How To Get A VA Loan Certificate Of Eligibility (COE)

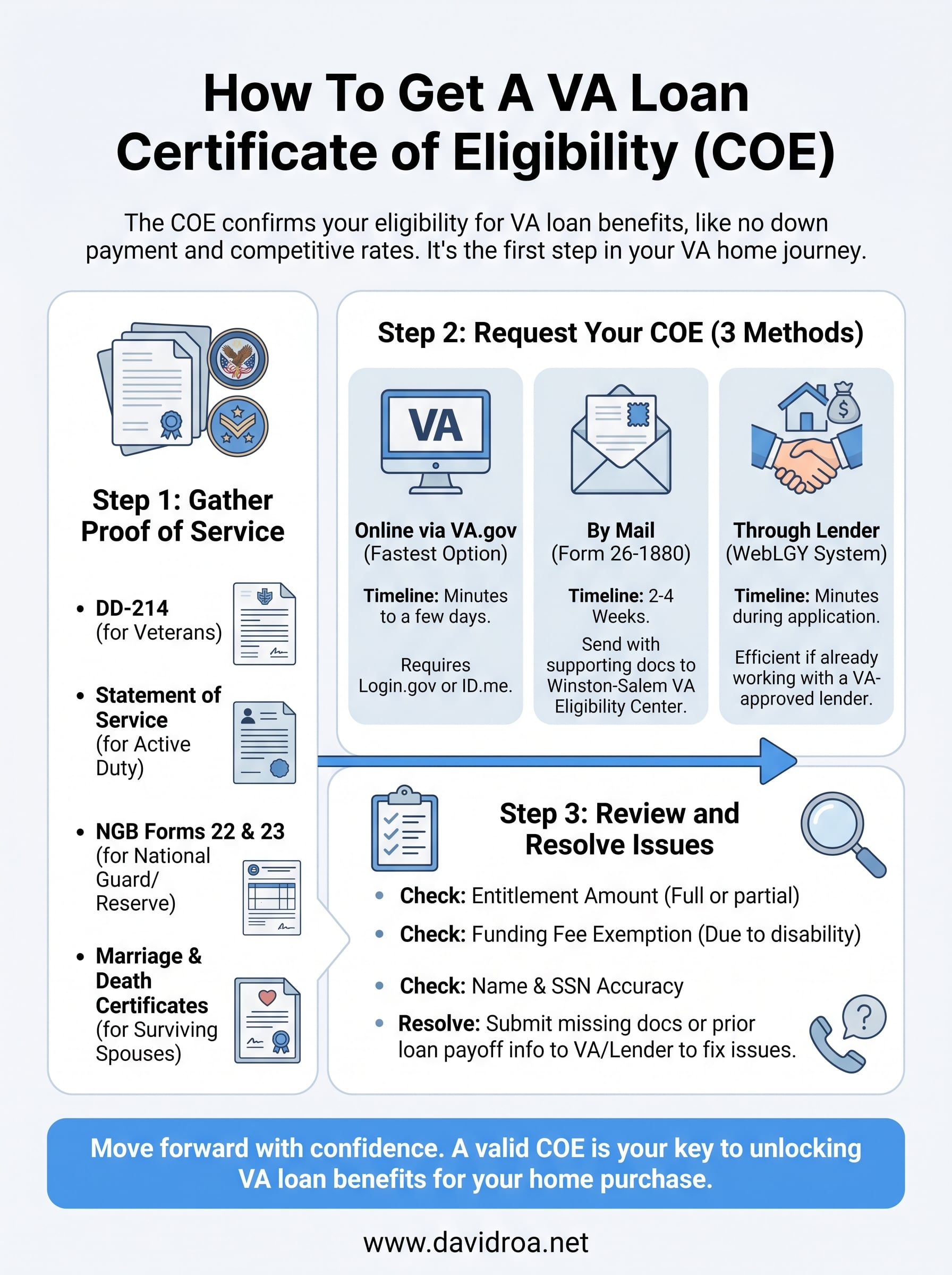

Before you can use your VA loan benefit to buy a home, you need one document first: the Certificate of Eligibility, or COE. If you're wondering how to get a VA loan Certificate of Eligibility, the process is more straightforward than most veterans and service members expect. The COE is simply the VA's confirmation that you meet the minimum service requirements for a VA-backed home loan, and without it, no lender can move your application forward.

The good news is you have multiple ways to request it, some taking minutes and others a few weeks. Whether you apply online through the VA's eBenefits portal, submit a request by mail, or have your lender pull it directly, each method gets you to the same result. The key is knowing which route fits your situation and what documents you'll need to have ready. As a senior loan officer with over 25 years of mortgage experience, I've helped countless veterans at David Roa navigate exactly this step, and I can tell you that a little preparation here saves a lot of headaches later.

This guide breaks down every method for obtaining your COE, the specific forms and paperwork required based on your service status, and what to do if your eligibility needs to be restored. By the end, you'll have a clear path from request to approval so you can move forward with your VA home purchase with confidence.

What a VA COE is and what you need before you start

The Certificate of Eligibility (COE) is an official document issued by the U.S. Department of Veterans Affairs that confirms you have met the minimum service requirements for a VA-backed home loan. Your lender uses it as proof that the VA will guarantee a portion of your mortgage, which is what unlocks the program's core benefits: no down payment on most purchases, no private mortgage insurance, and access to competitive interest rates. Without a valid COE, your loan file is incomplete, and no underwriter will approve a VA mortgage regardless of how strong your finances are.

What the COE actually proves

Your COE does more than confirm basic eligibility. It also tells your lender your entitlement amount, which is the dollar figure the VA will guarantee on your behalf. For most veterans using a VA loan for the first time, full entitlement means no loan limits apply in areas where the VA has restored your benefit completely. The COE also displays your funding fee exemption status, which shows whether you qualify for a waiver due to a service-connected disability rating. This single document gives your lender all the service-verification data they need to price your loan and move your application forward.

A COE confirms VA eligibility only. Your lender still evaluates your credit, income, debt load, and the property itself before approving the actual loan.

Who qualifies for a VA COE

Knowing which category applies to you is a critical step before figuring out how to get a VA loan Certificate of Eligibility, because your service background determines exactly which documents you will need. The VA extends COE eligibility to the following groups:

| Borrower Type | Basic Requirement |

|---|---|

| Active-duty service member | 90 continuous days of current active service |

| Wartime veteran | 90 days of active duty during a qualifying wartime period |

| Peacetime veteran | 181 days of continuous active duty during peacetime |

| National Guard / Reserve member | 6 years of service, or federal activation for at least 90 days |

| Surviving spouse | Veteran died in service or from a service-connected disability; spouse has not remarried (or remarried after age 57) |

Each category carries its own documentation requirements, which is why knowing your status before you begin saves you from submitting the wrong forms and waiting through unnecessary delays.

What to have ready before you apply

Before you start any submission method, gather the core identifying information the VA and your lender will need. At a minimum, have your Social Security number, your full legal name as it appears on military records, and your dates of service accessible. Veterans will almost certainly need their DD-214 (Certificate of Release or Discharge from Active Duty). Active-duty members typically need a current statement of service signed by a commanding officer or adjutant. Surviving spouses generally need the veteran's DD-214, the marriage certificate, and the veteran's death certificate. Organizing these documents before you submit anything keeps the process moving and reduces the chance of a request coming back incomplete.

Step 1. Gather the right proof of service

Your proof of service is the foundation of the entire COE process. The VA won't issue your certificate without documentation that confirms your service dates and discharge status, and submitting the wrong form for your situation is one of the most common reasons applications stall. Before you think about how to get a VA loan Certificate of Eligibility, nail down which document category applies to you and make sure you have a clean, legible copy ready to submit.

DD-214: The document most veterans need

If you separated or retired from active-duty service, the DD-214 (Certificate of Release or Discharge from Active Duty) is what you need. It records your service dates, character of discharge, and military occupational specialty. Request Copy 4 (Member 4), which includes your discharge characterization. An honorable discharge or a general discharge under honorable conditions qualifies you; a dishonorable discharge does not.

If you've lost your DD-214, request a replacement through the National Archives' National Personnel Records Center at archives.gov before you start your COE application.

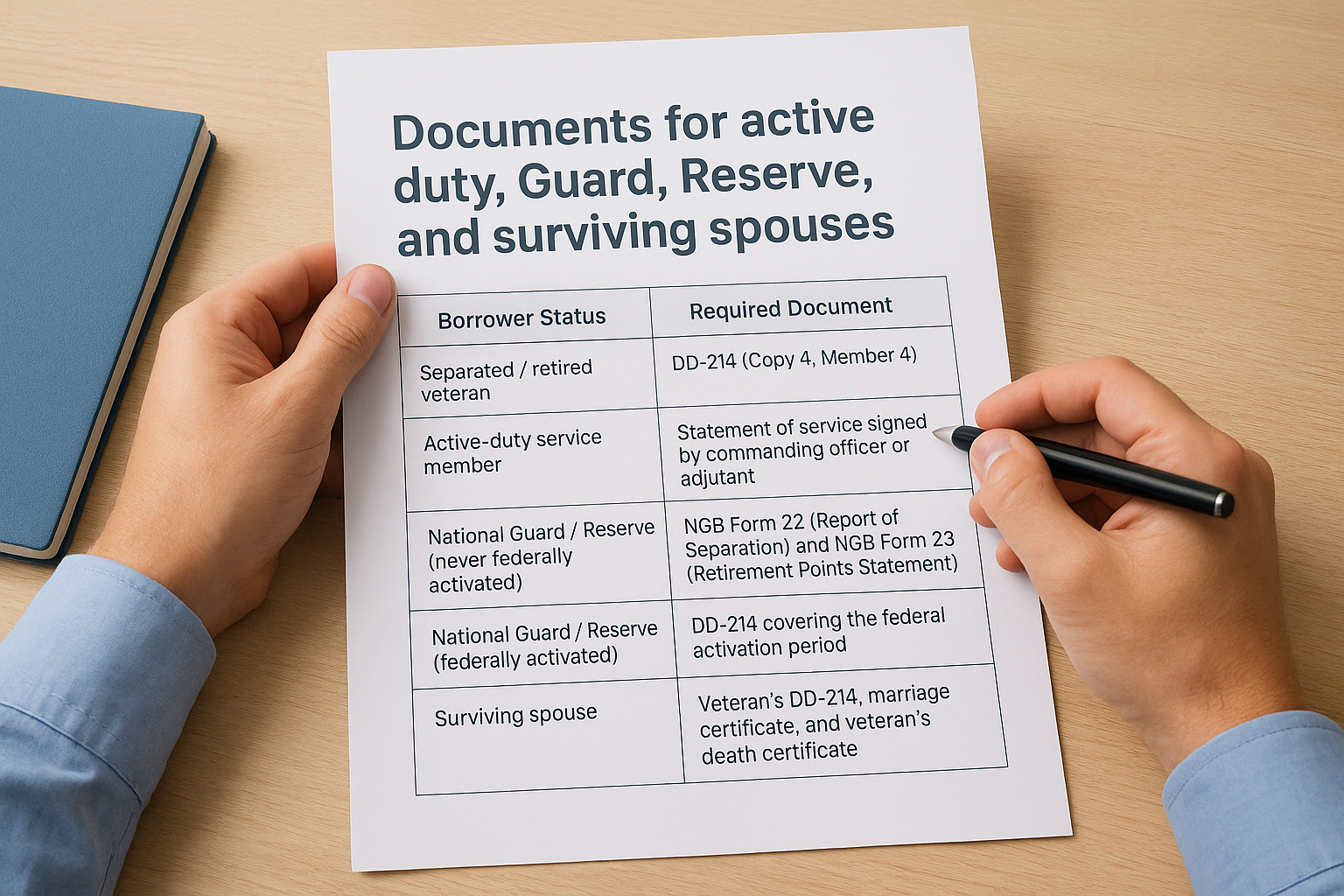

Documents for active duty, Guard, Reserve, and surviving spouses

Required paperwork varies based on your current service status, and submitting the wrong document adds unnecessary days to your timeline. Match your situation to the table below before you apply.

| Borrower Status | Required Document |

|---|---|

| Separated / retired veteran | DD-214 (Copy 4, Member 4) |

| Active-duty service member | Statement of service signed by commanding officer or adjutant, including your name, SSN, date of birth, entry date, active service duration, and any lost time |

| National Guard / Reserve (never federally activated) | NGB Form 22 (Report of Separation) and NGB Form 23 (Retirement Points Statement) |

| National Guard / Reserve (federally activated) | DD-214 covering the federal activation period |

| Surviving spouse | Veteran's DD-214, marriage certificate, and veteran's death certificate |

Once your documents are organized and confirmed accurate, you're in a strong position to choose your submission method in the next step.

Step 2. Request your COE online, by mail, or via lender

Once your proof of service documents are ready, you have three distinct methods to request your COE. Understanding each one helps you choose the fastest and most practical path for your specific situation. This is the core of knowing how to get a VA loan Certificate of Eligibility: picking the right channel from the start.

Online through VA.gov

The fastest option for most veterans is the VA's online portal at VA.gov. Sign in with a verified ID.me or Login.gov account, navigate to the "Records" section, and select "Apply for a VA home loan COE." The system pulls your service records automatically in many cases, and you may receive your COE within minutes if your discharge data is already in the VA's system. If the system can't verify your records automatically, you'll get a prompt to upload your supporting documents directly.

For active-duty members, your records may not yet be fully digitized, so have your statement of service ready to upload before you start.

By mail using VA Form 26-1880

If you prefer a paper process or have a complex service history, submit VA Form 26-1880 (Request for a Certificate of Eligibility) by mail. Download the form from VA.gov, complete it fully, attach your supporting documents, and mail the package to the Winston-Salem VA Eligibility Center at the address listed on the form instructions. Processing by mail typically takes two to four weeks, so plan your timeline accordingly if you're under contract on a home.

Through your lender

Working with an experienced lender is often the most efficient path, especially if you're already in the loan process. Most VA-approved lenders have direct access to the VA's WebLGY system and can pull your COE on your behalf in minutes during the application. Your lender handles the request, reviews the result immediately, and flags any entitlement or funding fee issues before they slow down your closing. This method keeps everything in one workflow and reduces back-and-forth between you and the VA.

Step 3. Review your COE and resolve common issues

Once your COE arrives, whether through the online portal, by mail, or directly from your lender, do not skip reviewing it immediately. Errors and outdated data appear more often than most veterans expect, and catching a problem at this stage is far easier than dealing with one during underwriting when a closing deadline is looming.

What to check the moment your COE arrives

Your COE contains several fields that directly affect your loan terms, so verify each one before your lender submits your file for underwriting. Focus on the following items:

- Name and SSN: Confirm they match your government-issued ID exactly.

- Entitlement amount: Check whether it shows "full entitlement" or a specific dollar figure for remaining entitlement.

- Funding fee exemption: If you have a service-connected disability rating of 10% or higher, your COE should display an exemption. A missing exemption costs you money at closing.

- Loan guaranty code: This one-digit code indicates your service category and must correspond to your actual military background.

If your COE shows a partial entitlement instead of full entitlement, ask your lender to walk you through how to get a VA loan Certificate of Eligibility restoration before you apply for a new purchase.

How to fix the most common COE problems

The most frequent issue is a funding fee exemption that doesn't appear even though you have a qualifying disability rating. To resolve this, submit your VA disability award letter to your lender and ask them to reprocess the COE through WebLGY, or contact the VA directly at 1-877-827-3702. The VA can update your record and reissue a corrected COE, usually within a few business days.

Entitlement problems typically show up when a veteran has a prior VA loan that was not properly closed out. In that case, you'll need to submit VA Form 26-1880 along with documentation showing the prior loan was paid off and the property sold or transferred. Your lender can guide you through this paperwork and submit it on your behalf to get your full entitlement restored before your purchase moves forward.

Timelines, replacements, and special situations

Knowing how to get a VA loan Certificate of Eligibility is only part of the picture. You also need to understand realistic processing times, what to do if your COE gets lost, and how certain situations require extra steps before your eligibility is confirmed.

How long each method takes

Your timeline depends entirely on the submission method you choose and how complete your service records are in the VA's system. Plan around these estimates when you're working toward a specific closing date.

| Submission Method | Typical Timeline |

|---|---|

| Online via VA.gov (records already digitized) | Minutes to 1 business day |

| Online via VA.gov (documents uploaded manually) | 3 to 5 business days |

| Through your lender via WebLGY | Minutes during application |

| By mail using VA Form 26-1880 | 2 to 4 weeks |

If you're under contract on a home with a tight closing window, use your lender's WebLGY access first. Waiting on a mailed request while a contract deadline approaches puts your earnest money at risk.

Getting a replacement COE

If you lose your original COE, you do not need to restart the full application from scratch. Log back into VA.gov and download a new copy directly from your records. Your lender can also reprint a copy through the WebLGY system at any point during your loan process. Keep a digital backup in cloud storage after you receive your COE the first time so you always have access regardless of what happens to the paper copy.

Special situations: surviving spouses and restored entitlement

Surviving spouses must submit additional documentation, including the veteran's DD-214, a marriage certificate, and a death certificate, and in some cases a completed VA Form 26-1817. If the veteran's death was not service-connected, the surviving spouse may need to complete VA Form 21P-534EZ to establish dependency and indemnity compensation (DIC) first. Veterans who want to reuse their benefit after a prior VA loan is paid off need to submit VA Form 26-1880 with proof of payoff to get their full entitlement restored before applying again.

Next Steps

You now have a complete picture of how to get a VA loan Certificate of Eligibility, from gathering your proof of service to resolving entitlement issues after you receive it. The next move is straightforward: choose your submission method, pull your documents together, and submit your request. If you're already working with a lender, ask them to run your COE through WebLGY during your first conversation so you can confirm your entitlement status and funding fee exemption before you go under contract on a home.

Working with an experienced VA lender makes every stage faster and less stressful. At David Roa, I've helped veterans across Chicago and nationwide close VA loans without surprises, using 25-plus years of hands-on mortgage experience to catch COE issues before they affect your closing timeline. When you're ready to move forward, connect with a VA loan specialist at David Roa and get your COE and pre-approval process started today.