Conventional Loan Requirements: Credit, DTI, Down Payment

A conventional loan is the most common type of mortgage in the United States, and for good reason. It offers competitive rates, flexible terms, and none of the red tape that comes with government-backed programs. But meeting conventional loan requirements isn't automatic. Lenders look at your credit score, income, debt load, and savings before they'll approve you, and each factor carries real weight.

The problem is that most borrowers don't get a straight answer on what actually qualifies them until they're already deep into the process. That wastes time, creates stress, and sometimes kills deals that could have closed with better preparation upfront.

This guide breaks down every requirement you need to know, from minimum credit scores and debt-to-income ratios to down payment thresholds and documentation standards. With over 25 years of lending experience and more than $150 million funded, I've walked thousands of borrowers through this exact process at David Roa. What follows is the same information I share with clients sitting across my desk: practical, specific, and built to help you qualify.

What a conventional loan is and how it works

A conventional loan is a mortgage that a private lender issues without any backing from a federal government agency. That means no FHA insurance, no VA guarantee, and no USDA support standing behind the loan. Instead, Fannie Mae and Freddie Mac, two government-sponsored enterprises, set the eligibility guidelines that most lenders follow. When you get a conventional mortgage, your lender almost always sells it into the secondary market, where those guidelines determine whether the loan qualifies for purchase.

The difference between conventional and government-backed loans

The clearest way to understand a conventional loan is to compare it to the alternatives. FHA loans require mortgage insurance for the life of the loan if you put less than 10% down, and they carry stricter property condition standards. VA loans are only available to eligible veterans and active-duty service members, while USDA loans are restricted to specific rural and suburban geographic areas.

Conventional loans give you more flexibility on property type, occupancy, and loan purpose than any government-backed program on the market.

Those restrictions don't apply to conventional mortgages. You can use them to buy a primary residence, a second home, or an investment property. You can also use them for a purchase, a rate-and-term refinance, or a cash-out refinance. That range of eligible uses is one of the main reasons conventional loans represent the largest share of mortgages funded each year in the United States.

How conventional loans are structured

Most conventional loans come in fixed-rate and adjustable-rate formats. A fixed-rate loan locks your interest rate for the life of the loan, typically 15 or 30 years. An adjustable-rate mortgage starts with a fixed introductory period, often 5, 7, or 10 years, then adjusts annually based on a market index. The structure you choose affects your monthly payment, your total interest paid, and the level of rate risk you carry over the life of the loan.

Lender decisions around structure are also shaped by where the loan ends up after closing. Fannie Mae and Freddie Mac purchase qualifying loans from lenders, which frees up capital for the lender to fund more mortgages. To qualify for that purchase, your loan must meet specific standards around credit, income, assets, and loan size. Those are the same conventional loan requirements you'll spend most of this guide working through in detail.

Conforming vs. non-conforming conventional loans

Not all conventional loans follow identical rules. Conforming loans stay within the loan limits set annually by the Federal Housing Finance Agency and meet Fannie Mae and Freddie Mac purchase guidelines in full. Non-conforming loans, commonly called jumbo loans, exceed those limits and require lenders to either hold them in their own portfolio or sell them to private investors, which typically means stricter qualification standards and slightly higher interest rates.

For 2026, the conforming loan limit for a single-unit property sits at $806,500 in most parts of the country, with higher ceilings in designated high-cost markets. If your loan amount falls below that threshold and you meet the credit and income benchmarks, you're working with a conforming conventional loan. Borrowing above that limit puts you in jumbo territory, where documentation requirements and reserve standards shift considerably. Knowing which category your loan falls into before you apply saves time and helps you prepare the right paperwork from the start.

Why conventional loan requirements matter

Understanding the rules before you apply isn't just good preparation; it's the difference between a smooth closing and a denial letter. Conventional loan requirements exist because lenders need to measure risk precisely before they commit hundreds of thousands of dollars over 15 to 30 years. Every standard around credit, income, and assets tells the lender something specific about the likelihood you'll repay the loan without defaulting.

Why lenders set these standards

Lenders don't set these requirements arbitrarily. When a lender funds a conventional mortgage, it almost always sells that loan to Fannie Mae or Freddie Mac on the secondary market. For that sale to happen, the loan must meet published eligibility guidelines in full. If your file doesn't qualify, the lender can't sell the loan, which ties up their capital and increases their risk exposure significantly.

Meeting the guidelines isn't about clearing bureaucratic hurdles; it's about making your loan sellable, which directly affects what rates and terms lenders can realistically offer you.

Because these eligibility standards are consistent across lenders, they also protect you as a borrower. Understanding the debt-to-income thresholds before you apply, for example, lets you structure your finances in advance rather than discover a problem on the day underwriting begins.

What failing to meet requirements costs you

When your application falls short, the consequences are real and immediate. A low credit score typically results in either a denial or a significantly higher interest rate, and both outcomes affect the total cost of your loan across its entire term. A debt-to-income ratio above acceptable limits can stop an approval even when your gross monthly income looks strong on paper.

The less obvious cost is time. Borrowers who don't understand the standards often apply too early, receive a denial, and then spend months repairing their credit or paying down debt before trying again. That delay can mean missing a specific property, losing a rate lock, or watching home prices move against you in a competitive market.

Knowing exactly where the qualification thresholds sit gives you a clear target to work toward before you ever submit an application. The sections that follow break down each requirement in precise detail, starting with credit score minimums, so you understand what lenders look for and can prepare accordingly.

Conventional loan credit score requirements

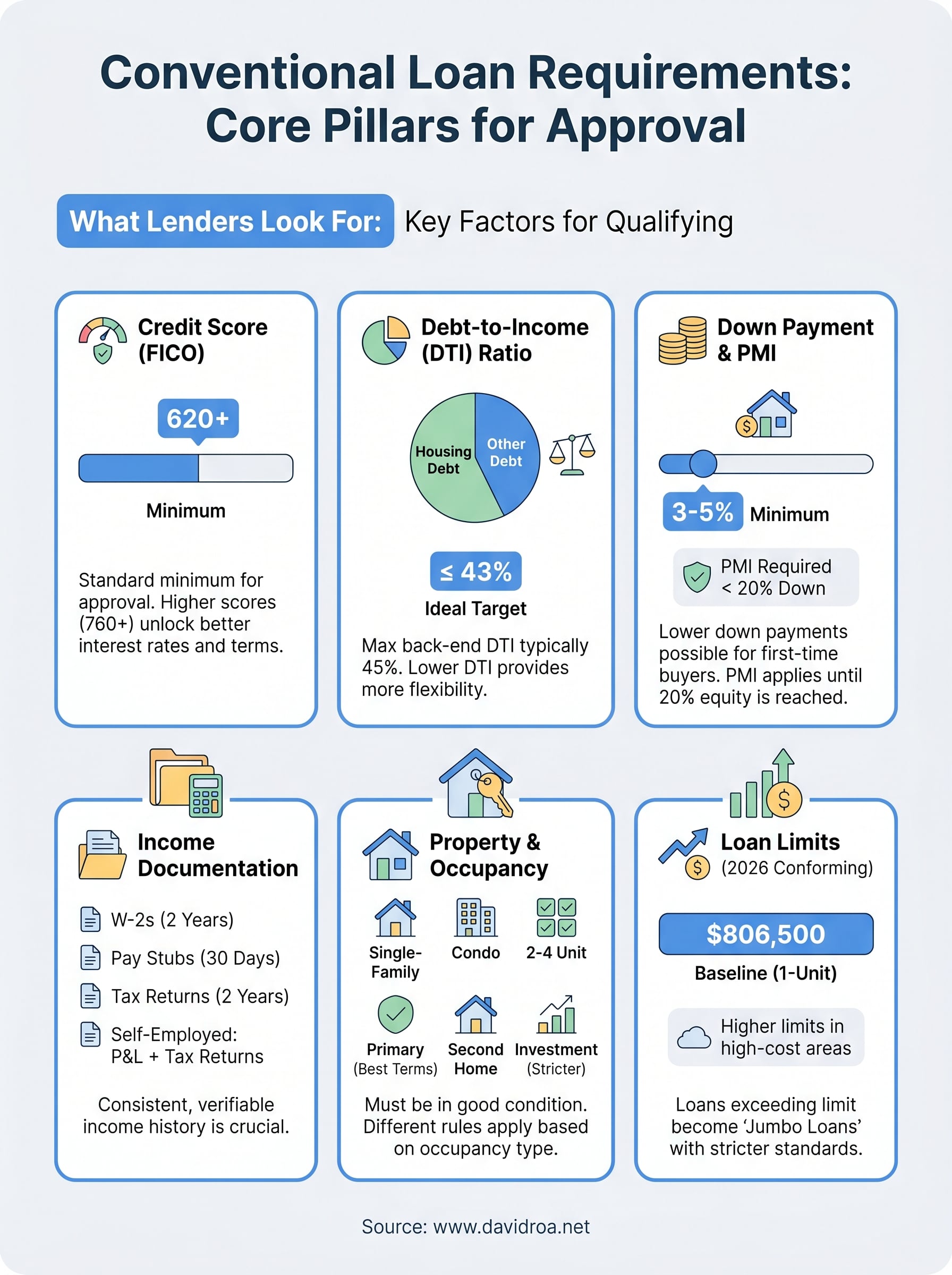

Your credit score is the first number an underwriter looks at when reviewing your file. It functions as a quick-read summary of your borrowing history, and lenders use it to determine both whether you qualify and what interest rate you'll pay. Meeting conventional loan requirements starts here, because a score below the minimum threshold stops the process before it begins.

The minimum score lenders accept

Most lenders require a minimum FICO score of 620 to approve a conventional mortgage. That's the floor set by Fannie Mae and Freddie Mac guidelines for conforming loans. Falling below 620 typically means your only options are government-backed programs like FHA, which carry their own tradeoffs.

That said, the 620 minimum applies to borrowers with strong compensating factors elsewhere in the file, such as a large down payment or low debt-to-income ratio. Lenders who see a borderline credit score often look harder at those other factors to decide whether the file is worth approving or pushing through automated underwriting systems.

Your score at the time of application is what counts, not the score you had six months ago or expect to have next year.

Here's how the credit score tiers typically map to loan eligibility:

| FICO Score Range | Eligibility |

|---|---|

| 760+ | Best available rates |

| 720-759 | Strong approval, competitive rates |

| 680-719 | Approved, moderate rate adjustments |

| 640-679 | Approved, higher rate adjustments |

| 620-639 | Minimum threshold, tightest conditions |

| Below 620 | Conventional loan not available |

How your score affects your rate

Lenders price conventional loans using loan-level price adjustments, which are risk-based fees tied directly to your credit score and loan-to-value ratio. A borrower with a 760 score and a 20% down payment gets the cleanest pricing. A borrower with a 640 score and 5% down pays a higher adjustment, which often shows up as a higher interest rate or additional closing costs.

The practical effect is significant across a 30-year loan term. A rate difference of even 0.5% to 0.75% adds tens of thousands of dollars in total interest paid. If your score sits in the lower ranges today, spending three to six months paying down revolving balances and correcting any reporting errors before applying can produce real savings across the life of your mortgage.

DTI and income requirements lenders use

Your debt-to-income ratio tells lenders how much of your gross monthly income already goes toward existing debt payments. It's the second major filter in conventional loan requirements, and it carries as much weight as your credit score. Lenders use DTI to measure whether you can realistically absorb a new mortgage payment without overextending your finances.

How lenders calculate your DTI

Lenders calculate two DTI figures: front-end and back-end. Front-end DTI measures your proposed housing payment, including principal, interest, taxes, and insurance, as a percentage of your gross monthly income. Back-end DTI measures all monthly debt obligations, including the new mortgage, divided by gross monthly income. Fannie Mae and Freddie Mac guidelines focus primarily on back-end DTI when evaluating risk.

The standard maximum back-end DTI for a conventional loan is 45%, though lenders can approve up to 50% when strong compensating factors like high reserves or excellent credit are present.

For most borrowers, staying below 43% back-end DTI gives you the most options across lenders and loan products. The lower your ratio, the more flexibility you have on rate negotiations and loan structure. If your DTI sits above 45%, paying down an installment loan or a credit card before applying can move your number into an approvable range.

Income documentation you'll need to provide

Lenders need to verify and document every income source you use to qualify. The exact paperwork depends on how you earn your income. W-2 employees typically provide two years of W-2s, two recent pay stubs, and federal tax returns. Self-employed borrowers must provide two years of complete tax returns along with a year-to-date profit and loss statement, and lenders use the average net income from both years after write-offs to calculate qualifying income.

Other income types follow specific documentation rules as well. Rental income from investment properties requires current lease agreements and Schedule E from your tax returns, and lenders typically use 75% of the gross rental income to account for vacancy and maintenance. Bonus income, commission income, and overtime pay all require a two-year history to count toward qualification, since lenders treat irregular earnings as less reliable than base salary. Gathering this documentation before you apply cuts underwriting delays and reduces the chance of a last-minute condition holding up your closing.

Down payment rules, PMI, and reserves

Your down payment size affects three things at once: your loan-to-value ratio, whether you pay private mortgage insurance, and the reserve requirements your lender applies to the savings you have left after closing. Understanding how these three factors connect gives you more control over your total monthly housing cost and the exact amount of cash you'll need to bring to the table.

How much down payment you actually need

Conventional loans don't require 20% down, despite what many first-time buyers assume. Fannie Mae and Freddie Mac both allow down payments as low as 3% for qualifying borrowers, though that minimum applies primarily to first-time buyers purchasing a primary residence. Standard purchase transactions typically require at least 5% down, and investment properties carry higher requirements, often 15% to 25% depending on the number of units.

Here's how down payment thresholds map to different loan scenarios:

| Property Type | Minimum Down Payment |

|---|---|

| Primary residence (first-time buyer) | 3% |

| Primary residence (repeat buyer) | 5% |

| Second home | 10% |

| Investment property (1 unit) | 15% |

| Investment property (2-4 units) | 25% |

When PMI kicks in and how to remove it

Private mortgage insurance is required on conventional loans whenever your down payment falls below 20%. PMI protects the lender, not you, in the event of default, and it adds a monthly cost that typically runs between 0.5% and 1.5% of the loan amount annually, depending on your credit score and loan-to-value ratio. On a $400,000 loan, that translates to an extra $166 to $500 per month on top of your principal, interest, taxes, and insurance.

Once your loan balance drops to 80% of the original appraised value, you can request PMI cancellation in writing, and lenders must remove it automatically when you reach 78% loan-to-value under the Homeowners Protection Act.

Reserve requirements lenders expect

Reserves are the funds you have remaining after closing, and lenders check them to confirm you can handle your mortgage payment if your income temporarily drops. Most conventional loan requirements call for at least two months of mortgage payments held in liquid assets once your down payment and closing costs clear. Investment properties and borrowers with multiple financed properties often face reserve standards of six to twelve months.

Acceptable reserve sources include checking accounts, savings accounts, and vested retirement funds. Lenders verify reserves through bank statements covering the most recent 60 days, so any large deposits during that window will require a paper trail explaining their origin before underwriting can clear your file.

Property, occupancy, and appraisal requirements

Your credit score and income aren't the only factors lenders evaluate. Conventional loan requirements also cover the property itself, how you plan to use it, and whether an independent appraiser confirms its value supports the loan amount. Getting these details wrong can delay your closing or change your loan terms even after you've already been pre-approved.

Property types lenders will finance

Conventional loans cover a wide range of residential property types, including single-family homes, two-to-four-unit multifamily properties, condominiums, and planned unit developments. Each type carries its own set of standards. Condominiums, for example, must meet Fannie Mae or Freddie Mac project approval requirements, meaning the condo association's financials, insurance coverage, and owner-occupancy ratios all factor into your loan eligibility.

Properties must also be in acceptable physical condition at the time of closing. Lenders won't fund loans on homes with significant structural damage, health hazards, or major deferred maintenance unless you resolve those issues before closing. Unlike FHA loans, conventional guidelines don't mandate a separate property inspection, but the appraisal itself flags conditions that could affect the safety or livability of the home.

How occupancy type changes your qualification

Lenders treat primary residences, second homes, and investment properties differently because each carries a distinct risk profile. A primary residence is the property you intend to occupy as your main home, and it receives the most favorable terms across down payment minimums, interest rates, and reserve requirements. A second home must be a reasonable distance from your primary residence and cannot be subject to a rental management agreement, or lenders will reclassify it as an investment property, which triggers stricter standards.

Investment properties face the tightest qualification criteria because borrowers are statistically more likely to default on a property they don't personally occupy.

What the appraisal process covers

An independent licensed appraiser evaluates the property and produces a report that lenders use to confirm the home's market value supports your loan amount. The appraiser compares your property to recent sales of similar homes nearby, adjusting for differences in size, condition, location, and features. If the appraised value comes in below your purchase price, you'll need to renegotiate the contract, increase your down payment, or walk away from the deal.

Lenders order the appraisal through an appraisal management company to maintain independence from the transaction. You pay for it, typically between $400 and $700, and the completed report belongs to the lender. Review it carefully, because factual errors in comparable selections or square footage calculations can support a formal rebuttal if the value appears understated.

Conforming loan limits and jumbo rules for 2026

The loan amount you're borrowing determines which set of conventional loan requirements applies to your file. In 2026, the Federal Housing Finance Agency set the baseline conforming loan limit at $806,500 for a single-unit property in standard-cost markets. If your loan falls at or below that threshold and your credit and income meet Fannie Mae and Freddie Mac standards, you're working with a conforming conventional loan and the full range of competitive rates that come with it.

How the 2026 conforming limit works across property types and markets

The $806,500 baseline applies to single-family homes in most counties, but the limit scales up for properties with multiple units and for homes in designated high-cost areas. In high-cost markets, the conforming ceiling reaches as high as $1,209,750 for a single-unit property, which covers many counties in California, Hawaii, New York, and parts of the Pacific Northwest. Borrowing above the local conforming limit in any of these areas pushes your loan into jumbo territory, regardless of how strong your credit file looks.

Here's how the 2026 conforming limits break down by property type in standard markets:

| Property Units | 2026 Conforming Limit |

|---|---|

| 1 unit | $806,500 |

| 2 units | $1,032,650 |

| 3 units | $1,248,150 |

| 4 units | $1,551,250 |

What jumbo loans require from borrowers

Once your loan amount exceeds the local conforming limit, lenders can no longer sell the loan to Fannie Mae or Freddie Mac, so they either hold it in their own portfolio or sell it to private investors. That shift in risk means stricter qualification standards across every part of your file. Most jumbo lenders require a minimum FICO score of 700 to 720, compared to the 620 floor on conforming loans, and many push that threshold higher for larger loan amounts.

The documentation burden on jumbo loans is heavier than on conforming loans, so gathering your financial records early in the process prevents delays once underwriting begins.

Reserve requirements are also significantly higher in the jumbo space. Where a conforming loan might require two to three months of reserves, jumbo lenders typically want six to twelve months of mortgage payments sitting in liquid accounts after closing. Down payment minimums run higher as well, with most lenders requiring at least 10% to 20% down, and some lenders setting a firm 20% floor depending on loan size and credit profile.

How to qualify for a conventional loan step by step

Qualifying for a conventional loan is straightforward when you work through the process in the right order. Rushing into an application before your credit, income, and documentation are ready is the most common reason borrowers face delays or denials. Follow these steps in sequence, and you'll enter underwriting with a clean, complete file.

Check your credit score and fix what you can

Start by pulling your credit reports from all three bureaus at AnnualCreditReport.com. Look for reporting errors, duplicate accounts, or outdated negative items that shouldn't still appear. Disputing inaccurate entries before you apply can move your score meaningfully in 30 to 60 days. If your score sits below 680, focus on paying down revolving balances to below 30% utilization on each card before submitting your application.

Calculate your DTI and identify what to pay off

Add up every minimum monthly debt payment on your credit report, then divide by your gross monthly income. If the result exceeds 43%, look at which accounts you can eliminate or reduce before applying. Paying off a small installment loan or a high-balance credit card often produces the fastest DTI improvement. You don't need to eliminate all debt; you just need the ratio to fall within the range that conventional loan requirements allow.

Gather documentation before you apply

Collect your two most recent W-2s, 30 days of pay stubs, and two years of federal tax returns before you contact a lender. If you're self-employed, add a year-to-date profit and loss statement. Pull 60 days of bank statements for every account you plan to use for your down payment and reserves. Having this package ready before your first lender conversation compresses the timeline from application to clear-to-close significantly.

Borrowers who submit complete documentation at application consistently close faster than those who provide documents in pieces throughout the process.

Get pre-approved and lock your rate at the right time

Submit your complete file for a formal pre-approval, not a pre-qualification. A pre-approval involves verified income and credit review, which makes your offer stronger in a competitive market. Once you're under contract, discuss rate lock timing with your lender. Rates shift daily, and locking too early or too late can cost you on a loan this size. Your lender should walk you through the lock options that match your expected closing timeline so you're not left exposed to market movement at the wrong moment.

Quick recap and next steps

Conventional loan requirements cover six core areas: credit score, debt-to-income ratio, down payment, income documentation, property standards, and loan limits. A minimum 620 FICO score gets you in the door, but stronger credit unlocks better pricing. Keeping your back-end DTI below 43% gives you the widest approval options, and your down payment determines whether PMI applies and how much you'll need in reserves after closing. Jumbo loans above $806,500 raise the bar across every category, so knowing which loan size you're targeting shapes your preparation from the start.

Preparation is what separates borrowers who close on time from those who spend months fixing problems that could have been resolved before the first application. Pull your credit reports, document your income, and run your DTI numbers before you contact a lender. When you're ready to move forward, connect with David Roa to work through your specific situation and find the right loan for your goals.