How To Buy A House For The First Time: Step-By-Step

Figuring out how to buy a house for the first time can feel overwhelming, there are credit scores to worry about, down payments to save, loan types to compare, and a closing process that seems designed to confuse you. But here's the truth: it's far more manageable than it looks once you break it down into clear steps.

I'm David Roa, a mortgage broker and senior loan officer with over 25 years in the lending business and more than $150 million funded in residential, commercial, and investment loans. I've walked hundreds of first-time buyers through this exact process, from that first "can I even afford this?" conversation all the way to handing them the keys. Whether you're looking at FHA, VA, conventional, or even ITIN loans, I've seen what works and what trips people up.

This guide covers every step of buying your first home, from getting your finances in order to closing day. No jargon-heavy lectures, no vague advice, just a practical walkthrough built on what I've learned funding real deals for real people.

Before you start: know your numbers and goals

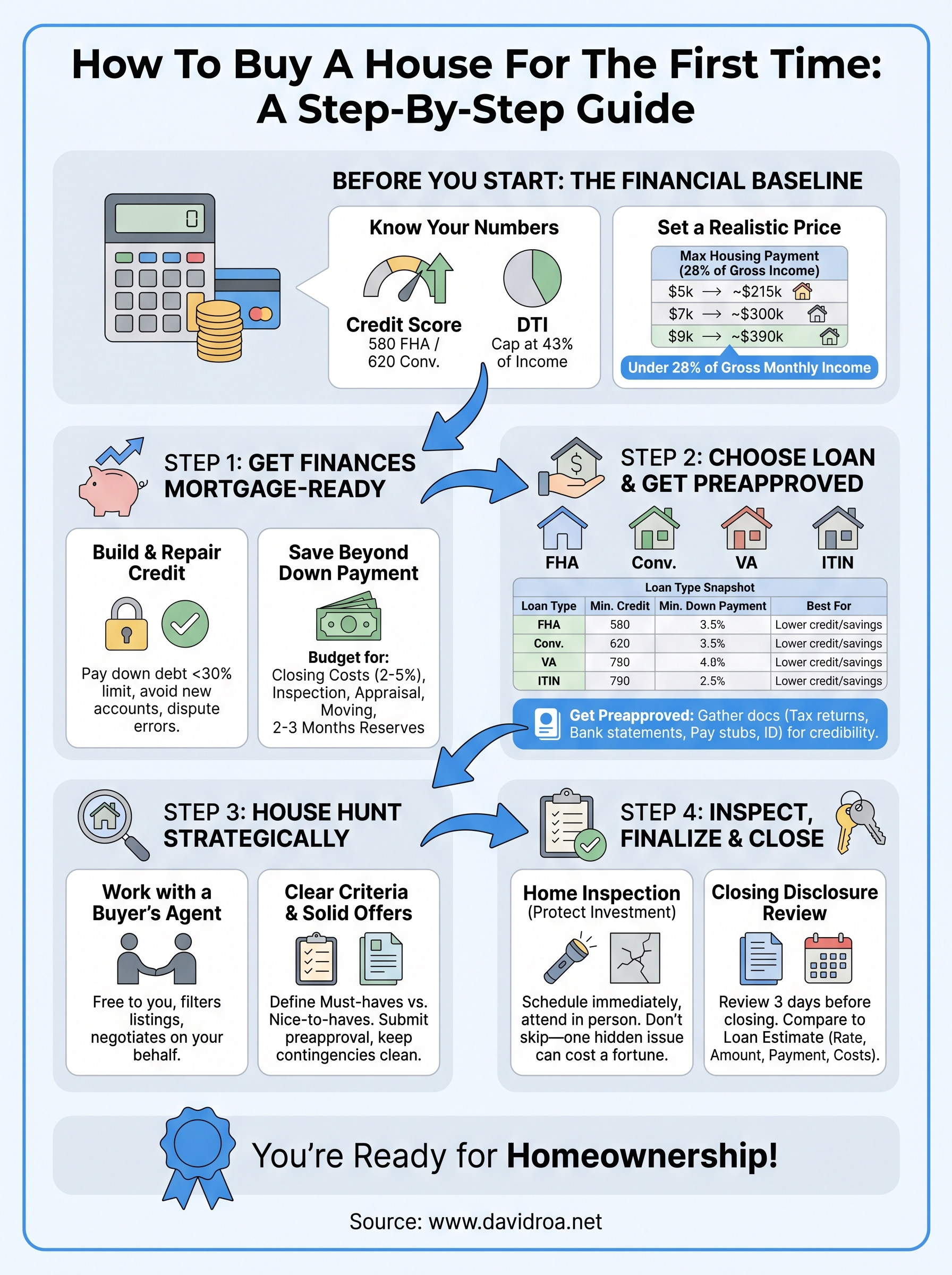

Before you book a single showing or talk to any lender, you need a clear financial baseline. Many first-time buyers skip this step and end up surprised by what they can or can't qualify for. Getting your numbers straight before you start shopping will save you time, prevent frustration, and put you in a much stronger position when you sit down to apply for a mortgage. Think of this as your pre-flight checklist for learning how to buy a house for the first time.

Know your credit score and debt-to-income ratio

Your credit score is the first thing every lender checks, and it determines which loan products are available to you and at what rate. Conventional loans typically require a score of 620 or higher, while FHA loans accept scores as low as 580 with a 3.5% down payment. Pull your free annual credit report at AnnualCreditReport.com to catch any errors before a lender does.

Your debt-to-income ratio (DTI) matters just as much. Add your monthly debt payments (car loans, student loans, credit cards) and divide by your gross monthly income. Most lenders cap DTI at 43% after including your projected mortgage payment. Paying down a credit card or two before applying can meaningfully improve both your approval odds and your interest rate.

On a $300,000 loan, a one-point improvement in your rate saves roughly $60,000 over 30 years, so cleaning up your credit before you apply is worth the effort.

Set a realistic purchase price before you search

Running the math before you fall in love with a property protects you from overextending. A reliable starting point is keeping your total housing payment (principal, interest, taxes, and insurance) under 28% of your gross monthly income. Here's how that looks across common income levels:

| Gross Monthly Income | Max Housing Payment (28%) | Estimated Home Price |

|---|---|---|

| $5,000 | $1,400 | ~$215,000 |

| $7,000 | $1,960 | ~$300,000 |

| $9,000 | $2,520 | ~$390,000 |

These figures assume a 30-year fixed loan at 7% interest and shift based on your down payment, local taxes, and insurance costs. Use this table as a starting point, then refine it with real quotes once you move into preapproval.

Step 1. Get your finances mortgage-ready

Once you know your numbers, you need to actively shape your financial profile before submitting a mortgage application. Lenders look at several factors simultaneously, and small improvements you make now can translate directly into better loan terms and lower monthly payments over the life of your loan.

Build or repair your credit before you apply

Your credit history affects both your approval odds and your interest rate. Pay down revolving balances to below 30% of each card's credit limit, and avoid opening any new accounts in the three to six months before you apply. If you spot errors on your report, dispute them directly through the official sites for Experian, Equifax, or TransUnion.

A 40-point score improvement can reduce your mortgage rate by 0.5% or more, which adds up to tens of thousands of dollars saved over 30 years.

Save beyond your down payment

Most first-time buyers lock in on the down payment and overlook the additional upfront costs that hit at closing. Budget for all of these before you start the how to buy a house for the first time process in earnest:

- Closing costs: Typically 2-5% of the loan amount

- Home inspection: $300-$500 on average

- Appraisal fee: $400-$700

- Moving costs: Plan for at least $1,000-$3,000

- Cash reserves: Most lenders want to see 2-3 months of mortgage payments in savings after closing

Step 2. Choose a loan and get preapproved

With your finances in shape, your next task is selecting the right loan product and getting formally preapproved. Preapproval carries real weight with sellers and agents because it confirms you've been vetted by a lender, not just handed a rough ballpark. This step separates serious buyers from casual shoppers, and it's one of the most important moves you'll make when figuring out how to buy a house for the first time.

Understand which loan type fits your situation

Not every loan works for every buyer, and choosing the wrong product can cost you more money upfront or over time. Here's a quick breakdown of the most common options for first-time buyers:

| Loan Type | Min. Credit Score | Min. Down Payment | Best For |

|---|---|---|---|

| FHA | 580 | 3.5% | Lower credit scores, smaller savings |

| Conventional | 620 | 3% | Strong credit, avoiding long-term mortgage insurance |

| VA | No minimum | 0% | Active military or veterans |

| ITIN | Varies | 10-20% | Non-U.S. citizens without a Social Security number |

Each loan carries different requirements for documentation, reserve funds, and property condition. Match your loan to your actual financial profile rather than defaulting to whichever option has the lowest down payment.

How to get preapproved quickly

Gather your documents before you contact any lender. Most lenders need two years of tax returns, two months of bank statements, recent pay stubs, and a government-issued ID. Submit everything at once to avoid back-and-forth delays that stretch out your timeline.

A preapproval letter is typically valid for 60 to 90 days, so time your application to align with when you realistically plan to start making offers.

Step 3. House hunt with a clear strategy

Knowing how to buy a house for the first time means more than scrolling listings and booking showings. Without a clear strategy, you waste weekends on properties that don't fit your budget or goals, and you risk making emotional decisions that cost you money. Treat the search like a structured process, not a treasure hunt.

Work with a buyer's agent who knows your market

A good buyer's agent costs you nothing out of pocket since the seller typically covers the commission. Your agent's job is to filter listings, flag red flags, and negotiate on your behalf, so choose someone with direct experience in the neighborhoods you're targeting. Ask how many buyers they've represented in the last 12 months and how often their clients win in competitive situations.

Before every showing, build a non-negotiable checklist that separates deal-breakers from preferences. For example:

- Must-haves: Minimum square footage, number of bedrooms, school district, commute distance

- Nice-to-haves: Updated kitchen, garage, finished basement

- Automatic disqualifiers: Flood zone without insurance options, foundation issues, proximity to industrial sites

Make offers that actually stick

When you find the right property, speed and clarity win. Submit your preapproval letter with every offer and keep contingencies focused on what truly protects you, like inspection and financing, rather than layering in requests that make sellers nervous.

A clean offer with a solid preapproval letter often beats a higher offer with sloppy terms.

Step 4. Inspect, finalize, and close with confidence

You're close to the finish line, but this stage is where many first-time buyers rush and make costly mistakes. The inspection and closing process protects your investment, so slow down, read everything, and ask questions before you sign anything. Knowing how to buy a house for the first time means treating these final steps with the same discipline you brought to your finances.

Schedule your home inspection immediately after acceptance

Once a seller accepts your offer, book your inspection within 48 to 72 hours to stay inside your contingency window. Attend the inspection in person so the inspector can walk you through findings directly. After the inspection, you have three main options:

- Accept the property as-is if issues are minor

- Request repairs or a price reduction for significant defects

- Walk away if structural, electrical, or foundation problems are too severe

Never skip the inspection to make your offer more appealing. One hidden foundation issue can cost more than your entire down payment.

Understand your closing disclosure before closing day

Your lender sends a Closing Disclosure three business days before closing, and you need to compare it line by line against your Loan Estimate. Look specifically at your interest rate, loan amount, monthly payment, and closing cost totals to catch any unexpected changes. If numbers shifted, call your lender immediately and get a written explanation before you show up at the closing table.

Your next move

You now have a complete picture of how to buy a house for the first time, from cleaning up your credit to signing at the closing table. The process rewards preparation. Every step you take now, whether that's pulling your credit report, calculating your DTI, or gathering your tax returns, puts you closer to an accepted offer and a funded loan.

The biggest mistake first-time buyers make is waiting until everything feels perfect before reaching out to a lender. Start the conversation early so you know exactly where you stand and what to fix. That clarity turns a stressful process into a predictable one.

If you're ready to run your numbers and figure out which loan fits your situation, connect with David Roa for a free mortgage consultation. With over 25 years of lending experience and more than $150 million funded, you'll get straight answers and a clear path forward.