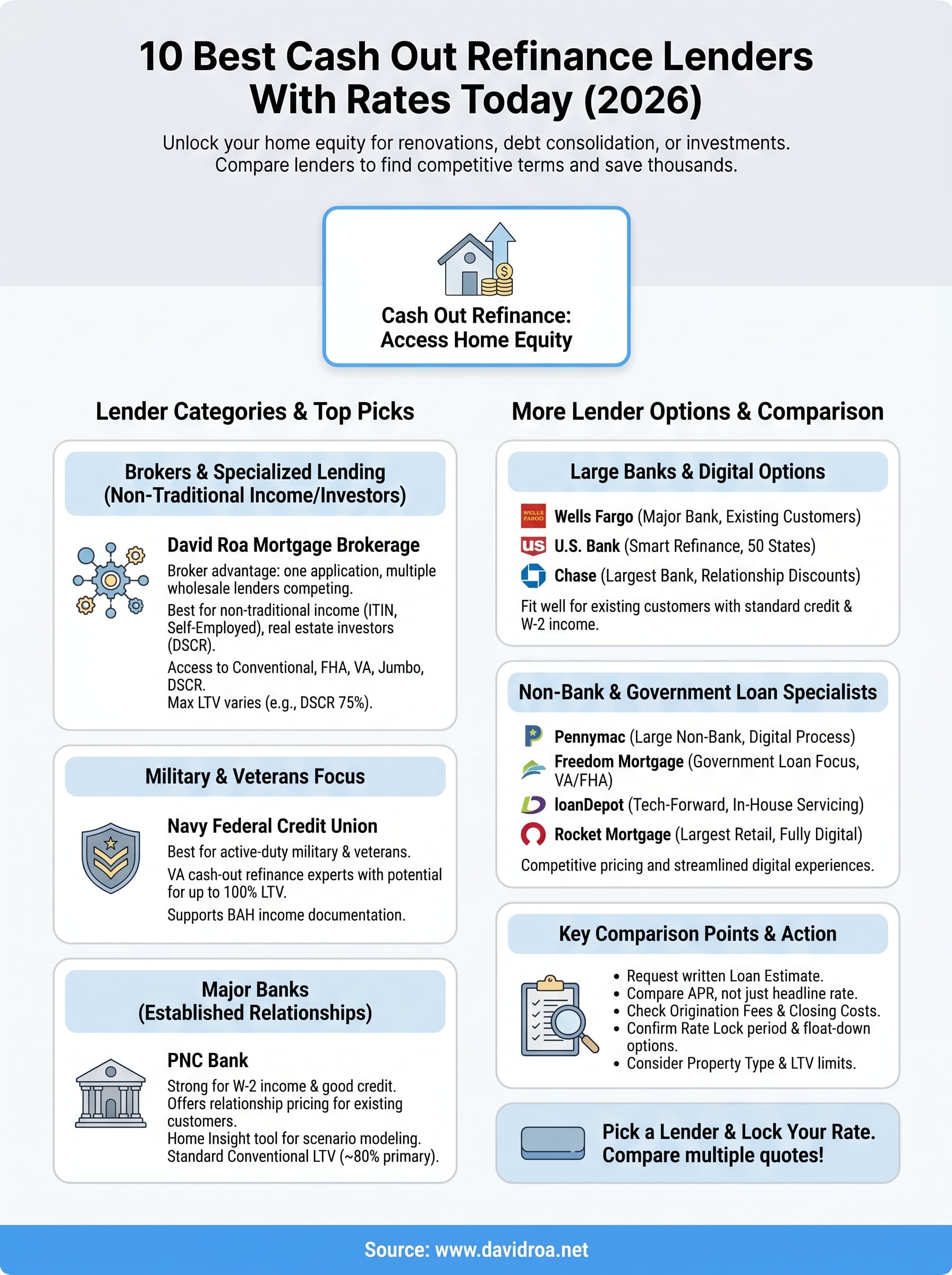

10 Best Cash Out Refinance Lenders With Rates Today (2026)

Your home equity is real money, and a cash-out refinance is one of the most practical ways to access it. Whether you need funds to renovate a property, consolidate high-interest debt, or invest in your next deal, choosing from the best cash out refinance lenders can mean the difference between a rate that works for you and one that costs you thousands over the life of the loan. With rates shifting throughout 2026, finding the right lender matters more than ever.

At David Roa, we've spent over 25 years originating mortgages and funding more than $150 million in loans across residential, commercial, and investment properties. As a mortgage broker and active real estate investor, I review lender products daily, not just on paper, but through the lens of someone who's actually closed on them. That hands-on experience is exactly what shaped this list. We work with a wide network of lending partners, and we know which ones deliver competitive terms and which ones fall short at the closing table.

Below, you'll find 10 cash-out refinance lenders worth considering right now, broken down by rates, eligibility requirements, and the types of borrowers each one serves best. Whether you're a homeowner tapping equity for the first time or an investor pulling capital from a rental property, this guide is built to help you compare your options and make a confident choice. Let's get into it.

1. David Roa Mortgage Brokerage

As a mortgage broker with over 25 years of origination experience and more than $150 million funded, David Roa brings something most lenders can't offer: direct access to dozens of wholesale lenders combined with the judgment of someone who actively invests in real estate. When you work with a broker rather than a single bank, you get a team that shops the market on your behalf and submits your scenario to multiple underwriters at once, which routinely produces better terms than walking into a single retail branch.

How David Roa structures cash-out refinances

The process starts with a clear review of your property equity, current loan balance, and financial goals. From there, the team identifies which wholesale lending partners offer the most competitive pricing for your specific profile. Because the brokerage isn't tied to one product shelf, you benefit from genuine rate competition across multiple capital sources rather than one lender's fixed rate sheet.

Working with a broker means one application, multiple lenders competing for your loan, and pricing you simply can't get by going direct to a single bank.

Where David Roa fits best

This brokerage stands out for borrowers with non-traditional income documentation, including ITIN holders, self-employed borrowers, and real estate investors who qualify through property cash flow rather than W-2s. If another lender has already turned you down or quoted rates that feel steep, running your scenario through a broker network is a logical next move.

Investment property owners also find a natural fit here. David Roa handles DSCR cash-out refinances, which let rental property owners pull equity based on the property's income rather than personal tax returns, one of the more useful tools among the best cash out refinance lenders in this market.

Cash-out limits and loan types to ask about

The brokerage has access to conventional, FHA, VA, jumbo, and DSCR loan programs, so cash-out limits vary by product and property type. Conventional loans typically cap cash-out at 80% LTV on primary residences, while DSCR investor loans may allow up to 75% LTV. Ask specifically about programs that match both your property type and your documentation situation.

What to compare when you request a quote

Request the loan estimate in writing so you can compare the APR, origination fees, and closing costs directly against any competing offer. Also ask about the rate lock period and whether a float-down option is available if rates improve before your closing date.

2. Navy Federal Credit Union

Navy Federal Credit Union is the largest credit union in the United States, serving active-duty military, veterans, and their immediate family members. If you meet the membership requirements, Navy Federal regularly offers some of the most competitive mortgage rates available, making it a strong entry on any list of the best cash out refinance lenders.

How Navy Federal handles cash-out refinances

Navy Federal offers cash-out refinances on conventional and VA loan products, with the VA cash-out option being a particular strength. The application process runs through their online portal or by phone, and their loan officers specialize in military-specific financial scenarios, which speeds up approvals for eligible borrowers.

VA cash-out refinances through Navy Federal can allow eligible veterans to refinance up to 100% of their home's appraised value, a ceiling most conventional lenders don't come close to matching.

Where Navy Federal fits best

Navy Federal is the right call if you hold VA loan eligibility and want to maximize how much equity you pull out. It also serves members who prefer working with a lender that understands military pay structures, deployment gaps, and BAH income documentation rather than forcing your profile into a standard bank underwriting box.

Cash-out limits and loan types to know

For VA cash-out refinances, eligible borrowers can access up to 100% LTV in many cases. Conventional cash-out programs follow standard limits closer to 80% LTV depending on your credit profile and property type.

What to compare when you request a quote

Ask Navy Federal for the full loan estimate with all closing costs itemized, and compare their VA funding fee structure against the rate savings before committing.

3. PNC Bank

PNC Bank is one of the largest regional banks in the U.S., operating across more than 25 states with a full-service mortgage division that handles both purchase and refinance loans. For borrowers who prefer working with an established bank rather than an online lender or broker, PNC offers a straightforward path to tapping home equity.

How PNC handles cash-out refinances

PNC processes cash-out refinances through its retail branch network and online platform, with dedicated loan officers available throughout the application. The bank uses conventional loan guidelines for most cash-out refinances and offers a digital tracker so you can follow your file's progress from submission to closing.

PNC's Home Insight tool lets you model different loan scenarios before you apply, which can help you decide how much equity to pull and what rate environment makes the math work.

Where PNC fits best

PNC works best for borrowers with strong W-2 income and established credit profiles who want the stability of a traditional bank relationship. If you already bank with PNC, you may qualify for relationship pricing that shaves a portion off your rate. This makes PNC worth checking when you're comparing the best cash out refinance lenders alongside other retail options.

Cash-out limits and loan types to know

PNC follows conventional cash-out limits, generally capping at 80% LTV on primary residences. Investment properties carry stricter limits, so confirm the exact ceiling for your property type early.

What to compare when you request a quote

Request the full loan estimate and pay close attention to origination fees and discount points, since retail banks often build margin into points rather than displaying it directly in the rate.

4. Wells Fargo

Wells Fargo is one of the largest mortgage lenders in the country by volume, with a nationwide branch network and a long track record in both purchase and refinance lending. For borrowers who want the backing of a major institution when exploring the best cash out refinance lenders, Wells Fargo offers broad product availability and dedicated home lending advisors in most markets.

How Wells Fargo handles cash-out refinances

Wells Fargo processes cash-out refinances through its online application platform and in-person branch locations, giving you flexibility in how you engage. Their loan officers guide you through income verification, appraisal scheduling, and underwriting on a timeline that typically mirrors other large retail banks. The digital portal lets you upload documents and track your loan status without calling in for updates.

Wells Fargo's existing customer relationships can work in your favor, as current account holders sometimes receive priority service and rate incentives during the application process.

Where Wells Fargo fits best

This lender fits borrowers who hold existing Wells Fargo checking or savings accounts and want to consolidate their financial relationship. It also suits applicants with conventional loan profiles, clean credit histories, and straightforward W-2 income documentation where the underwriting process moves quickly.

Cash-out limits and loan types to know

Wells Fargo follows standard conventional cash-out guidelines, capping most primary residence refinances at 80% LTV. Investment properties face tighter restrictions, so confirm the specific limit for your property before you apply.

What to compare when you request a quote

Ask for the complete loan estimate and compare the rate alongside origination charges and any discount points. Also confirm whether Wells Fargo's rate lock window matches your expected closing timeline.

5. U.S. Bank

U.S. Bank is one of the five largest commercial banks in the country, and its mortgage division operates in all 50 states with a full suite of refinance products. For borrowers who want the resources of a major institution combined with competitive loan pricing, U.S. Bank consistently earns a place among the best cash out refinance lenders reviewed by industry analysts each year.

How U.S. Bank handles cash-out refinances

U.S. Bank runs its cash-out refinance applications through both its digital mortgage portal and in-person branch network, giving you flexibility depending on how hands-on you want to be. Loan officers are assigned to your file directly, so you have a consistent point of contact from application through closing rather than bouncing between departments.

U.S. Bank's Smart Refinance option is a no-closing-cost product worth asking about if you want to preserve liquidity rather than roll fees into your new loan balance.

Where U.S. Bank fits best

This lender works well for existing U.S. Bank customers who hold checking accounts or other deposit relationships, since the bank often extends rate discounts to clients who consolidate their financial accounts. It also suits salaried borrowers with clean credit files who qualify under standard conventional underwriting guidelines without needing alternative documentation.

Cash-out limits and loan types to know

U.S. Bank follows conventional cash-out caps of 80% LTV on primary residences. Second homes and investment properties carry lower LTV ceilings, so confirm your property type's specific limit before you submit an application.

What to compare when you request a quote

Ask for the full loan estimate, then compare origination fees and any discount points against competing offers. Also confirm the rate lock duration and whether an extension is available if your closing runs longer than anticipated.

6. Pennymac

Pennymac is one of the largest non-bank mortgage lenders and servicers in the United States, handling billions of dollars in loan volume each year across conventional, FHA, VA, and jumbo products. Its scale gives it access to competitive pricing that often undercuts smaller retail competitors, which is why it regularly surfaces when borrowers compare the best cash out refinance lenders available in 2026.

How Pennymac handles cash-out refinances

Pennymac processes applications primarily through its digital platform, where you complete most of the loan file online and upload supporting documents without visiting a branch. Assigned loan officers stay with your file through closing, so you avoid being transferred between departments when questions come up during underwriting.

Pennymac's servicing scale means it processes a high volume of refinance transactions daily, which keeps its operational costs lower and can translate into sharper rate pricing for borrowers who qualify.

Where Pennymac fits best

Pennymac suits borrowers with conventional or government-backed loans who want a streamlined digital experience without sacrificing personal support. It also works well for existing Pennymac customers already in their servicing portfolio, since transferring fewer documents can speed up the process compared to applying with a new lender from scratch.

Cash-out limits and loan types to know

Pennymac follows standard conventional cash-out guidelines, capping primary residences at 80% LTV. FHA and VA cash-out options are also available, each with their own LTV and eligibility requirements depending on your property type.

What to compare when you request a quote

Ask Pennymac for the full loan estimate with all fees itemized, and compare both the rate and the closing cost total against other offers before committing.

7. Freedom Mortgage

Freedom Mortgage is one of the largest privately held mortgage companies in the U.S., with a strong focus on government-backed loans including FHA, VA, and USDA products. Its volume and specialization in these programs consistently positions it among the best cash out refinance lenders for borrowers who qualify under government loan guidelines.

How Freedom Mortgage handles cash-out refinances

Freedom Mortgage processes applications through its digital platform and a network of dedicated loan officers, with a particular strength in VA and FHA cash-out refinance programs. The company handles a high volume of government-backed transactions annually, which means its underwriters have deep experience with the specific documentation and eligibility requirements those programs demand.

Freedom Mortgage's focus on VA loans means eligible veterans often receive faster processing times and more competitive terms than they would from a general-purpose retail bank.

Where Freedom Mortgage fits best

This lender suits veterans, active-duty military members, and FHA borrowers who want a lender that handles government loan programs at scale. If you currently hold a VA loan and want to pull equity out of your home, Freedom Mortgage's familiarity with VA cash-out refinance requirements makes it worth including in your comparison.

Cash-out limits and loan types to know

VA cash-out refinances through Freedom Mortgage can reach up to 100% LTV for eligible borrowers, while FHA cash-out programs cap at 80% LTV based on the appraised value of your property.

What to compare when you request a quote

Ask for the complete loan estimate and confirm the VA funding fee structure and any lender credits that offset closing costs before you commit to a final rate.

8. loanDepot

loanDepot is one of the largest non-bank mortgage lenders in the country, originating billions of dollars in loan volume annually across conventional, FHA, VA, and jumbo products. Its fully digital origination platform and nationwide network of licensed loan consultants make it a flexible option for borrowers who want the efficiency of an online process without giving up direct human support.

How loanDepot handles cash-out refinances

loanDepot runs its cash-out refinance applications through its proprietary digital lending platform, where you can complete your application, upload documents, and track progress from one dashboard. Assigned loan consultants stay with your file throughout underwriting, so you're not handed off between teams when questions come up before closing.

loanDepot's in-house servicing operation means your loan doesn't disappear into a third-party servicer immediately after closing, which matters if you expect to need direct support down the line.

Where loanDepot fits best

This lender suits borrowers who want a tech-forward experience combined with licensed support at each step. It works particularly well for conventional and FHA borrowers who have clear documentation and want a fast, low-friction process that doesn't require visiting a branch at any point. When comparing the best cash out refinance lenders online, loanDepot consistently draws consideration for its competitive pricing on government-backed products.

Cash-out limits and loan types to know

loanDepot follows standard conventional guidelines, capping most primary residences at 80% LTV for cash-out refinances. FHA and VA cash-out options each carry their own eligibility thresholds depending on your credit profile and property type.

What to compare when you request a quote

Request the full loan estimate with closing costs itemized, and confirm the rate lock window matches your expected closing timeline before you move forward.

9. Chase

Chase is the consumer banking arm of JPMorgan Chase, the largest bank in the United States by assets, and its mortgage division operates across all 50 states with a full suite of refinance products. For borrowers who want the stability of the nation's biggest bank when evaluating the best cash out refinance lenders, Chase brings both scale and a well-developed digital platform to the process.

How Chase handles cash-out refinances

Chase processes applications through its online mortgage portal and in-person branch network, with home lending advisors available to guide you through each stage from application to closing. The bank's underwriting team handles a high volume of refinance transactions annually, which keeps the process predictable and well-documented for borrowers with standard income profiles.

Chase's DreaMaker loan program is worth asking about if your income falls within qualifying limits, as it offers reduced mortgage insurance costs compared to standard conventional products.

Where Chase fits best

Chase works best for existing Chase banking customers who qualify for relationship pricing tied to their checking or savings accounts. The bank also suits salaried borrowers with documented income and strong credit profiles who want a straightforward conventional cash-out refinance handled by a lender with deep operational resources.

Cash-out limits and loan types to know

Chase follows standard conventional guidelines, capping most primary residence cash-out refinances at 80% LTV. Investment properties and second homes carry tighter restrictions, so confirm the specific ceiling for your property type before you apply.

What to compare when you request a quote

Ask Chase for the full loan estimate with closing costs itemized, and verify whether relationship rate discounts apply to your account type before accepting the initial quote they provide.

10. Rocket Mortgage

Rocket Mortgage, operated by Rocket Companies, is the largest retail mortgage lender in the United States by origination volume. Its fully digital platform and heavy brand recognition make it one of the most searched names when borrowers start comparing the best cash out refinance lenders for 2026.

How Rocket Mortgage handles cash-out refinances

Rocket Mortgage runs its entire application through its proprietary online platform, where you complete your file, upload documents, and receive status updates without visiting a branch or mailing paperwork. The platform guides you step by step, and licensed mortgage bankers are available by phone or chat if you hit a question you can't resolve on your own.

Rocket Mortgage's technology investment means most borrowers receive a verified approval decision faster than they would at a traditional retail bank, which matters when rate locks are time-sensitive.

Where Rocket Mortgage fits best

This lender fits borrowers who prefer handling the entire process digitally and have straightforward conventional income documentation. It also works well for first-time refinancers who want a guided, low-pressure experience without navigating a branch relationship.

Cash-out limits and loan types to know

Rocket Mortgage follows standard conventional guidelines, capping most primary residence cash-out refinances at 80% LTV. FHA and VA cash-out programs are also available, each carrying their own eligibility and LTV requirements based on your credit profile.

What to compare when you request a quote

Ask for the full loan estimate with all fees itemized, and confirm whether any lender credits offset your closing costs before you lock a rate.

Pick a Lender and Lock Your Rate

Every lender on this list handles cash-out refinances differently, and the right choice depends on your specific profile: your income documentation, property type, credit score, and how much equity you plan to pull. Run your numbers, request loan estimates from at least two or three options, and compare the full APR alongside closing costs rather than just the headline rate. A lower rate with heavy origination fees can cost more than a slightly higher rate with minimal charges at closing.

Working with a broker gives you a built-in advantage when comparing the best cash out refinance lenders, because one application reaches multiple wholesale sources at once. If you want that kind of competitive access backed by 25 years of origination experience, reach out to David Roa Mortgage Brokerage and get a real quote tailored to your situation. Rates move fast in 2026, so the sooner you lock, the better your position.